If you want the best raw performance over the long term, expanding your menu to 13 asset classes, plus a simple mechanical formula, is just the ticket. • Standing on the shoulders of giants in finance — including Nobel Prize winners — ETF pioneer Mebane Faber developed and publicly disclosed the best way to select the low-cost index funds that are most likely to outperform in the coming month.

Figure 1. Faber is co-author of the 5-asset Ivy Portfolio and the architect of an improved 13-asset strategy, which the book Muscular Portfolios calls the Papa Bear Portfolio. Photo by Ringo Chiu/Zuma Press/Alamy.

• Parts 1, 2, and 3 of this column appeared on Jan. 1, 3, and 8, 2019. •

Mebane Faber is one of the best-known names in the small world of exchange-traded fund (ETF) sponsors. His firm, Cambria Investment Management, has started 11 ETFs in the past few years — each with its own unique niche.

For example, the Cambria Tail Risk ETF (symbol: TAIL) is for people who think bad things are going to happen. The ETF holds mostly US Treasury notes and put options on US stocks. As you’d expect, the fund does poorly during market rallies and well during corrections. From the recent Sept. 20 top to the Dec. 24 low, TAIL gained 23.90% while SPY dropped 19.35%.

Faber gained public attention through his book The Ivy Portfolio. He argued that individual investors should be able to get the same handsome returns as professionally managed Ivy League endowment funds. Faber first posted a five-asset strategy to the Social Sciences Research Network (SSRN) in 2006. His work was then selected for publication as an article in the spring 2007 issue of the prestigious Journal of Wealth Management. The book, based on the same material, was published in 2009 by Wiley.

Fortunately for the historical record, market experts — such as Doug Short of Advisor Perspectives — began tracking Faber’s simple formula in real time at the beginning of 2007. That was just before the beginning of the Great Recession and the worst stock-market crash in decades.

Short’s real-time figures showed that Faber’s simple asset-rotation strategy lost no more than a very mild 7% in the 2007–2009 bear market. During the same period, of course, the S&P 500 including dividends crashed more than 50%. (All drawdowns in this column are measured between month-ends.)

With this success under his belt, Faber went to work on improving his selection of assets. His much-revised SSRN whitepaper, “A Quantitative Approach to Tactical Asset Allocation,” went live in February 2013. It featured a complete set of 13 asset classes and an even simpler formula than before. The text significantly updated the previous strategy for greater gains, at the expense of somewhat larger drawdowns during bear markets. Faber’s owes an intellectual debt (as do we all) to finance professors — such as Eugene Fama, a winner of the Nobel Prize in Economics — who’ve demonstrated that assets with good performance over the past 3 to 12 months are statistically likely to outperform in the following one month. (For details, see my summary page.)

SSRN is a repository of academic papers by more than 250,000 authors. Despite the long odds, Faber’s 2013 paper ranks as the No. 1 most-downloaded of all time.

That’s an indication of popularity, but not necessarily of usage. Faber specified the 13 asset classes but didn’t name any mutual funds or ETFs could use to match those indexes. The book Muscular Portfolios is the first source to “clone” the strategy (i.e., make it freely available to individual investors) and reveal the ETFs that precisely fit. The MuscularPortfolios.com website updates the rankings of these ETFs every 10 minutes during market hours. The book also lists mutual funds that track the same indexes, for 401(k) account holders whose plans do not yet support ETFs.

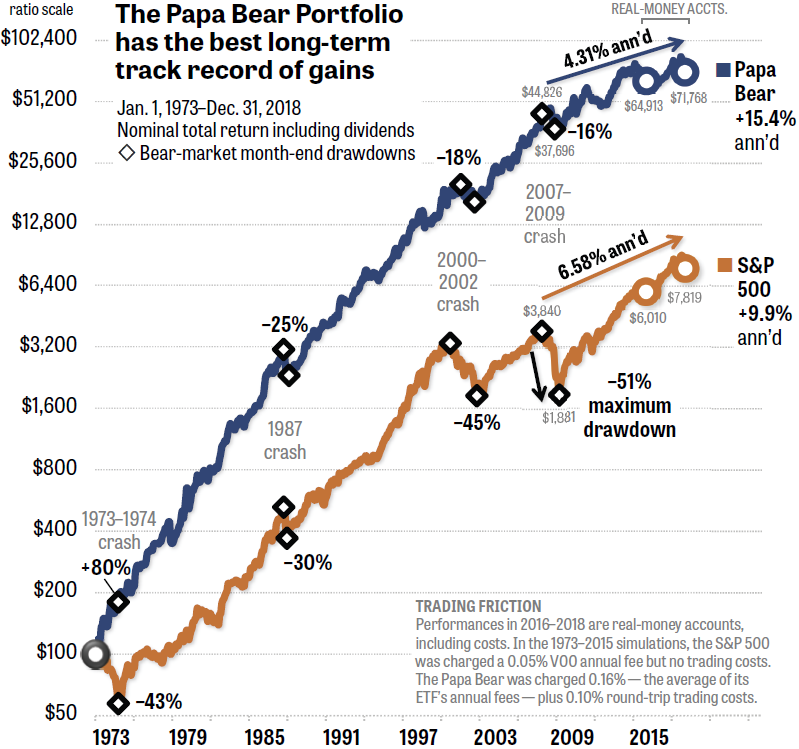

We now have 46 years of data. The first 43 years are estimated by the Quant simulator, while the last three are based on a real-money tracking account at FolioInvesting.com. During the entire 46-year period, the Papa Bear delivered an annualized rate of return of 15.4%. The S&P 500 total return was “only” 9.9%. Despite the Papa Bear’s strength, it never subjected investors to drawdowns worse than 25% — the level at which many people throw in the towel, hurting their lifetime performance.

You can see why I like the Papa Bear. Even if its performance in future decades only matches that of the S&P 500, the Papa Bear’s much lower losses during crashes would make it all worthwhile.

Long-term performance is more predictable than short-term

As I’ve stated many times, investing strategies should never be evaluated over any period less than one full bear-bull market cycle — and preferably more than one. But many readers want to know the latest performance figures for shorter periods.

The book’s graphs end on Dec. 31, 2015, since that’s as much asset-class data as was available when the text was being written. Figure 2, shown below, adds the Papa Bear’s 2016–2018 real-money experience to the 1973–2015 simulated performance.

Figure 2. The Papa Bear has shown great performance over long periods, but is lagging during the current bear-bull market cycle. Source: Quant simulator (1973–2015), real-money accounts (2016–2018).

As we saw earlier, the Mama Bear beat the S&P 500 total return in the current 2007–2018 bear-bull market cycle: 7.67% annualized vs. 6.58%.

The Papa Bear suffered hiccups during the same cycle, returning 4.31% annualized vs. the S&P 500’s 6.58%. That’s a noticeable underperformance.

What we’ve learned from our examination of all three portfolios by LeCompte, Bogle, and Faber is this:

- The Mama Bear Portfolio beat the S&P 500 in both the 46-year long-term record and in the latest bear-bull cycle beginning on Oct. 31, 2007. That’s a performance that most high-priced hedge funds can’t claim.

- The Baby Bear Portfolio, with nothing more complex than its 50/50 balance of US stocks and US bonds, closely tracked the return of the S&P 500 — within a fraction of a percentage point. That’s my definition of “market-like returns.” A Baby Bear account would have had a higher dollar balance than a buy-and-hold S&P 500 account in 61% of the months during the 46-year record. That’s remarkable for such a simple strategy.

- The Papa Bear Portfolio beat the S&P 500 by more than the other strategies over the 46-year period, but is underperforming the index during the most recent market cycle. Competing against one of the longest bull markets in history (almost 10 years) was more than the Papa Bear was able to manage.

As we saw with the Mama Bear in Part 2 of this column, the Papa Bear peaked and bottomed during the financial crisis in different months than the S&P 500 did. Using its own unique start and end dates, the Papa Bear was actually down a still-tolerable 21% at one point during the financial crisis. This drawdown is shown in Figure 6-1 of the book. But to compare apples to apples, Figure 2 herein uses the same start and end dates for both the S&P 500 and the Papa Bear. The 21% drawdown is still fully reflected in the performance numbers graphed in Figure 2.

Investing does not give us guarantees but probabilities

At the beginning of Part 1 of this column, I published the three ETFs that the Mama Bear and the Papa Bear formulas predict will do the best in the 30 days to come. Do I expect these six ETFs to beat the S&P 500 in one month? No, I don’t. Asset classes with strong momentum are statistically likely to do well in the coming weeks. But the true value of any mechanical formula only shows up when the cycle is complete. It’s not how much you make, it’s how much you keep. My publication of the list is intended to spark a discussion about using mechanical formulas instead of trusting our opinions, which have been shown to disappoint us.

The Papa Bear’s underperformance in the current (almost) 10-year market cycle would be accepted by finance experts if the portfolio produced a better risk-adjusted return than its benchmark. Rick-adjusted performance is a difficult measure for the crash-prone S&P 500 to excel on.

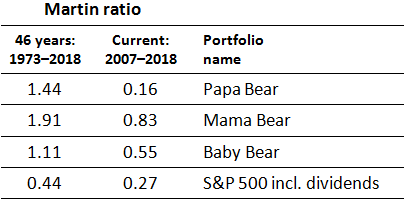

The best risk-adjusted performance measure I’ve found is called the Martin ratio. This calculation is a big improvement on the old Sharpe ratio, which gives identical ratings to extremely different strategies. (Follow the link in this paragraph or see the Bonus Chapter of Muscular Portfolios for complete details.)

Here are the Martin ratios of the portfolios for the entire 46-year period and just for the current bear-bull market cycle (monthly closes from Oct. 31, 2007, through Dec. 31, 2018):

All of the portfolios have better risk-adjusted returns than the S&P 500 over the 46-year period, and all but the Papa Bear have better risk-adjusted returns in the current bear-bull market cycle. Investors who hate experiencing the crashing of their life savings — which affects even the most hardened traders — will like Muscular Portfolios for the small losses, compared with the S&P 500. But these strategies are not guarantees, they are probabilities for outperformance over time.

All of the portfolios have better risk-adjusted returns than the S&P 500 over the 46-year period, and all but the Papa Bear have better risk-adjusted returns in the current bear-bull market cycle. Investors who hate experiencing the crashing of their life savings — which affects even the most hardened traders — will like Muscular Portfolios for the small losses, compared with the S&P 500. But these strategies are not guarantees, they are probabilities for outperformance over time.

I’ll continue to examine the Papa Bear to discover ways to strengthen it in all kinds of markets. In the meantime, the Mama Bear and the Baby Bear are doing exactly what they were developed by their designers to do, even in one of the longest bull markets in history. (Note: At this writing, the bull market isn’t over. The S&P 500 closed only 19.9% down on Dec. 24, not more than 20% down, which is the usual definition of a bear. After we have confirmation that the bull market is over, I’ll recompute the portfolio returns for the entire market cycle. Stay tuned!)

With great knowledge comes great responsibility.

—Brian Livingston

Send story ideas to MaxGaines “at” BrianLivingston.com