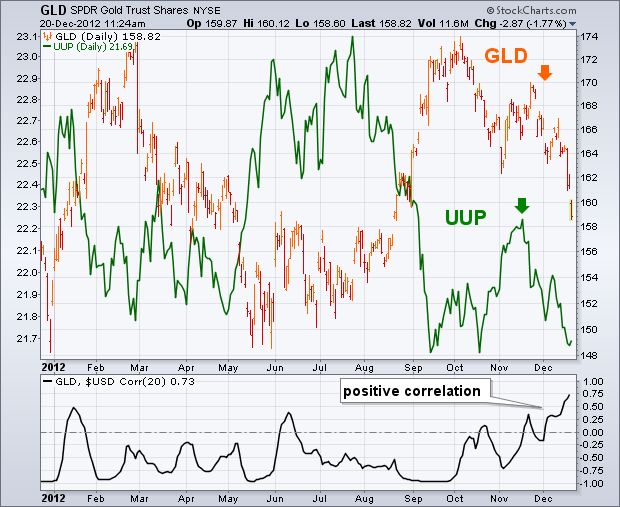

ChartWatchers December 23, 2012 at 01:13 AM

One of the most consistent intermarket principles is that gold (and most commodities) usually trend in the opposite direction of the U.S. Dollar. That inverse relationship has broken down of late. Chart 1 compares the Gold Trust (GLD) to the Dollar Index (UUP) over the last year... Read More

ChartWatchers December 23, 2012 at 01:06 AM

To historians, this doesn't come as a surprise. Since 1987, the Russell 2000 has produced annualized returns during the month of December of 43.38%. April is the next best month for small caps with its annualized return of 21.84%, a very distant second... Read More

ChartWatchers December 23, 2012 at 01:04 AM

In the past several weeks, the FOMC has voted to "expand" its balance sheet until which time economic growth is strong and getting stronger ($45 billion long-term treasuries/$45 MBS)... Read More

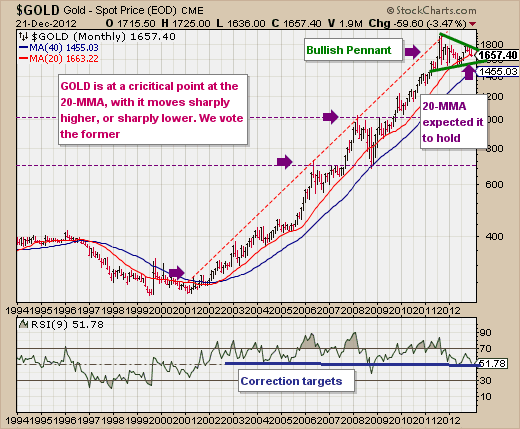

ChartWatchers December 22, 2012 at 05:56 PM

About a month ago I wrote an article stating that I thought that gold was resuming its long-term up trend, but that belief was conditioned upon price moving above the October top. That did not happen... Read More

ChartWatchers December 22, 2012 at 11:48 AM

2012 is ending with a bang for banking stocks as sentiment towards this sector improved significantly in December. Perhaps the big banks are looking forward to open-ended quantitative easing in 2013... Read More

ChartWatchers December 08, 2012 at 05:16 PM

Homebuilders have been a leading industry group throughout the S&P 500 rally off the 2009 lows. This strength has been particularly obvious over the past year. Looking strictly at a shorter-term chart, technical indicators couldn't look much better... Read More

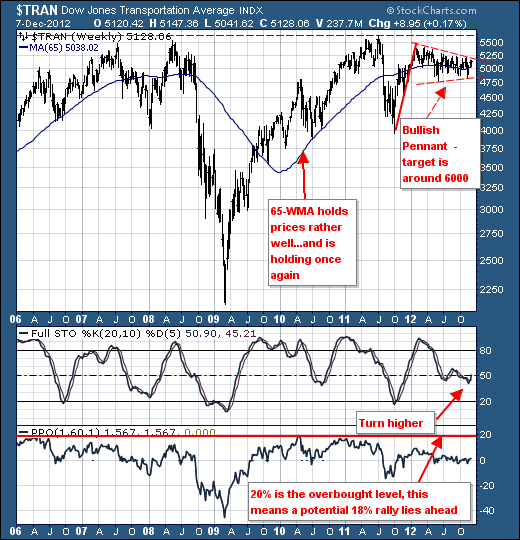

ChartWatchers December 08, 2012 at 05:13 PM

The Dow Jones Transportation Index ($DJT) is on the verge of a major breakout that could see prices rise by up to +20%... Read More

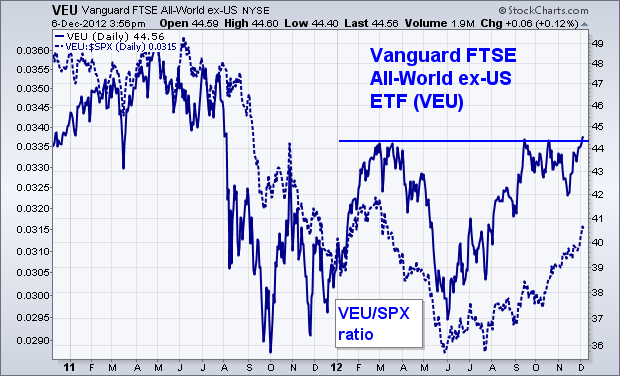

ChartWatchers December 08, 2012 at 05:04 PM

Foreign stocks look technically stronger than the U.S. at the moment. Tuesday's message showed EAFE iShares testing their spring high. Emerging markets are rising as well. A more comprehensive measure of foreign stocks that includes developed and emerging markets is shown below... Read More

ChartWatchers December 08, 2012 at 09:00 AM

Gasoline Jan13 (^RBF13) formed a lower high and broke support with a sharp decline this week. First, notice that the trend since mid September is down with a series of lower lows and lower highs taking shape the last few months... Read More