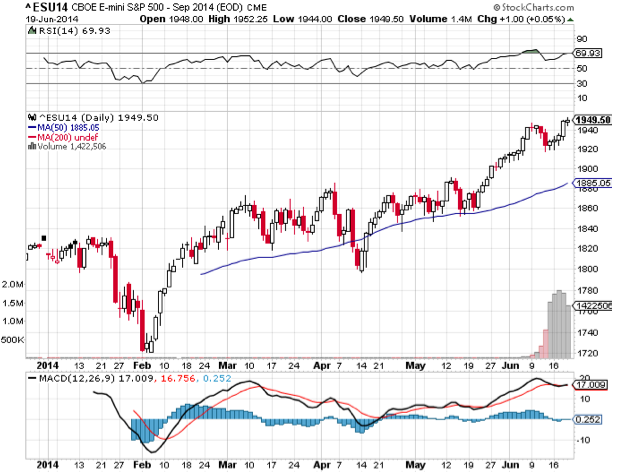

A utopian 'new neutral' - is not the case; nor is this pattern sustainable. For now there is no reason to scratch our heads about the market's behavior; as very little about it departs from follow-through after the post-Yellen panic yesterday, as well as Quarterly Expiration pressures; all of which reached an expected crescendo.

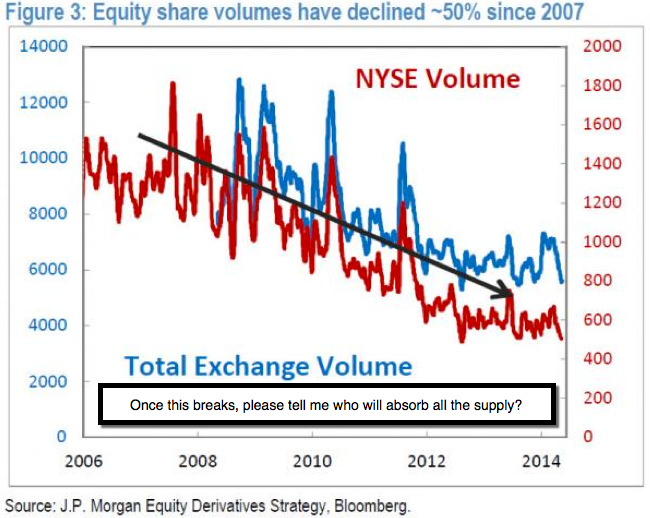

Whether this turns on a dime, or takes its time, this remains a period of danger. If one looks at the volume trends as the industry transforms and many use leverage to hold prices up (presumably while others exit or central-bank-stimulated buyers keep goosing it up), we will ponder anew what happens when the plug's pulled.

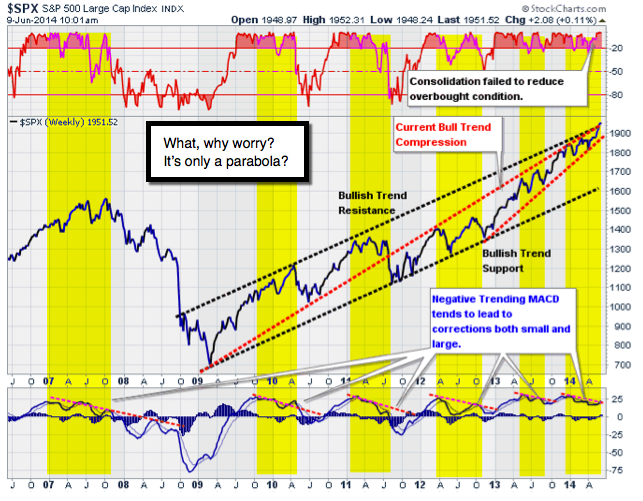

We see the current low volatility as disconnected from reality, and not a symptom of a protracted 'new neutral' forthcoming. Actually, 'new neurosis' is a more likely phenomenon, as those overloaded with equities might ponder 'how to exit' in the near future. Why is that different? Because we had really solid declines just a few months ago, but aware that it could hold if it merely adhered to frequently seen seasonal patterns.

Aside the outcome; the nearer term question is: where is the exit point? That's of course more than academic for traders; while for investors there's a couple varying approaches.

A flood of IPO's coming over the week ahead (will have noted effects). That, along with concern about Iraqi involvement; plus renewed focus (overdue) on Ukraine, where Russian tanks are on the move to the border yet-again, along with thousands of troops; will weigh on global concerns. In fact, while Gold and Silver had robust rallies in-line with renewed optimism of recent weeks (after having called the early 2014 rally and ensuing pullback), presumably on the back of inflationary fears; Easter Europe and flight capital aspects likely also contributed. We have leaned to a bullish side of metals (especially Silver) from the day they announced closing of the London 'Fix' this Summer.

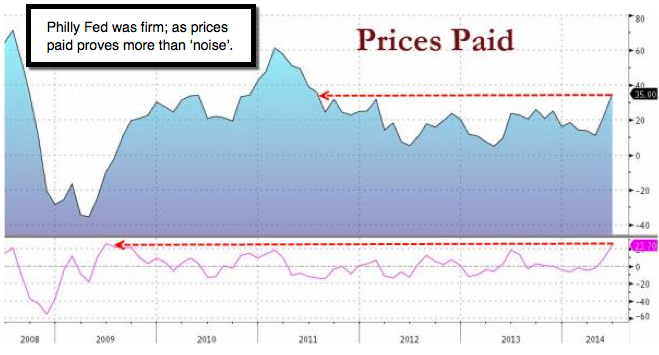

This week Oracle followed Caterpillar with 'misses' or shortfalls abroad. All this should serve as reminders that in the fullness of time, 'business' matters; not just Fed perceptions (or delusions); or implementation of heavy leverage. So will the mix of exploding 'global' (and domestic) debt, built-upon rising balance sheet central bank structures; prove unsustainable and toxic?

Liquidity or lack of it - is becoming a gradual issue in credit markets. This illiquidity must be observed concurrent with more 'out-front' crucial economic and geopolitical issues; as should a rapid credit market shift occur (as did early this week in London), it could evolve contrary to central bank assumptions.

Conclusion: shall I call this market a 'Great Insanity'? It's not a 'new neutral'; it's not the 'Epic Debacle' we called in 2007 coming after 5 years of persistent bullishness; but may set a stage for events a great deal more worrisome.

Enjoy the weekend!

Gene Inger

www.ingerletter.com