Pioneers of the index investing revolution, such as Vanguard, started their movement in the United States. But what if your interests go beyond the US? • There are many reasons why an individual investor should take a global view of asset allocation. This process can reveal to us a lot about how to construct the ideal portfolio, no matter where in the world our assets may reside.

Figure 1. The TSX 60 is a broad equity-market index of companies listed on the Toronto Stock Exchange, similiar to the composition of the S&P 500 but priced in Canadian dollars. Photo by Pavel Ignatov/ Shutterstock.

• NOTICE: This column will begin a temporary hiatus in August 2019. To continue receiving my articles, subscribe now to the free Muscular Portfolios Newsletter.

All long-term investing comes down to three basic points, which I call Core Principles:

- Compounding. By not removing your gains until you absolutely need to, your portfolio will eventually pay you more than you can earn by working at any job.

- Diversification. Remaining 100% invested in at least three different asset classes from an expert-designed menu gives you greater gains with smaller declines than a portfolio with only one asset class or a static asset allocation.

- Momentum. Holding the asset classes with the best performance over the past 3 to 12 months tends to improve a portfolio’s gains and reduce its drawdowns.

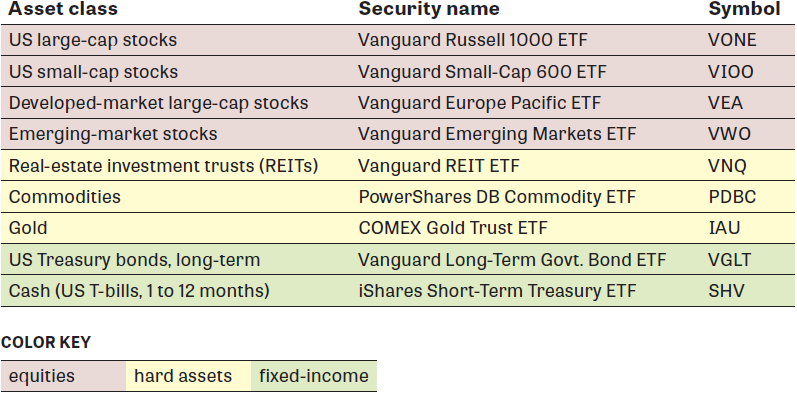

At my Muscular Portfolios website, I give away, free of charge, two menus of ultra-low-cost global index ETFs that were originally designed by Mebane Faber, co-author of The Ivy Portfolio, and Steve LeCompte, CEO of the CXO Advisory Group. In addition, the ETFs are ranked by their relative strength. The rankings are updated every 10 minutes while the market is open. An example of the CXO menu is shown below in Figure 2.

A reader of this column, Peter D., asked: “Most of my investments are in Canadian dollars. Is there a way to use the same portfolio system?”

That’s a question that applies to us all, whether you are American, Canadian, or any other nationality:

- Although StockCharts is an American company, the Web is global, and the server stats tell me 30% of my readers are outside the US. Almost half of those folks view my column from Canada.

- If you work for a big organization, it might someday send you to Europe, Japan, or any number of other places to work, each of which has its own currency and unique marketplace of available financial products.

- It’s very common for retirees to relocate to a country with a lower cost of living, such as Mexico, Costa Rica, or Kazakhstan — again, with their own distinct currencies and index funds. (Don’t laugh, I actually have 20 readers in Kazakhstan!)

In this article, we’ll see how to construct an “investing universe” (menu) of low-cost index funds that’s tailored to the currency and the financial products that are available in whatever country you might find yourself.

Figure 2. The CXO selection of US-based index funds — also called the Mama Bear Portfolio — includes nine different asset classes, which I consider the minimum number necessary to take advantage of diversification and momentum. Source: Muscular Portfolios website.

Since many of my readers are based in Canada, I’ll use that country’s financial products as an example. The same principles also apply to many other nations.

Investors everywhere tend to buy assets that are denominated in their own currency. For Canadians, that means Canadian dollars (CAD). Buying index funds that are priced in US dollars (USD), such as the ETFs in Figure 2, could expose investors in other countries to currency risk.

For example, due to currency fluctuations, assets priced in US dollars lost about 35% of their value in Canadian dollars in the nine-year period from Nov. 6, 2007, to Jan. 21, 2016. On the other hand, a Canadian investor holding USD assets enjoyed a 74% boost in value during the previous six years: Feb. 26, 2002, to Nov. 6, 2007. That’s currency risk, whether it turns out to be working for you or against you (see graph).

You can’t easily predict fluctuations in foreign exchange. As I reported in a previous column on currency speculation, 70% of currency traders lose money. For your own peace of mind, you may wish to eliminate currency moves as a source of profit/loss in your portfolio — and therefore sleep well at night.

Which ETFs priced in Canadian dollars would roughly replicate a portfolio of ETFs priced in USD? One effort to answer this question was published by Dan Bortolotti. He writes a column called the Canadian Couch Potato for MoneySense.ca.

In his USD-to-CAD column, he uses the so-called Coffeehouse Portfolio as an illustration. That’s a static asset allocation strategy published in 2001 by Bill Schultheis, a financial adviser and co-founder of Soundmark Wealth Management. I analyzed Schultheis’s portfolio in my June 25, 2019, column.

Bortolotti recommends the following substitutions for the Coffeehouse menu of assets:

- Instead of Vanguard ETFs that track the S&P 500, use Canadian funds that track Canada’s own TSX 60 benchmark. (These funds are denominated in CAD.)

- Instead of Vanguard’s All-World Ex-US ETF, which would duplicate the TSX 60, use Vanguard’s Europe-Pacific and Emerging Markets ETFs (which are denominated in USD).

- Instead of Vanguard’s US real-estate investment trust ETF, use one of two Canadian REIT index funds (denominated in CAD) and possibly an international REIT fund for global exposure.

- Instead of Vanguard’s US bond market ETF, use a Canadian total bond market ETF, priced in CAD.

For specific fund names and symbols, see Bortolotti’s column.

Asked for comment, Bortolotti suggested that I contact Benjamin Felix, a portfolio manager for PWL Capital in Ottawa, Ontario.

In a email, Felix said, “I do not think that there is any need to worry too much” about foreign exchange fluctuations. “Long-term, currency returns are expected to be zero.”

Felix published a PDF white paper on the subject, which provides a specific list of six ETFs he recommends for Canadian investors. Some of the funds are denominated in CAD, while others are US-based ETFs priced in USD. He’s also posted a YouTube video on whether you should protect a portfolio from currency fluctuations.

In my view, both Bortolotti’s and Felix’s approaches qualify as Lazy Portfolios. As I showed in a previous article on Lazy Portfolios, these static asset allocation strategies do not change the percentages you hold in each asset as market conditions change. In addition, actual individual investors might not want to wait 5 to 10 years to see whether exchange rates were going to wipe out a large portion of their gains.

To illustrate the enhancements that are easily possible, adding a single Momentum Rule improved the Coffeehouse Portfolio’s annualized return to 15.1% from 10.5%, resulting in five times more ending value over a 43-year period, as described in my earlier column on Coffeehouse.

In the second part of this series, we’ll see a global investing menu that:

- Truly protects against currency risk;

- Takes advantage of the latest findings on the momentum factor to safely boost our gains; and

- Tilts our portfolio away from equity-market crashes.

If you have suggestions on non-USD portfolios, send me an email at the address below by 5 p.m. PT on July 23, 2019.

• Part 2 appears on July 25, 2019.

With great knowledge comes great responsibility.

—Brian Livingston

Send story ideas to MaxGaines “at” BrianLivingston.com