Market Recap for Thursday, March 28, 2019

Lululemon Athletica (LULU, +14.13%), PVH Corp (PVH, +14.76%), and Movado Group (MOV, +22.77%) all surged after the clothing & accessories retailers all posted much better than expected quarterly earnings. The Dow Jones U.S. Clothing & Accessories Index ($DJUSCF, +5.10%) stormed higher and closed at its highest level since early November. The DJUSCF has more work to do, but yesterday was a very good start as the DJUSCF made a relative trendline breakout vs. the benchmark S&P 500:

Despite the strength in this industry group, the consumer discretionary sector (XLY, +0.60%) as a whole was just middle of the pack on Thursday. Leadership came in the form of materials (XLB, +0.97%) as specialty chemicals ($DJUSCX, +1.28%) and commodity chemicals ($DJUSCC, +1.14%) both gained more than 1%. The most surprising part of this was that the U.S. Dollar Index ($USD, +0.50%) had a very solid day. Materials tend to outperform when the USD is falling.

Despite the strength in this industry group, the consumer discretionary sector (XLY, +0.60%) as a whole was just middle of the pack on Thursday. Leadership came in the form of materials (XLB, +0.97%) as specialty chemicals ($DJUSCX, +1.28%) and commodity chemicals ($DJUSCC, +1.14%) both gained more than 1%. The most surprising part of this was that the U.S. Dollar Index ($USD, +0.50%) had a very solid day. Materials tend to outperform when the USD is falling.

Our major indices all finished with gains, although it was a roller coaster ride throughout the session. We saw an early move higher, followed by considerable selling that wiped out those early gains. But it was mostly buying pressure throughout the afternoon session as the small cap Russell 2000 ($RUT, +0.85%) led on a relative basis for the third consecutive day.

Pre-Market Action

Dow Jones futures are on the move higher, rising 130 points at last check this morning. This is accompanying one of the few times this month that we've seen money rotate away from the defensive treasuries. Lower treasury prices result in higher treasury yields. The 10 year treasury yield ($TNX) is up 3 basis points to 2.42% in early action.

Crude oil prices ($WTIC) are up nearly 2% and currently trade at $60.46 per barrel. On an intraday basis, this is the highest that crude has traded since November 12th. We're all seeing the effects of this at the pump each and every day. Here in South Carolina, we've seen gas prices rise 20% over the past month.

Overnight, the Shanghai Composite ($SSEC) surged 3.20% as more positive rumors swirled regarding US-China trade talks. That strength carried over into Europe, where the German DAX ($DAX) is up nearly 1% this morning.

Current Outlook

I mentioned on MarketWatchers LIVE yesterday that we've seen the 10 year treasury yield ($TNX) clear its prior day highs only twice during the month of March. It's been a steady downtrend as money has rotated heavily into the more defensive treasury market. That's typically a bad sign for our economy on a forward-looking basis, but equity traders seem to be overlooking that fact and instead focusing on a much more dovish Fed. Still, it's good to see the TNX rising this morning, even if it's just a couple basis points:

We've been mired in a 5 month downtrend. Initially, it was problematic for equities as the Fed was discussing multiple rate hikes in 2019. Rising rates and a slowing economy is not exactly nirvana for stocks. But the Fed has come around and essentially said there'll be no rate hikes in 2019, possibly one in 2020. Many market pundits are beginning to think the Fed's next move could be a rate cut. Interest rates are already close to historic lows, so the thought of continuing cheap money seems to be exciting stock traders once again.

We've been mired in a 5 month downtrend. Initially, it was problematic for equities as the Fed was discussing multiple rate hikes in 2019. Rising rates and a slowing economy is not exactly nirvana for stocks. But the Fed has come around and essentially said there'll be no rate hikes in 2019, possibly one in 2020. Many market pundits are beginning to think the Fed's next move could be a rate cut. Interest rates are already close to historic lows, so the thought of continuing cheap money seems to be exciting stock traders once again.

Sector/Industry Watch

The financial sector (XLF, +0.87%) was the second-best performing sector on Thursday and the renewed strength may be happening just in time. The XLF carries the lowest SCTR among all of our major sector ETFs and could be in the midst of forming a reverse right shoulder in a bottoming reverse head & shoulders pattern:

The red circle highlights the daily PPO moving back into negative territory. The XLF is the only major sector ETF with a negative daily PPO, another sign of its relative weakness in 2019. However, let's keep an eye on this pattern. We know that rapidly-declining treasury yields are playing havoc with many financial stocks, especially banks ($DJUSBK) and life insurance companies ($DJUSIL). But, if we begin to see the TNX rise again, it could help to confirm the above reverse head & shoulders bottoming pattern. Ultimately, a closing breakout above 27.10-27.20 would be needed to confirm this reversal pattern.

The red circle highlights the daily PPO moving back into negative territory. The XLF is the only major sector ETF with a negative daily PPO, another sign of its relative weakness in 2019. However, let's keep an eye on this pattern. We know that rapidly-declining treasury yields are playing havoc with many financial stocks, especially banks ($DJUSBK) and life insurance companies ($DJUSIL). But, if we begin to see the TNX rise again, it could help to confirm the above reverse head & shoulders bottoming pattern. Ultimately, a closing breakout above 27.10-27.20 would be needed to confirm this reversal pattern.

Historical Tendencies

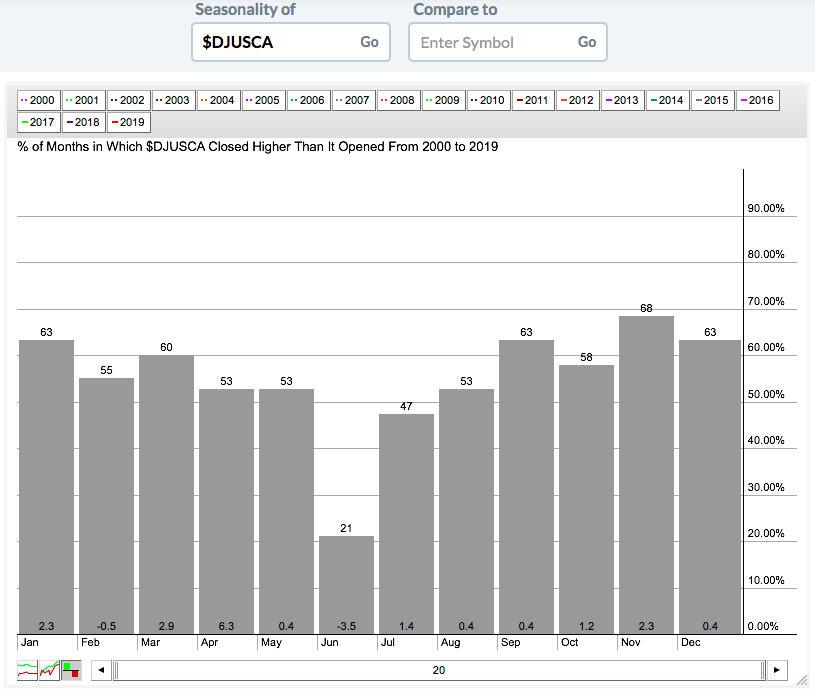

Gambling stocks ($DJUSCA) have not had a very good March thus far, but March and April have produced average monthly gains of +2.9% and +6.3%, respectively, over the past two decades:

Gains seem to occur at a higher frequency later in the year as the higher bars above would indicate, but the price strength has been much stronger as we head into Spring. We'll see if the DJUSCA can get back on track as we move into April.

Gains seem to occur at a higher frequency later in the year as the higher bars above would indicate, but the price strength has been much stronger as we head into Spring. We'll see if the DJUSCA can get back on track as we move into April.

Key Earnings Reports

(actual vs. estimate):

KMX: 1.13 vs 1.04

BB: .11 vs .04

Key Economic Reports

February personal income released at 8:30am EST: +0.2% (actual) vs +0.3% (estimate)

January personal spending released at 8:30am EST: +0.1% (actual) vs +0.3% (estimate)

March Chicago PMI to be released at 9:45am EST: 60.3 (estimate)

February new home sales to be released at 10:00am EST: 615,000 (estimate)

March consumer sentiment to be released at 10:00am EST: 97.8 (estimate)

Happy trading!

Tom