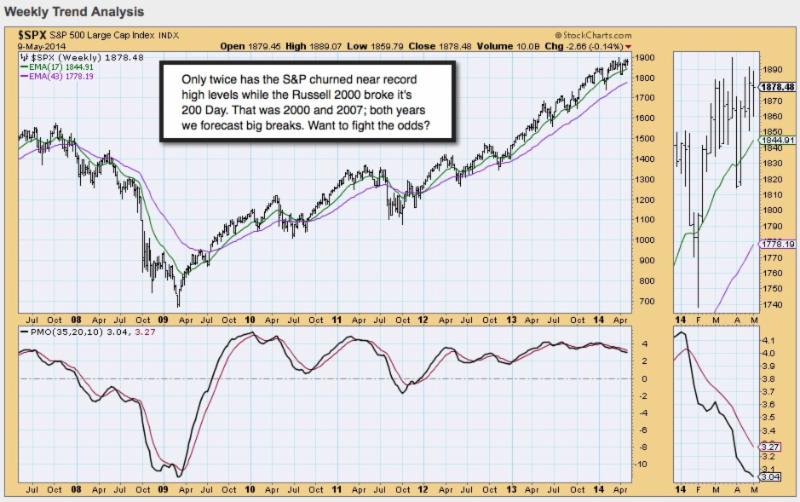

Who says they don't ring a bell at the top? Coincident with our 'inflection' June S&P short-sale early in March at the 1890 level; we proclaimed internally the high was at-hand, if not already behind for a few leading technology stocks.

Calling then for an 'A-B-C' decline, to be followed by a 'D' (rebound; expecting it as the defensive shift of funds into 'hiding places', as money struggled to find somewhere to 'park). That 'D' never fully-blossomed into a broad upward leg; in-spite of superficial appearances by 'some' Averages. That's part of a 'tired' market in terms of S&P; with NASDAQ hard-pressed to reflect rebounds within a persistently unfolding 'bear market' called for over two months ago. This isn't hindsight; but absolutely impacts what's envisioned forthcoming for laggards.

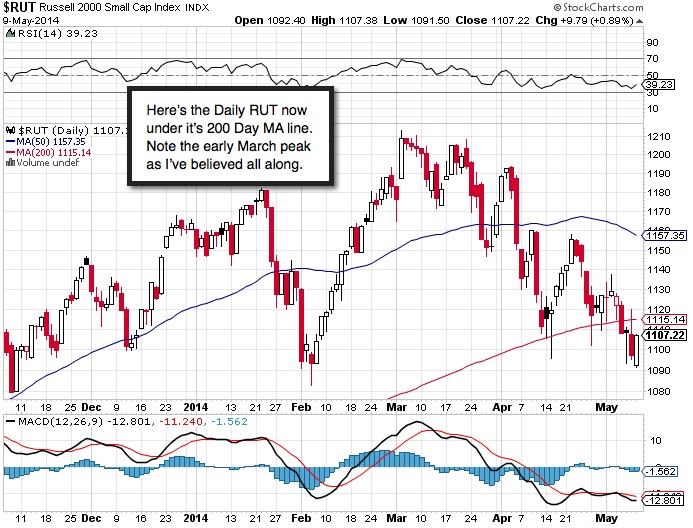

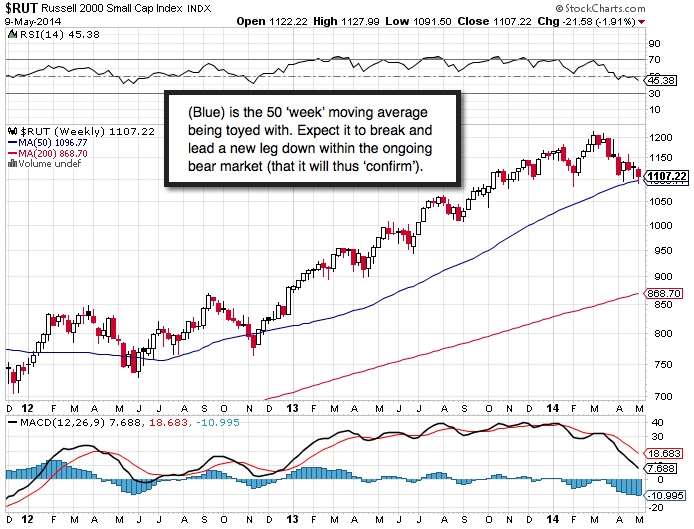

While this transpires, some pundits and analysts continue debating 'whether' a bubble exists in some sectors. Even Fed Chair Yellen questioned this in small cap stocks. Well, guess what? There's not much of a bubble in small-caps now; because that bubble was pricked back in March, as we'd outlined at the time.

So what we have is a perpetuated rush to safety (more so than yield), helped a good deal by the lower 10-year yield that so many pray continues (requiring of course no economic recovery of substance as we just roll-along), and answers the question as to the merit of investments for such reasons alone.

This assessment is based on 'facts' evident to anyone willing to look at reality, rather than delusion. What were some facts, outlined, and not hindsight? 'Tax changes' impacted a slew of sales late in 2012, which meant big boys couldn't repurchase shares at least until 30 days or early 2013; which couldn't be sold until 2014 (rotationally) to achieve a long-term capital gain. That's why I called for late 2013 upside absent heavy selling until 2014's 'brick-wall of resistance'.

Buybacks were seen as an 'enticing gimmick' that would inflate earnings when unaccompanied by greater profitability, allowing heavy insider sales, which we contended were a part of the 1st Quarter's action. This is not patting ourselves on the back; but rather setting-the-stage for understanding the evolution which has the next phase already internally well underway. Investment bankers knew this was occurring; advised clients contemplating IPO's to move quickly while they could still extract capital from investors.

The market is not at a high; it's been under-distribution for months; it's going to give an 'official' bear-market confirmation in the Nasdaq. This will occur 'after' many key stocks of this generation are off 20-40% or more. They rang a 'bell' in early March. The point is very important looking to the next phase, as what we have is not gravitating from growth to value, but from growth to 'parking places'.

Bottom-line: a single little technical observation summarizes where we stand. The only caveat: this has taken longer -and been more stealthy- because of so few alternatives for risk-averse investors, who have been compelled to pursue yield, when they really wish to be disengaged. We've alluded to this (clearly).

Enjoy the weekend!

Gene Inger

www.ingerletter.com