Market Recap for Wednesday, June 14, 2017

The FOMC concluded its two day meeting on Wednesday afternoon and, for the most part, followed its prior script. They stuck to their previous plan to raise interest rates for a third time in six months and maintain their forecast for another rate hike in 2017. They also indicated their intentions for three more rate hikes in 2018 and discussed their plan to reduce their bloated balance sheet. The market response? Mostly boring to be quite honest. The Dow Jones and S&P 500 traded in a 0.5% range in the final two hours, although the NASDAQ resumed its recent volatile action and sold off roughly 1% in the hour following the Fed's announcement before turning higher and cutting those losses in half by the close. Here's the NASDAQ's intraday volatility visualized:

There was some serious back and forth action on the NASDAQ yesterday afternoon, but neither the afternoon high or low cleared what I consider to be the NASDAQ's very short-term trading range from roughly 6110-6240.

There was some serious back and forth action on the NASDAQ yesterday afternoon, but neither the afternoon high or low cleared what I consider to be the NASDAQ's very short-term trading range from roughly 6110-6240.

The reason the NASDAQ underperformed after the FOMC announcement is rather clear. Traders sought safety. Wednesday's leadership came from consumer staples (XLP, +0.63%), utilities (XLU, +0.54%) and healthcare (XLV, +0.48%). Drug retailers ($DJUSRD) closed at its highest level since mid-March to lead the consumer staples space. With a recent bullish MACD crossover, this group appears to be poised to continue its rally to test a significant gap resistance level as shown below:

Tobacco ($DJUSTB), another consumer staples industry group, was strong on Wednesday as it bounced off rising 20 day EMA support. That chart can be found under the Sector/Industry Watch section below.

Tobacco ($DJUSTB), another consumer staples industry group, was strong on Wednesday as it bounced off rising 20 day EMA support. That chart can be found under the Sector/Industry Watch section below.

Pre-Market Action

One day after the Federal Reserve raised interest rates and suggested our economy will continue to improve during the balance of 2017, we have several economic reports to be released. Already this morning, we've seen better than expected reports in terms of initial jobless claims, the Philly Fed and the empire state manufacturing survey. That's resulted in a slight uptick in the 10 year treasury yield ($TNX). Gold ($GOLD) is taking its largest hit in awhile and crude oil ($WTIC) is down again this morning after a brutal day on Wednesday where the WTIC fell 3.72%.

The Hang Seng index ($HSI) fell more than 1% overnight in Asia and all the key European indices are down over 1% this morning. That's set the tone for a weak open here as Dow Jones futures are lower by 85 points. It's setting up to be another rough open for NASDAQ stocks, adding to the volatility there of late.

Current Outlook

I've mentioned this before.....and I'll mention it again. Railroads ($DJUSRR) are very risky at this juncture. Not only have they reached a key resistance level near 1600, they're doing so with a very ugly negative divergence on their weekly chart. These types of negative divergences can result in sideways consolidation or outright selling for the next few to several months so without a definitive, high volume breakout above 1600, I'd look elsewhere for long positions. Here's the chart:

It's been 18 months of investing bliss in railroads with the weekly MACD cooperating every step of the way. However, the failure of the MACD to turn higher on the most recent advance is an indication of waning bullish price momentum. That, combined with lower volume of late, suggests the run higher in railroads is likely over - at least over the summer. We'll soon find out.

It's been 18 months of investing bliss in railroads with the weekly MACD cooperating every step of the way. However, the failure of the MACD to turn higher on the most recent advance is an indication of waning bullish price momentum. That, combined with lower volume of late, suggests the run higher in railroads is likely over - at least over the summer. We'll soon find out.

Sector/Industry Watch

The Dow Jones U.S. Tobacco Index ($DJUSTB) rallied exactly where you'd expect from a technical perspective as momentum there is very strong and the 20 day EMA was tested. Here it is:

Tobacco had a huge run from mid-May into the second week of June, but became extremely overbought as the RSI and stochastic readings above show. Readings above 70 on the RSI and 90 on stochastic is my signal that an index or stock needs some short-term relief. While overbought can remain overbought for awhile, just realize that entering an overbought group increases risk significantly. It doesn't mean we'll see a pullback, it simply tells you that entering is much riskier given the recent advance. The DJUSTB did pull back subsequently and when it reached its 20 day EMA test, note that both RSI and stochastic had fallen back into their 50s, a much more palatable (and less risky) entry point.

Tobacco had a huge run from mid-May into the second week of June, but became extremely overbought as the RSI and stochastic readings above show. Readings above 70 on the RSI and 90 on stochastic is my signal that an index or stock needs some short-term relief. While overbought can remain overbought for awhile, just realize that entering an overbought group increases risk significantly. It doesn't mean we'll see a pullback, it simply tells you that entering is much riskier given the recent advance. The DJUSTB did pull back subsequently and when it reached its 20 day EMA test, note that both RSI and stochastic had fallen back into their 50s, a much more palatable (and less risky) entry point.

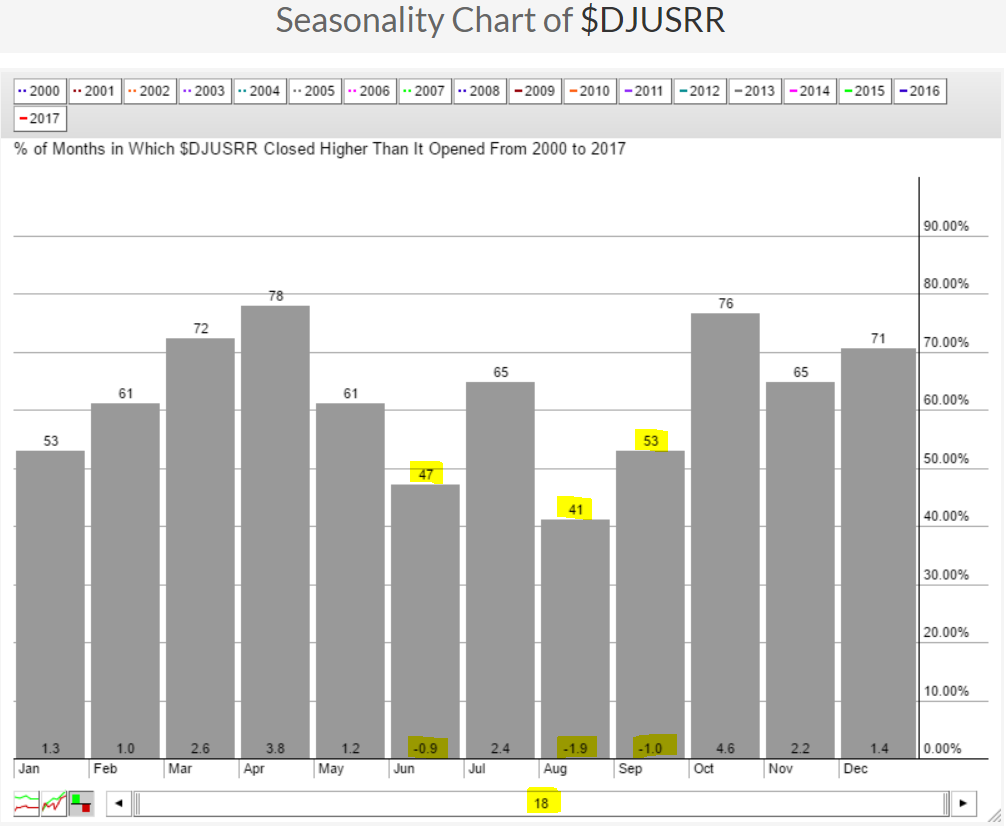

Historical Tendencies

The technical issues with railroads ($DJUSRR) were discussed above in the Current Outlook section. They also have seasonal issues during the summer months as June, August and September all tend to be quite weak. Only July provides historical relief as you can see below:

Note that every calendar month outside of the summer months highlighted above have averaged positive returns over the past 18 years. It's fairly evident to me that railroads face an uphill summer battle. After seeing the weekly negative divergence emerge, is this really an area we want to take a chance on the long side?

Note that every calendar month outside of the summer months highlighted above have averaged positive returns over the past 18 years. It's fairly evident to me that railroads face an uphill summer battle. After seeing the weekly negative divergence emerge, is this really an area we want to take a chance on the long side?

Key Earnings Reports

(actual vs. estimate):

KR: .58 vs .57

Key Economic Reports

Initial jobless claims released at 8:30am EST: 237,000 (actual) vs. 243,000 (estimate)

June Philadelphia Fed Survey released at 8:30am EST: 27.6 (actual) vs. 26.0 (estimate)

June empire state manufacturing survey released at 8:30am EST: 19.8 (actual) vs. 5.0 (estimate)

May industrial production to be released at 9:15am EST: +0.2% (estimate)

May capacity utilization to be released at 9:15am EST: 76.8% (estimate)

June housing market index to be released at 10:00am EST: 70 (estimate)

Happy trading!

Tom