Market Recap for Wednesday, July 11, 2018

Utilities (XLU, +0.90%) moved higher in an otherwise down day, highlighted by the latest trade headlines in which the U.S. announced another $200 billion in Chinese imports to be subject to a 10% tariff. While the initial reaction was obviously negative, the major U.S. indices did hold up well after the opening bell, most likely due to a Volatility Index ($VIX) that had drifted lower to 12.50 over the past two weeks. Stocks tend to hold up much better to bad news when the VIX is low. I view it as a signal that the market is following technical indications, not fundamental news. The Dow Jones fell to 24750 in the opening 10 minutes and was still at 24750 just minutes before the closing bell. There was very little panic associated with the latest trade news as the market grows more comfortable with the rhetoric.

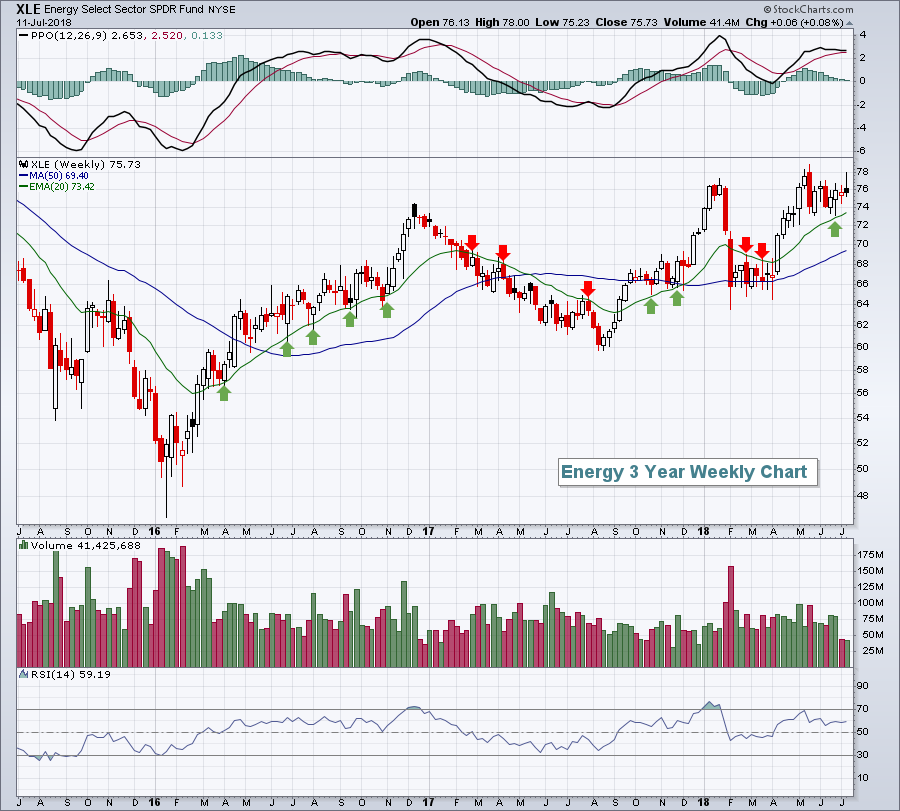

One day after successfully negotiating short-term price resistance at 77, the volatile energy sector (XLE, -2.12%) lost that support as crude oil prices ($WTIC) fell a steep 5.03% to just above $70 per barrel. However, the XLE is still holding onto more significant intermediate-term support at the 20 week EMA:

Over the past few years, you can see how important it has been to hold onto rising 20 week EMA support (green arrows) during uptrends. The opposite has held true during downtrends where the red arrows show the declining 20 day EMA holding as resistance.

Pre-Market Action

The 10 year treasury yield ($TNX) is up 2 basis points this morning at 2.86% and once again knocking on the door of 20 day EMA resistance. A breakout there would be important for financials, especially as four major banks get set to report their quarterly earnings tomorrow morning before the bell. Crude oil ($WTIC) is rebounding from yesterday's big selloff, approaching $71 per barrel.

Global markets were up overnight and are up this morning. That is lifting the spirits here in the U.S. after a rough day on Wednesday. Dow Jones futures are currently higher by 188 points with roughly an hour to go to the opening bell.

Netflix (NFLX) was downgraded by UBS Securities on valuation concerns this morning, indicating that good news is already priced into the stock. Traders don't seem to care much as NFLX trades down only fractionally in pre-market. Earnings and guidance next week will likely determine whether NFLX is fairly priced. Meanwhile, Twitter (TWTR) shares are on the rise in pre-market on positive comments from Goldman Sachs (GS).

Current Outlook

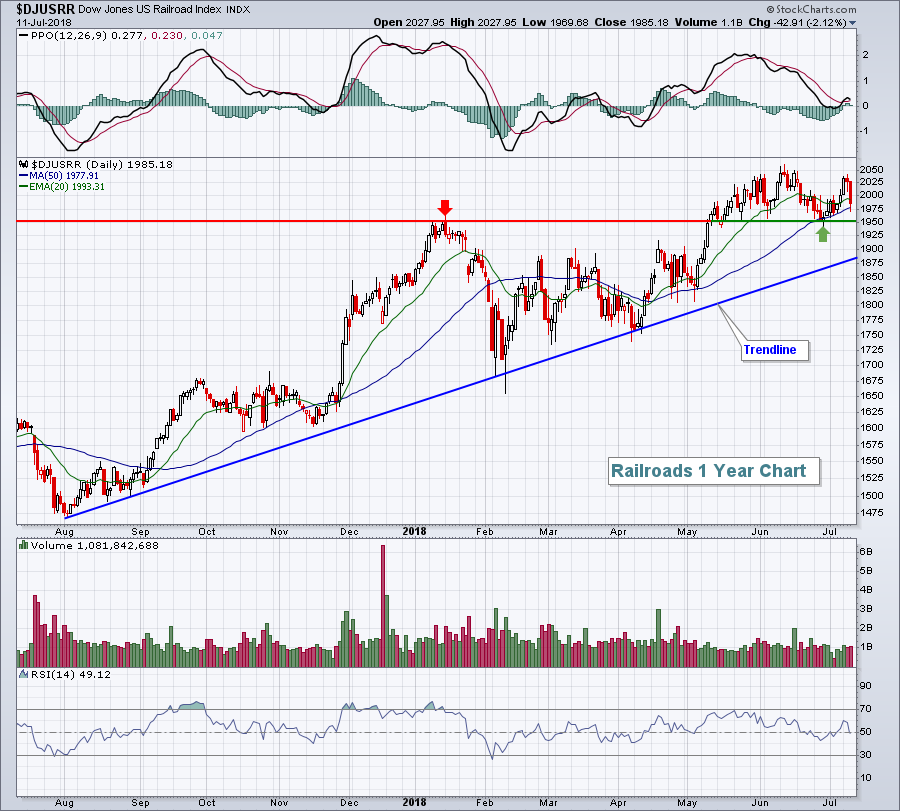

The May breakout in the Dow Jones U.S. Railroad Index ($DJUSRR) should be viewed as a bullish sign for the U.S. economy looking ahead. We've since seen a pullback to test price support and now the DJUSRR is range-bound:

The red arrow marked the earlier price high (resistance), which was cleared in May. That level then became support (green arrow). As a result, the DJUSRR is now trading between 1950 and 2050. If short-term price support is lost at 1950, then trendline support becomes extremely important as this trendline has been successfully tested on several occasions.

The red arrow marked the earlier price high (resistance), which was cleared in May. That level then became support (green arrow). As a result, the DJUSRR is now trading between 1950 and 2050. If short-term price support is lost at 1950, then trendline support becomes extremely important as this trendline has been successfully tested on several occasions.

Sector/Industry Watch

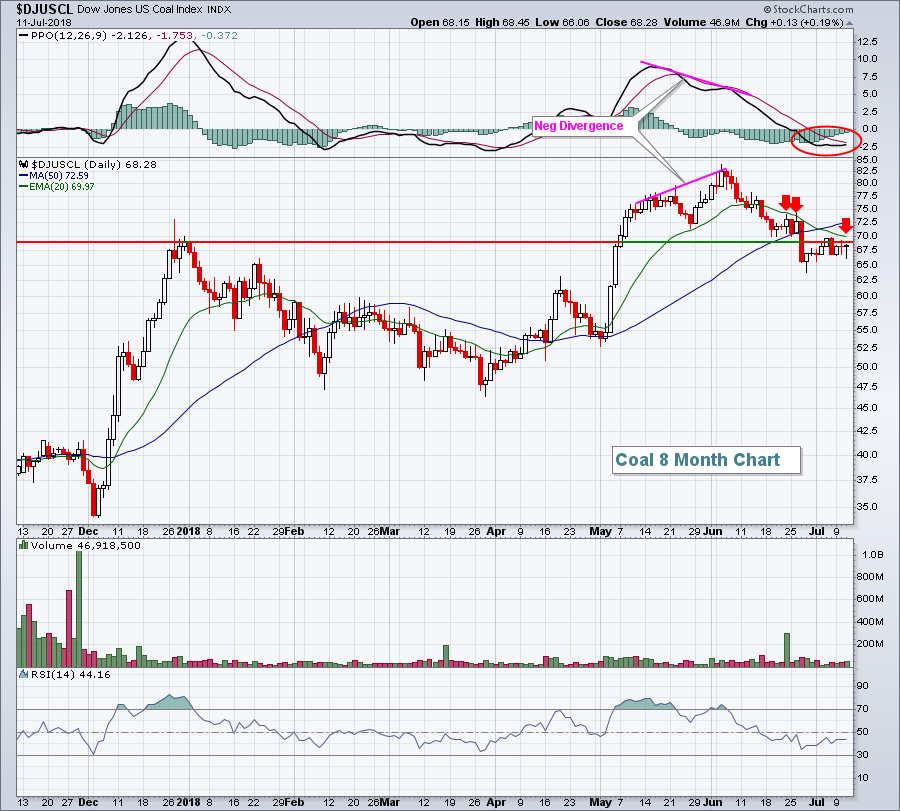

The Dow Jones U.S. Coal Index ($DJUSCL) has had an up and down 2018 and is virtually flat year-to-date. But technical conditions have clearly taken a turn for the worse since early June when a negative divergence printed. Here's the latest look:

The pullback to the 50 day SMA was healthy, as was the PPO returning to centerline support. But the selling didn't stop there. Both of those were lost, as was price support. Now we're seeing failures on bounces at the now-declining 20 day EMA.

The pullback to the 50 day SMA was healthy, as was the PPO returning to centerline support. But the selling didn't stop there. Both of those were lost, as was price support. Now we're seeing failures on bounces at the now-declining 20 day EMA.

Historical Tendencies

History supports the notion that we've seen a top in the DJUSCL. Over the past two decades, here are the average monthly returns by the following calendar months:

June: -3.8%

July: -3.9%

August: -1.2%

September: -4.8%

Key Earnings Reports

(actual vs. estimate):

DAL: 1.77 vs 1.72

Key Economic Reports

June CPI to be released at 8:30am EST: +0.2% (estimate)

June Core CPI to be released at 8:30am EST: +0.2% (estimate)

Initial jobless claims to be released at 8:30am EST: 225,000 (estimate)

Happy trading!

Tom