Market Recap for Wednesday, April 11, 2018

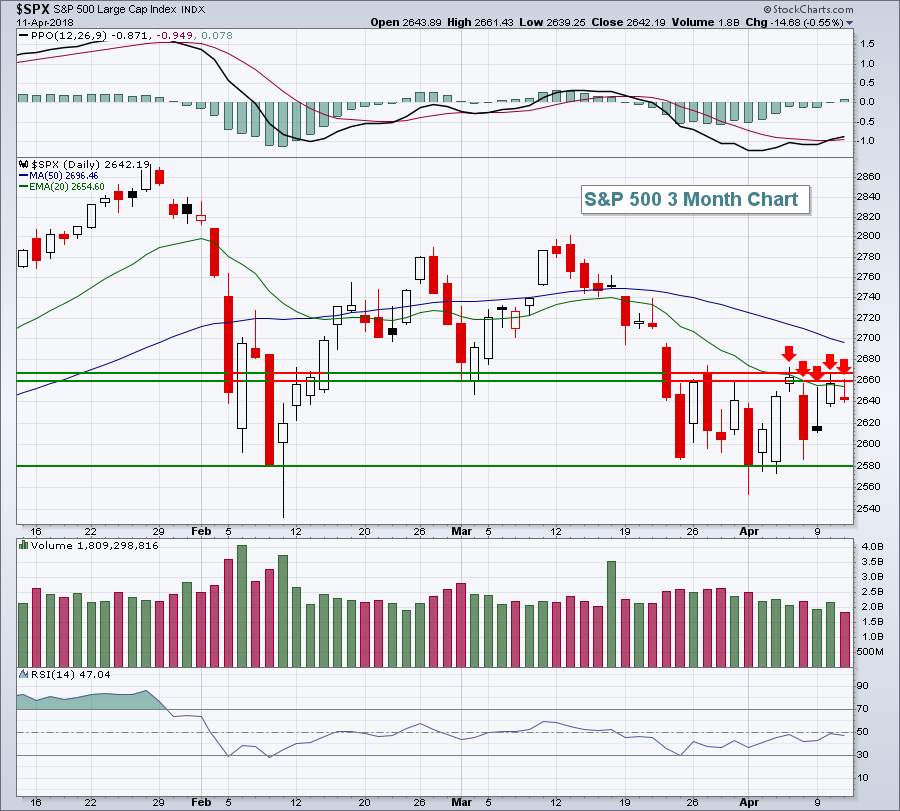

Well, the S&P 500 tried to clear its 20 day EMA again. And it failed....again. That marks the 5th consecutive day of failed 20 day EMA breakouts. Given that futures are higher this morning, this benchmark index appears headed for a 6th consecutive test. Here's the current view:

There's been a lot of news lately regarding trade threats, missile threats, upcoming earnings, volatility, etc. But what I'm focusing on are the technicals. I believe the 9 year bull market remains quite sustainable so a break above the 20 day EMA would be the first signal of technical repair.

There's been a lot of news lately regarding trade threats, missile threats, upcoming earnings, volatility, etc. But what I'm focusing on are the technicals. I believe the 9 year bull market remains quite sustainable so a break above the 20 day EMA would be the first signal of technical repair.

Energy (XLE, +1.04%) was the only sector able to finish in positive territory yesterday as crude oil prices ($WTIC) closed at a level not seen since December 2014. Higher crude oil prices provide solid tailwinds for energy stocks and that's beginning to show up on the chart:

I would expect to see energy continue to lead the market given the breakout in crude oil prices.

I would expect to see energy continue to lead the market given the breakout in crude oil prices.

Relative weakness was found yesterday in financial stocks (XLF, -1.19%) ahead of key earnings reports later this week. Asset managers ($DJUSAG) had a particularly rough day ahead of Blackrock's (BLK) earnings report this morning. Banks ($DJUSBK) did the same ahead of key earnings reports from Bank of the Ozarks (OZRK) and Commerce Bancshares (CBSH). All three of these stocks handily beat earnings expectations. Will buyers return? That'll be a key question to be answered in today's session.

Pre-Market Action

Gold ($GOLD) is down $14 per ounce this morning, backing off of significant overhead resistance close to $1360. Crude oil prices ($WTIC) have also retreated after setting 3 1/4 year highs on Wednesday. Asian markets were fractionally lower overnight, while European markets are mixed this morning.

U.S. futures are poised for another early push higher as Dow futures look set to open up 138 points higher with 45 minutes left to today's opening bell.

Current Outlook

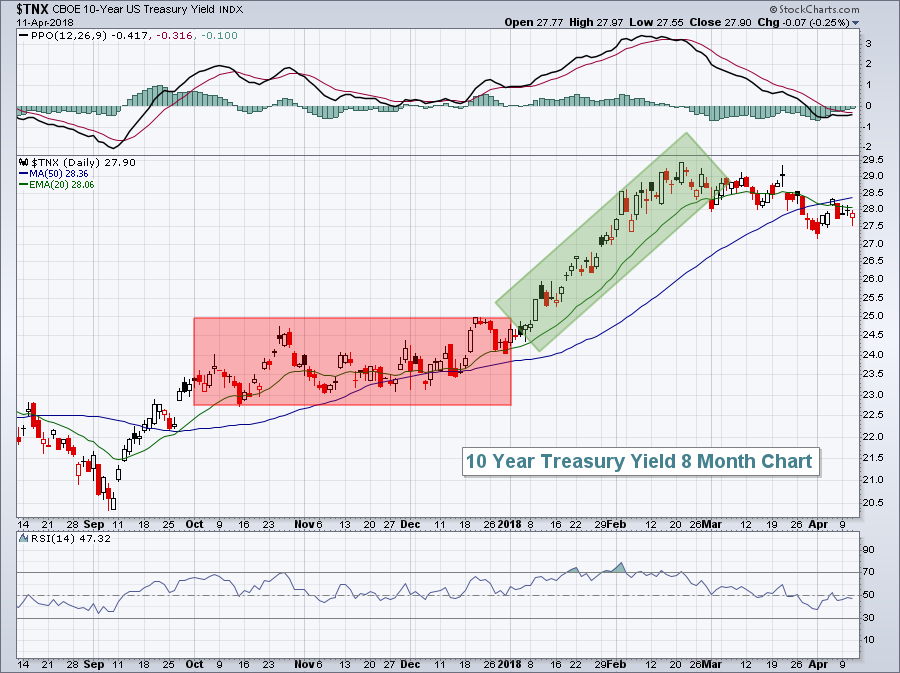

The 10 year treasury yield ($TNX) is a major driver for bank earnings. One year ago, the TNX stood near 2.20%. Today the TNX, even after consolidating for the past several weeks, resides near 2.80%. That increase in yield represents HUGE tailwinds for financials in general, and banks more specifically. It's no surprise that the financial ETF (XLF, +19.06%) ranks in second position over the last year. Only technology (XLK, +26.43%) has performed better.

Since topping in February near 2.95%, the TNX has been drifting lower. Continuing such a move lower would not be good for bank earnings in Q2 so it'll be very important to listen to the guidance from the big banks tomorrow morning. But looking at Q1 earnings, I expect to see more earnings blowouts like the two we saw this morning (see Key Earnings Reports section below). The reason? A much higher TNX throughout Q1. Take a look:

It's pretty clear to me that the TNX had a gigantic trend higher during Q1. That will translate into strong profit growth for banks. Again, we've already seen that in two small bank earnings reports this morning and we're likely to see this trend continue tomorrow morning with the likes of JPM, PNC and others.

It's pretty clear to me that the TNX had a gigantic trend higher during Q1. That will translate into strong profit growth for banks. Again, we've already seen that in two small bank earnings reports this morning and we're likely to see this trend continue tomorrow morning with the likes of JPM, PNC and others.

Sector/Industry Watch

Here's a long-term 10 year weekly chart of the banks:

First, the green shaded area highlights the strong positive correlation between the DJUSBK and TNX. The gray shaded area in the RSI suggests that pullbacks during the 6 year uptrend channel have represented excellent entry into bank stocks. The weekly RSI is currently in this RSI "buy zone" from 40-50 as it resides at 49. Future performance of banks will likely be determined, at least in large part, by the direction of the TNX. Simply moving back to 2.95% or to 3.05% to test highs reached a few years back would be a tailwind for banks. Based on everything the Fed has discussed, I fully expect we'll see the TNX rise to accompany improving economic conditions. That would be a major catalyst for banks during the balance of 2018.

First, the green shaded area highlights the strong positive correlation between the DJUSBK and TNX. The gray shaded area in the RSI suggests that pullbacks during the 6 year uptrend channel have represented excellent entry into bank stocks. The weekly RSI is currently in this RSI "buy zone" from 40-50 as it resides at 49. Future performance of banks will likely be determined, at least in large part, by the direction of the TNX. Simply moving back to 2.95% or to 3.05% to test highs reached a few years back would be a tailwind for banks. Based on everything the Fed has discussed, I fully expect we'll see the TNX rise to accompany improving economic conditions. That would be a major catalyst for banks during the balance of 2018.

Historical Tendencies

We're currently in the seasonal sweet spot for banks ($DJUSBK). I mention this because this morning a couple of small banks, Bank of the Ozarks (OZRK) and Commerce Bancshares (CBSH), beat their Wall Street EPS estimates and tomorrow morning, we'll hear from four behemoth banks - JP Morgan Chase (JPM), Bank of America (BAC), Wells Fargo (WFC) and PNC Financial Services (PNC) - as Q1 earnings season really begins to kick in.

March, April and May have produced average DJUSBK monthly returns of 2.7%, 2.1% and 0.8%, respectively, over the past two decades. That is, by far, the strongest three consecutive calendar month stretch for banks. We also remain in an environment that favors higher interest rates, which historically coincide with higher bank profits.

Key Earnings Reports

(actual vs. estimate):

BLK: 6.70 vs 6.42

DAL: .74 vs .73

CBSH: .92 vs .80

OZRK: .88 vs. 85

Key Economic Reports

Initial jobless claims released at 8:30am EST: 233,000 (actual) vs. 230,000 (estimate)

Happy trading!

Tom