Rationales & Targets

British economist John Maynard Keynes coined quite a few memorable phrases in his illustrious career, including “The market can stay irrational longer than you can stay solvent,” the principal reason we have not been willing to short as prices have risen to ridiculous extremes. Keynes also said, “In the long run, we are all dead,” a quite sensible reason to remain bearish. Bull markets die and the odds have risen sharply for this one to die and to die a nasty death. Valuations are so stretched that a 50% collapse in price, as occurred twice before in the last 15 years, is possible.

The expansion of credit/debt over the last 15 years is truly frightening. The five largest central banks cumulatively total more than $18 trillion. They were less than half that size—$8 trillion—just before the collapse of Lehman and are now nine times their size in 2000. The present environment attempts to support the most massive leverage worldwide than ever before. If expansion of credit/debt continues at this rate, the slightest pullback in demand will likely be sufficient to trigger at the very last, an economic recession. In the meantime, we are stuck with extraordinary and gross overvaluations. The S&P 500 trade 88% higher than in 2012, yet earnings are down 9%. At this juncture, it all feels like déjà vu. Clearly, it’s not remotely like 2000 or even 2007, but we’ve definitely been here twice before in this century.

Internal Dynamaics Have Deteriorated

Please note: a free three issue trial to Crosscurrents is available upon request.

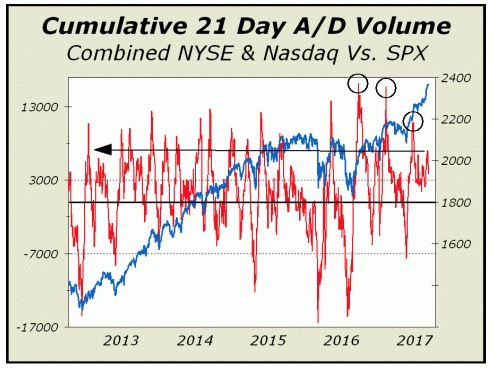

Price doesn’t tell you everything. At some point, the internal dynamics change and a reversal of trend is indicated. We measure this internal health by comparing the performance of breadth, volume and the new highs/new lows list. We’ve seen negative divergences for months for all three without any change in trend, not even a correction. If anything, the indexes has been more on a roll than before. Does this change our view?

In fact, it does not. Amazingly, the near straight up rally since the election has only intensified the negative divergences at left, a unique development in our experience. Typically, we would not expect to see the market’s internal dynamics lagging at all. Given a 15.5% spike in prices, the pictures at left are frightening.

Below, volume dynamics have faded badly. In fact, while prices advanced for the major indexes last Wednesday, Thursday and Friday, there was significantly more declining volume on the NYSE than advancing volume for all three days. Nasdaq managed to show more advancing volume on Friday but still had significantly more declining volume on Wednesday and Thursday. Our indicator illustrates a rather large draw down in advancing minus declining volume from the first spike in prices post election (see third highlighted circle). As well, we have placed an arrow from the most recent peak last Monday all the way back to 2012 to show just how weak the rally from February 7th has been.

For more information, please contact us:

Alan M. Newman, Editor, Crosscurrents

www.cross-currents.net