Market Recap for Friday, November 9, 2018

There was a return of strength in defensive sectors on Friday as consumer staples (XLP, +0.58%), utilities (XLU, +0.15%) and real estate (XLRE, +0.12%) were the only sectors to finish the session in positive territory. There was also significant relative weakness in the more aggressive NASDAQ and Russell 2000, which retreated 1.65% and 1.82%, respectively. The relative laggards were familiar names from October - communication services (XLC, -2.05%), technology (XLK, -1.73%), materials (XLB, -1.40%) and consumer discretionary (XLY, -1.39%). Materials are discussed in further detail below in the Sector/Industry Watch section.

As for communication services, the culprit dragging the sector lower once again was internet ($DJUSNS, -1.64%), although publishing ($DJUSPB, -2.69%) stocks were quite weak as well. Over the past three months, the DJUSNS has fallen 16.44%. No other industry group in the space has lost more than 6% and a couple - mobile telecommunications ($DJUSWC, +9.84%) and media agencies ($DJUSAV, +9.49%) - have been exceptionally strong. Internet is the weak link. The DJUSWC has broken to fresh decade-long highs, led by SBA Communications (SBAC) and T-Mobile (TMUS). The latter attempted a breakout last week, but couldn't quite make it:

Given the strength in the group, it's likely just a matter of time before TMUS breaks to new highs.

Given the strength in the group, it's likely just a matter of time before TMUS breaks to new highs.

Pre-Market Action

The U.S. Dollar Index ($USD) is rallying along with crude oil ($WTIC), which is trying to snap a 10 session losing streak. The WTIC is up 1.31% to $60.98 per barrel at last check. Asian markets were mostly fractionally higher overnight, although the China Shanghai Composite ($SSEC) gained more than 1% to lead. In Europe this morning, prices are mostly lower with relative weakness in Germany as the German DAX ($DAX) retreats more than 1.3%.

Dow Jones futures are lower by 66 points with a bit more than 30 minutes to the opening bell.

Current Outlook

There's always been an interesting correlation between copper prices ($COPPER) and the S&P 500. They tend, more often than not, to move in the same direction. It's certainly not a perfect correlation, but there's common sense as to why there should be some positive correlation. Unlike silver ($SILVER) and especially gold ($GOLD), copper is much more closely aligned with global growth and demand. If our global economy is expanding, demand for copper should increase. Therefore, prices should rise. Copper is more heavily impacted by economic conditions and less by movement of the U.S. Dollar ($USD). If we take a look at the correlation coefficient, what we see is not very encouraging:

The blue shaded area above represents times when copper and the S&P 500 are positively correlated and moving in the same direction. The red shaded areas show the two moving in opposite directions. I think it's pretty clear from the analysis above that copper prices and the S&P 500 do tend to move in the same direction. We've seen only four prior occasions over the past two decades where the negative correlation has reached -0.75. Two of those times, in 1999 and 2007, the S&P 500 was rising while copper prices were declining. In both instances, we began an S&P 500 bear market within a year. The 2008 negative correlation was different in that copper prices were rising while the S&P 500 was falling. Perhaps not too surprisingly, the S&P 500 found its bear market bottom roughly a year later. The only negative correlation that didn't seem to matter was the 2013 instance. Now here we are again in 2018 with falling copper prices while the S&P 500 remains fairly close to its all-time high.

The blue shaded area above represents times when copper and the S&P 500 are positively correlated and moving in the same direction. The red shaded areas show the two moving in opposite directions. I think it's pretty clear from the analysis above that copper prices and the S&P 500 do tend to move in the same direction. We've seen only four prior occasions over the past two decades where the negative correlation has reached -0.75. Two of those times, in 1999 and 2007, the S&P 500 was rising while copper prices were declining. In both instances, we began an S&P 500 bear market within a year. The 2008 negative correlation was different in that copper prices were rising while the S&P 500 was falling. Perhaps not too surprisingly, the S&P 500 found its bear market bottom roughly a year later. The only negative correlation that didn't seem to matter was the 2013 instance. Now here we are again in 2018 with falling copper prices while the S&P 500 remains fairly close to its all-time high.

Are the falling copper prices going to signal the beginning of a new bear market ahead? It's certainly possible. I have drawn a rising trendline that connects the prior two price lows in copper. If that's violated, then I'd grow much more cautious. For now, however, I'd simply chalk this signal up in the bear market column and continue to evaluate ALL signals as we move forward.

Sector/Industry Watch

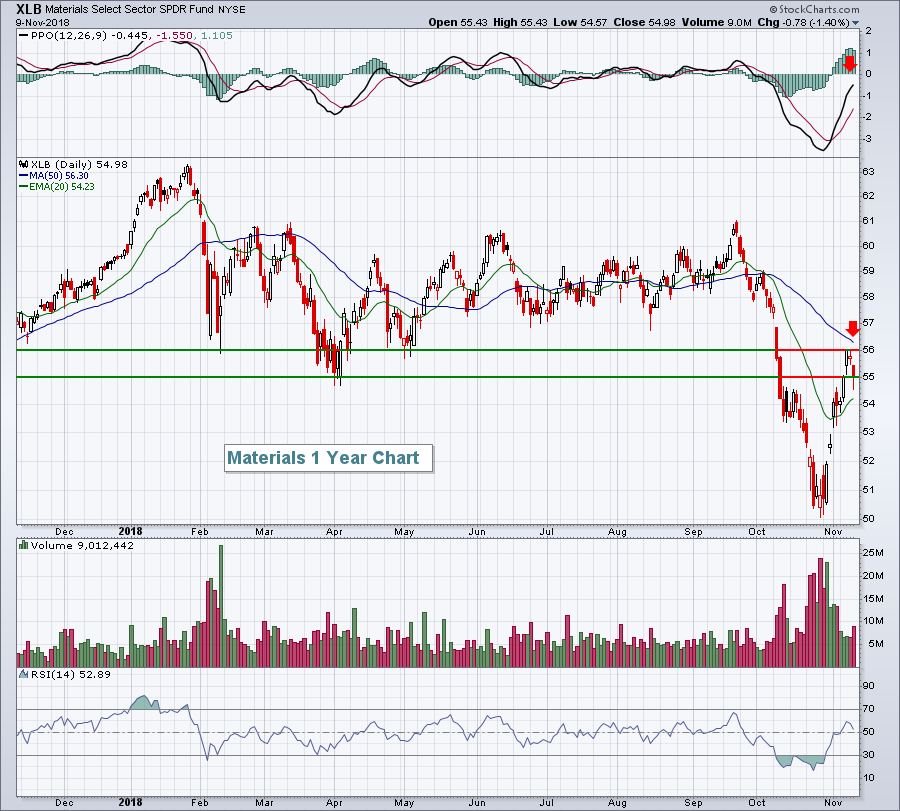

Basic materials (XLB) backed off of overhead price resistance last week and the rising U.S. dollar ($USD) will not help the group. Here's last week's reversal on the XLB:

The XLB certainly could push through overhead price resistance at any time, but the PPO and price action turning lower beneath PPO centerline and 50 day SMA resistance (red arrows) doesn't bode well for the sector. And as I mentioned above, the USD has been quite strong and I'm expecting it to strengthen further. That is likely to keep a lid on the XLB's relative performance (vs. the S&P 500) and likely its absolute performance.

The XLB certainly could push through overhead price resistance at any time, but the PPO and price action turning lower beneath PPO centerline and 50 day SMA resistance (red arrows) doesn't bode well for the sector. And as I mentioned above, the USD has been quite strong and I'm expecting it to strengthen further. That is likely to keep a lid on the XLB's relative performance (vs. the S&P 500) and likely its absolute performance.

Monday Setups

Last week's setups performed quite well, so the bar is raised as I look to find a fresh list of potential trades in the week ahead. I'm going to start with a $540 million communication services company. Communication services (XLC) has been the weakest sector of late, so this one might be a bit of a stretch. However, they've clearly been outperforming their peers and just reported quarterly earnings that included the following:

Revenues: $217.4 mil (actual) vs. $214.9 mil (estimate)

EPS: (.47) vs (.71)

Yes, they reported a sizable loss, but much less than expected. The market reaction, which is what I watch most closely, was excellent with GOGO jumping more than 26% on the session after earnings. GOGO has since sold off and isn't far from the top of gap support now:

Adding in the gap support zone of just above it sets up a very nice reward to risk trade. This is a small stock and carries more risk than larger cap stocks, but for those interested in small caps, this one looks solid.

Adding in the gap support zone of just above it sets up a very nice reward to risk trade. This is a small stock and carries more risk than larger cap stocks, but for those interested in small caps, this one looks solid.

For all of this week's trade setups, CLICK HERE.

Historical Tendencies

Over the past 68 years (since 1950), the S&P 500 has the tendency to trend a bit lower in the middle part of November. Early November and late November is quite bullish historically, but the 6th through the 20th has produced annualized returns of -5.99%. So while the stock market is free to do whatever it wants, just keep in mind that typical Q4 seasonal tailwinds haven't really applied through the early part of next week.

Key Earnings Reports

(actual vs. estimate):

ATHM: .90 vs .84

(reports after close, estimate provided):

EQH: .90

UGI: (.04)

Key Economic Reports

None

Happy trading!

Tom