ChartWatchers February 19, 2012 at 02:28 PM

With all the press centering in upon Gold gains recently +10%, Silver has risen by +19% - thereby outperforming the yellow metal by +9%. Silver - the poor man's good; now looks rather ripe for trading once again... Read More

ChartWatchers February 18, 2012 at 09:32 PM

Energy shares were this week's strongest market sector. That's the first time we've seen relative strength by the energy sector in three months. Chart 1 shows the Energy Sector SPDR (XLE) trading at the highest level in seven months... Read More

ChartWatchers February 18, 2012 at 09:17 PM

It takes time and patience for continuation patterns to play out. Many traders grow frustrated, especially after the stealth move higher ends because of the time involved for continuation patterns to form... Read More

ChartWatchers February 18, 2012 at 07:21 AM

Of the nine sector SPDRs, the Consumer Discretionary SPDR (XLY) and the Technology SPDR (XLK) have the highest StockCharts Technical Rank (SCTR). The SCTR for the Industrials SPDR (XLI) is in a close third... Read More

ChartWatchers February 17, 2012 at 08:17 PM

News headlines are usually more confusing than helpful, especially when trying to determine if stocks are overvalued, fairly valued, ot undervalued. At any given time there will be those who simultaneously claim that stocks overvalued and undervalued... Read More

ChartWatchers February 05, 2012 at 02:45 AM

(THIS WEEK'S DECISION POINT ARTICLE WAS WRITTEN BY GUEST WRITER ERIN SWENLIN HEIM) As many of you are aware, I've been doing my duty as a citizen of this great country by serving on a jury. It has been interesting, to say the least... Read More

ChartWatchers February 04, 2012 at 09:41 PM

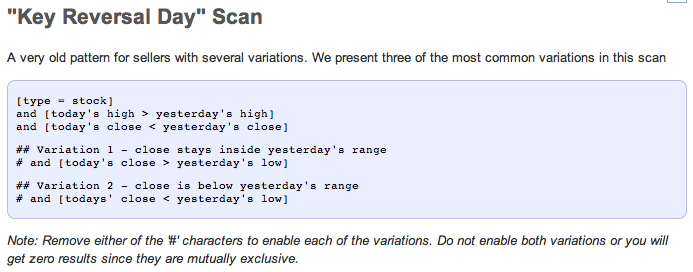

Hello Fellow ChartWatchers, Today I'm please to announce the grand opening of our Advanced Scan Library. We've collected some of the best scans available and posted them in this new ChartSchool area for everyone to see... Read More

ChartWatchers February 04, 2012 at 06:31 PM

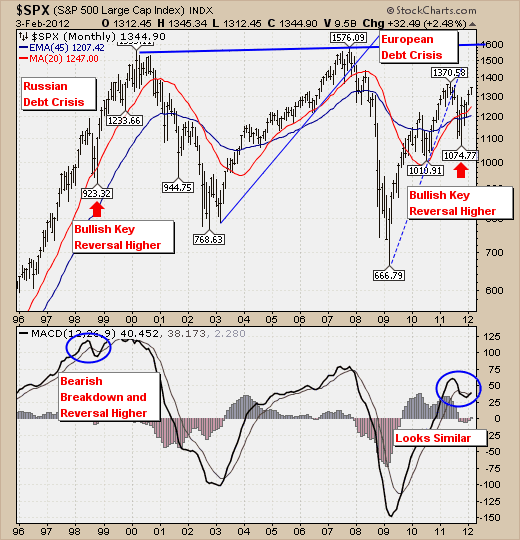

My market message from Thurs, Jan 26th, argued for the inclusion of Canada in a foreign stock portfolio. I'm going to expand on Canada's unique role in the global intermarket picture in this message. In my view, Canada is unique for at least three reasons... Read More

ChartWatchers February 04, 2012 at 06:27 PM

The 2012 trading year has begun with a "bang" to be sure. In terms of the S&P 500, we find that 16 of the 23 trading sessions have traded to the upside, with no losing session down more than -8 points or -0.6%... Read More

ChartWatchers February 04, 2012 at 06:23 PM

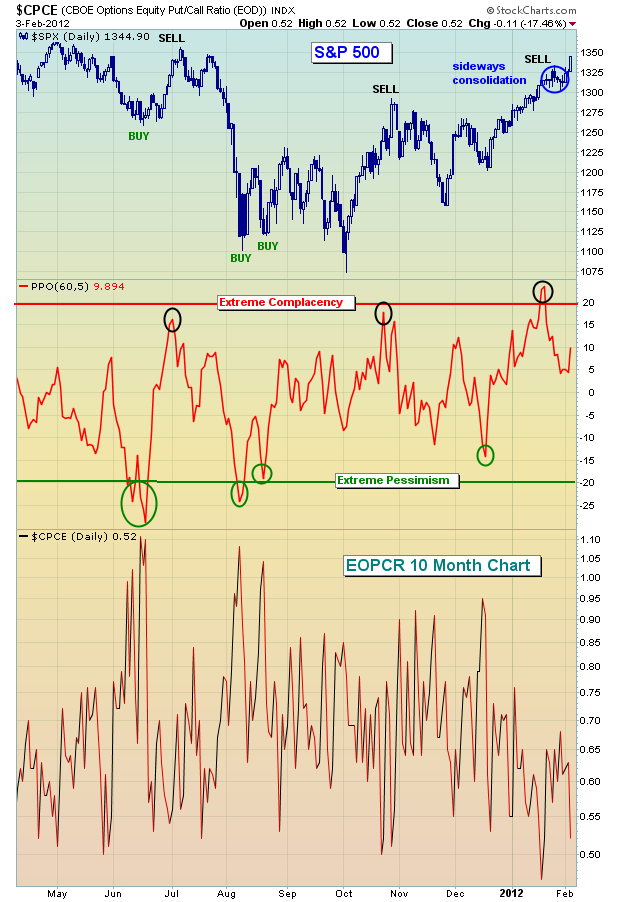

Two weeks ago, I wrote that equities were very overbought and quite complacent. While we didn't see any selling of substance, the market did struggle to move up - that is, until Friday's Nonfarm Payrolls hit the wires... Read More

ChartWatchers February 04, 2012 at 11:59 AM

With a string of positive economic reports lifting stocks this week, the S&P 500 ETF (SPY) closed higher for the fifth consecutive week. Friday was a big reporting day with Factory Orders showing strength, IWM Services indicating expansion and the employment rate coming down... Read More