Market Recap for Monday, April 16, 2018

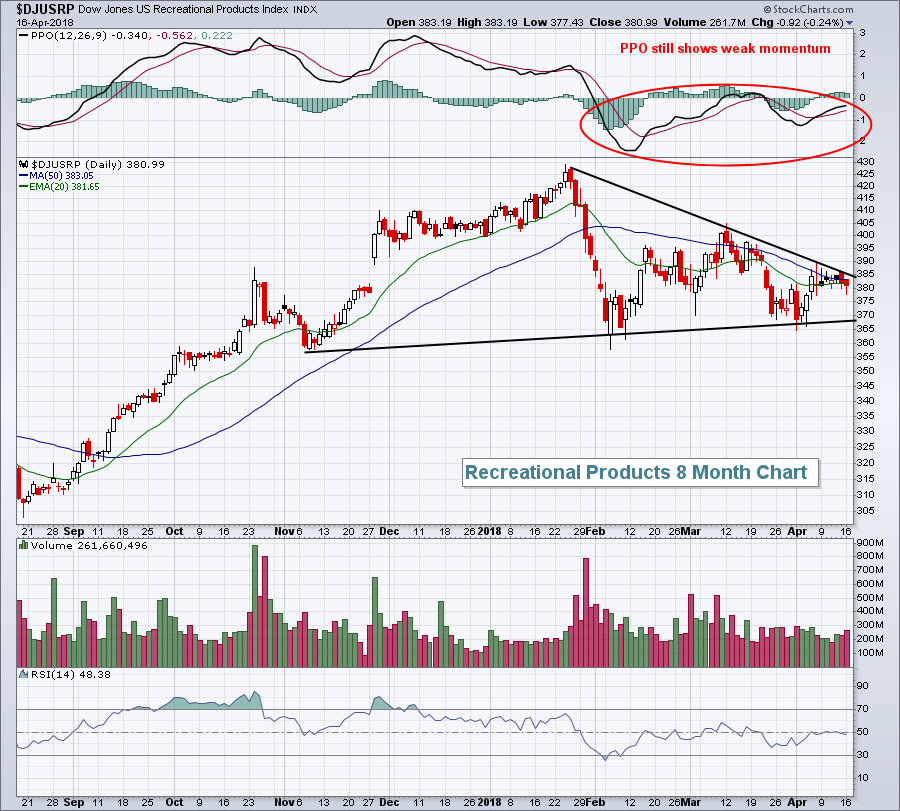

Utilities (XLU, +1.37%) and materials (XLB, +1.34%) led rather odd market behavior on Monday. The good news is that all nine sectors finished higher. The bad news is that our most aggressive sectors struggled on a relative basis. Financials (XLF, +0.44%) continued to suffer from an uninspired banking group ($DJUSBK, -0.03%). Recreational products ($DJUSRP) were the weakest part of consumer discretionary (XLY, +0.75%) as that group can't quite make up its mind whether it wants to break out or break down:

The 20 day EMA and 50 day SMA are very close to one another, highlighting the indecision taking place right now. We do remain in a bull market, however, so I'd favor a breakout to the upside in the coming days/weeks.

The 20 day EMA and 50 day SMA are very close to one another, highlighting the indecision taking place right now. We do remain in a bull market, however, so I'd favor a breakout to the upside in the coming days/weeks.

Software ($DJUSSW) had a strong day in technology, gaining 1.07% on Monday. But its hourly chart is showing mixed signals as it approaches fairly important short-term price resistance established on the March 27th opening gap and selloff:

There's a bit of a momentum issue with software (neg divergence), but I believe the more important issue is overhead resistance just above 2020. If the DJUSSW can negotiate that level with gusto, I'd expect to see the PPO regain its strength and clear earlier highs.

There's a bit of a momentum issue with software (neg divergence), but I believe the more important issue is overhead resistance just above 2020. If the DJUSSW can negotiate that level with gusto, I'd expect to see the PPO regain its strength and clear earlier highs.

Pre-Market Action

Netflix (NFLX) impressed traders last night with its quarterly earnings report and the stock is up nearly 7% in pre-market trade. Housing starts and building permits for March easily beat expectations. That combination is aiding already strong pre-market action as Dow Jones futures are higher by 200 points as we get set for another open on Wall Street. Homebuilders ($DJUSHB) should get a nice lift from the bullish housing report this morning.

Global markets are mixed. Overnight in Asia, we saw mostly lower indices as traders digested economic data in China. This morning, European markets are moving higher with notable strength in Germany. The German DAX ($DAX) was up 0.76% at last check.

Current Outlook

Here's perhaps the best news of all. The Volatility Index ($VIX) continues to creep lower and lower. A high VIX environment is a necessary ingredient of a bear market. The stock market must remain on edge for sellers to establish control. We've seen that since late-January/early-February. But the volatility tide appears to be turning and that's a huge plus for the bulls, especially if the VIX can clear the lows established on the last S&P 500 rally in early March:

The VIX is at its lowest level in a month, which is a sign of returning complacency. Complacency helps to drive bull markets as the stock market begins to routinely overlook or ignore bad news. This is the sentiment side of technical analysis. But nothing overrules price action. During the last bout of selling, in which we printed a double bottom, there was a significant gap down in the S&P 500 that has not been cleared and that looms large for the bulls:

The VIX is at its lowest level in a month, which is a sign of returning complacency. Complacency helps to drive bull markets as the stock market begins to routinely overlook or ignore bad news. This is the sentiment side of technical analysis. But nothing overrules price action. During the last bout of selling, in which we printed a double bottom, there was a significant gap down in the S&P 500 that has not been cleared and that looms large for the bulls:

The S&P 500 has multiple obstacles ahead:

The S&P 500 has multiple obstacles ahead:

(1) Clearing its 50 day SMA, currently at 2687

(2) Negotiating the top (2712) and bottom (2691) of gap resistance, and

(3) Breaking above trendline resistance at approximately 2730

So the range to watch is from 2687-2730, which is identified on the chart above as roughly a 1.7% swath of resistance. Clearing all of the above while the VIX drops back beneath the March low would be great technical developments for the current bull market.

Sector/Industry Watch

Many had written off homebuilders ($DJUSHB) as their chart had deteriorated significantly in 2018. But when a group outperforms like the DJUSHB did in 2017 (it was the second best performing industry group last year), it needs time to consolidate and gather itself before it can potentially resume that upward thrust. I believe that's exactly what's occurred with the DJUSHB. I featured a homebuilding stock in my Monday Setups yesterday and the group should do quite well today with solid fundamental news out this morning:

The 2017 strength was slowed with the emergence of a negative divergence. That led to a scary decline, but note that the recent bottom printed a positive divergence. That, along with the double bottom, sets major price support just beneath 800. Violation of that support level would completely alter the bullish technical picture here. I expect to see a resumption of earlier 2017 strength.

The 2017 strength was slowed with the emergence of a negative divergence. That led to a scary decline, but note that the recent bottom printed a positive divergence. That, along with the double bottom, sets major price support just beneath 800. Violation of that support level would completely alter the bullish technical picture here. I expect to see a resumption of earlier 2017 strength.

There are many who would argue that the potential of higher interest rates would be a head wind for home construction. Keep in mind, however, that interest rates remain extremely low historically-speaking. I don't see interest rates as a problem at this point, so long as economic strength supports the higher rates.

Historical Tendencies

I've discussed homebuilders quite a bit today, so let's take a look at the group's seasonal behavior. April is a very strong month for home construction as the DJUSHB has averaged rising 2.1% during April over the past two decades. The bad news? May and June have historically been the weakest two consecutive calendar months, posting average monthly losses of -1.5% and -1.6%, respectively. The DJUSHB has risen more often that it's fallen during both months as gains have been realized in 56% of these months. But when the group has been weak, it's been really weak.

In the short-term, I really like the DJUSHB to get back on its bullish track. As April comes to a close in a couple weeks, we'll re-evaluate.

Key Earnings Reports

(actual vs. estimate):

CMA: 1.59 vs 1.49

GS: 6.95 vs 5.67

JNJ: 2.06 vs 2.01

NTRS: 1.61 vs 1.42

OMC: 1.14 vs 1.05

PGR: 1.18 (estimate, still awaiting results)

PLD: .80 vs .74

UNH: 3.04 vs 2.92

(reports after close, estimate provided):

CSX: .66

IBKR: .56

IBM: 2.40

ISRG: 1.99

LRCX: 4.36

UAL: .49

Key Economic Reports

March housing starts released at 8:30am EST: 1,319,000 (actual) vs. 1,264,000 (estimate)

March building permits released at 8:30am EST: 1,354,000 (actual) vs. 1,315,000 (estimate)

March industrial production to be released at 9:15am EST: +0.4% (estimate)

March capacity utilization to be released at 9:15am EST: 78.0% (estimate)

Happy trading!

Tom