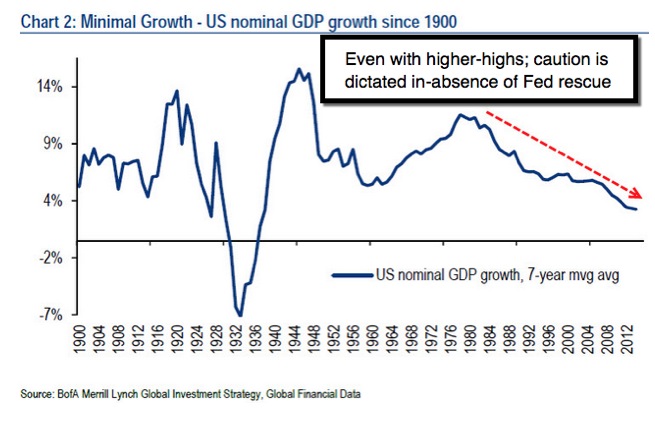

Market vulnerability - is actually elevated by virtue of not only higher levels (a further divorce from reality); by a renewal of overbought technical aspects; by a paucity of favorable earnings or 'policy' pronouncements ahead; but also by increased realization monetary policy is moving in the direction called for. To all that one can add the incalculable brewing geopolitical risks. (The Daily Briefing full report assesses handling near-term Ukrainian news.) To that add our review of the real implications of hardball between Greece and the ECB.

The equity market continues to debate and 'churn' around where this leads; a sort of 'tension-on-the-tape' environment, where alternating moves dominate; and a clear resolution does not, even as primarily domestic stocks advance a bit. Also, behind the scenes there is chatter about global 'central bank' capital structures, as increasingly at-risk to a degree; although that in-itself is hard to gauge, while there's little doubt psychological efforts to 'talk-up' recovery sure exceed most-sector realities in the real world, and for 'most' households. This is all part of what I've called a technical 'disconnect' that bears concern.

On Friday, the majority believe the after-lunch shakeout was due to S&P's cut of Greek Debt; that was part of it; so they rebounded those who sold into the immediate weakness. But the rebound didn't stick for a different reason: few noticed the concurrent statements by Lachman of the Fed (and Plosser) that basically continue to prepare markets (or try to) for monetary transitions.

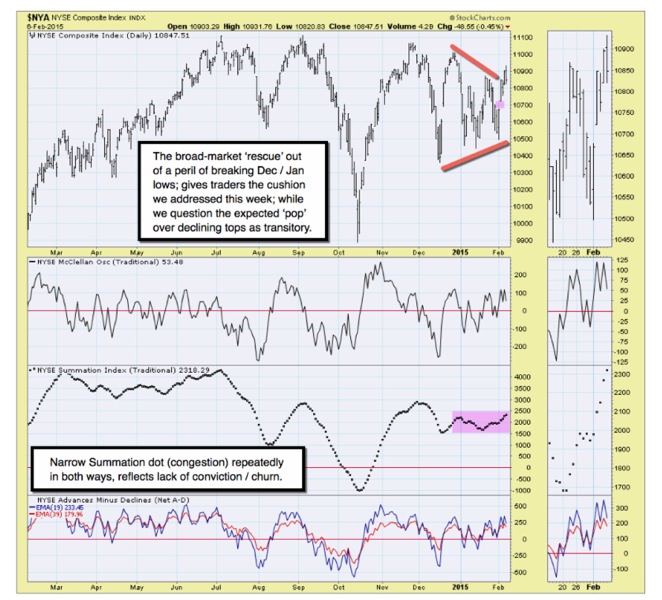

Did traders push the latest rebound more than can be sustained? Creating a 'cushion' zone above nearly-twin December and January lows; creates more 'technical' maneuvering room (and trading opportunities we welcome again).

The week just past was not easy; even intraday swings often had nothing to do with overall technical behavior. ( Prospective action ahead detailed next.)

In the short run the market is sensitive to anything coming out of Moscow (on Ukraine). Realistically 'peace hopes' for European Unity are discounted; thus leave vulnerability if (as so far points negative pending now a Wed. meeting); while the meetings thus far feature a series of blasts from both sides (more).

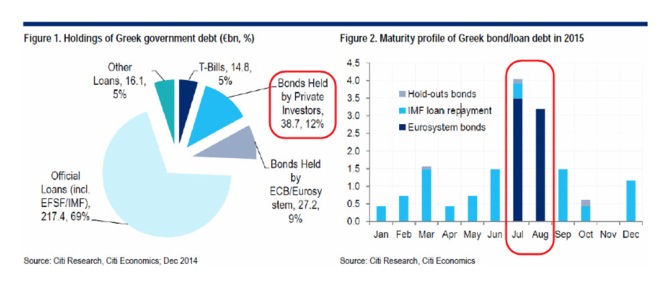

Meanwhile, the stock market has clearance; Greece does not; and tough talk is something markets are trying to adjust too; but dangers lurk (such as China and Swiss moves that may be forthcoming; while nobody mentions Turkey; a potentially unfolding basket case).

Daily action - we go into the weekend with a seemingly 'defiant' Putin; and a false statement of optimism on Ukraine that firmed the S&P right after NYSE closed the week. We hope for progress, but that's definitely pending, if at all.

(Reports Saturday and Sunday are not encouraging and suggest fragmented positions; whether 'lethal arms' debate; or concern France suggests differing US / Russian and EU / Russian 'interests'. Sec'y. Kerry argues it's not so.)

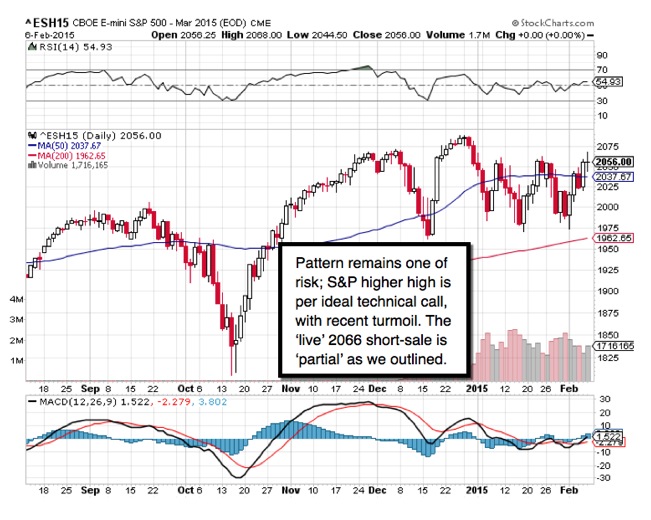

Recognizing the market may or may not rally or tank Monday initially on news from Moscow regarding Ukraine, the idea was to hold some skin-in-the-game over the weekend; since we had a 20 handle gain on a March S&P guideline ahead of the Bell. Essentially suggested: either take the gain; or to split it (as outlined); leaving a guideline March E-mini short-sale from 2066 alive.

Prior highlights follow:

Europe's 'populist groundswell' - in the wake of the ECB & IMF 'initial' blink on Athens post-Election stance (particularly demonstrations in Spain), served as a 'call to arms' by the 'conventional playbook wisdom' among central bank and sovereign leaders, as well as emboldened Grecian leaders to believe the 'track' they were taking had popular support (currency & oil discussions).

The 'theatrical genre' of Greek comedy - can be described as a dramatic performance, which pits two groups against each other in an often amusing, but simultaneously agonizing, performance. Call it mystical bullish optimism.

A Greek comedy can be funny, or have a tragic ending. Likewise many Greek tragedies had amusing conclusions. This market projects a sort of kine-static approach to theatrical techniques; which leaves the audience wondering if it's real, or a satire. I suspect that applies to the 'actual' Greeks just now; plus the players in Europe, who are torn between walking out of the show (denying all efforts to restructure Greek debt); or bowing to reality of holding the Eurozone together, and therefore renegotiating along the lines Athens proposes.

(Aside Oil, just analyzed); the Dollar dip was projected; as it the upside angle of attack was too steep; but still (given global mess); still within an uptrend. (It stems from a strong Dollar call since 79, and projected Euro drop from 1.40; this and 'divergence' charges between macro and S&P levels in full report.)

Bottom-line: typically a protagonist in a Greek tragedy commits some terrible crime without realizing how foolish and arrogant he has been. Then, as he slowly realizes his error, the world crumbles around him.

We tend to think that's what the stock market, and perhaps certain leaders on the global stage, face. Bulls arrogance is a known quantity; low liquidity is as well. So you get the '3 Act' tragic-comedies; which can culminate in what the Greek's called 'catharsis'.

Is S&P's extension likely to be a 'Trojan Horse'.

Bottom-line: stock markets were on borrowed time. We had a year-end 'grind' many 'wanted' to believe in; with no particular impetus to move it forward. Markets started to fade, with alternating declines and rebounds as the process was suspected to evolve; and a late January expected fade. In a sense ensuing comebacks allow a bit more macro borrowed time; ideally continuing trading swings for members, pending 'the 2015 line' break.

Rebounds persist because of fear, not optimism. They won't let go, which took us in recent days back to: 'something's got to give'.

Gene

Gene Inger

www.ingerletter.com