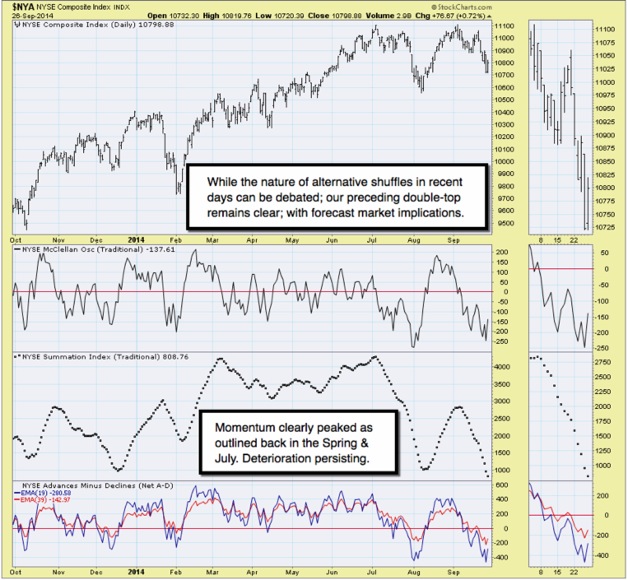

Conviction has been waning - for months, as Oscillators (Summation Index is a decent example) and major Indexes like the Russell and NY Composite have denoted. Eroding momentum was masked by the shuffle into big-caps; a large portion of which are multinational, and thus likely to see real earnings (not from buybacks) come in shy of goals (in-part due to our multi-month forecast Dollar strength and Euro weakness); beside the loss of business from relatively suppressed overseas/emerging markets.

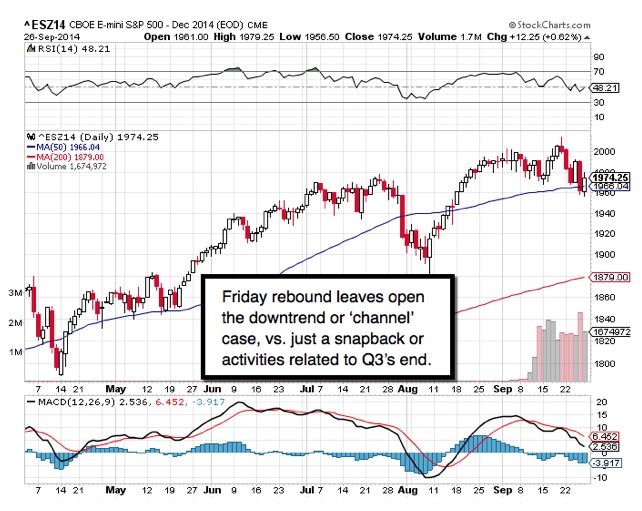

The week past saw extremely volatility in both directions; around key Moving Averages. No market transition occurs in a technical 'vacuum'; though this one has been extremely tenacious for many reasons. By the time S&P truly cracks, it will be after (the distribution long-described).

What's gone on last week; purge, bounce, plunge, snap-back, and even credit market jitters (High Yield plus Bill Gross's sudden exodus at PIMCO, which is itself more of a 'swan' (black or not) than markets realize (more).

It's really a 'Battle Royale', and it's being fought now.

That is the 'behavioral battle' that roils. It's blamed on everything from Rosh Hashanah, to Hedge Funds (end-of-Quarter regular settlements for sales in Q3 was Thursday; first day for Q4 buying was Friday); to now 'derivatives risks' stemming from possible outflows coming from PIMCO in the wake of Bill Gross resigning.

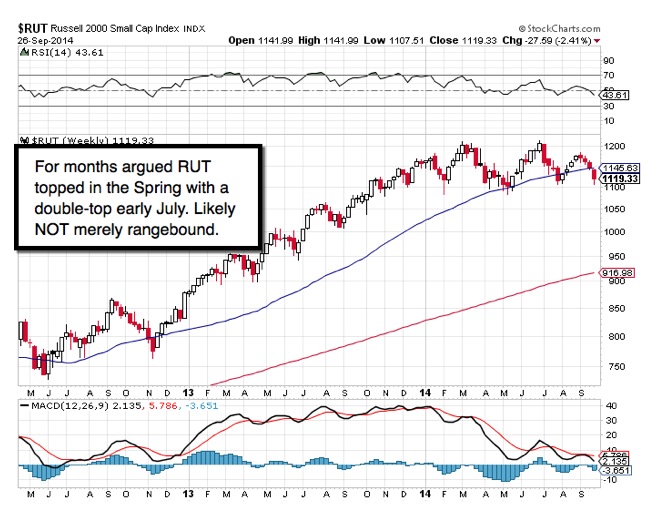

The Russell chart demonstrated that topping process through most of this challenging year. Though we focus on E-mini S&P trading; there is no doubt leverage or concentration in influential stocks helped the Averages resist capitulating or catching-down with the list.

Bottom-line: it remains a very dangerous market; (key points ahead).

Also bear in mind most mutual funds, not necessarily hedge funds, have 'fiscal years' (implications were explored in detail). What this means is an increasing absence of contributory funding flows.

This contributed to desperate holding and rebound efforts; as augmented by volatility associated with final days for liquidations as relate to the end of Q3 (regular way selling some hedge funds desired if they didn't want to show certain stocks on the books as of the new Quarter). Friday allowed purchases to settle within Q4; an offset. So a down Thursday and up Friday were projected and not surprising.

For now we retain our overall E-mini / Dec. S&P 2007 short-sale guideline (having segmented this for traders so they took huge 25-30 handle gains on the way down and were prepared for the ensuing rebound).

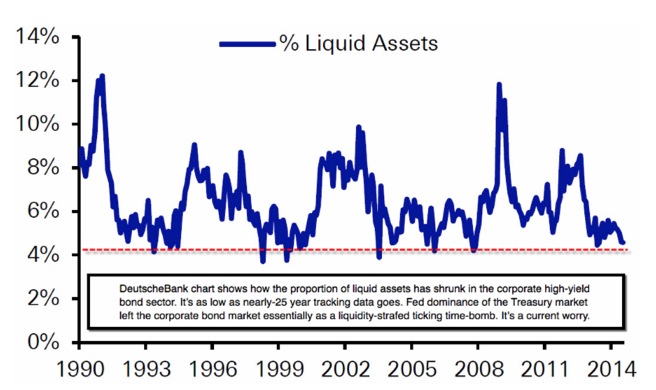

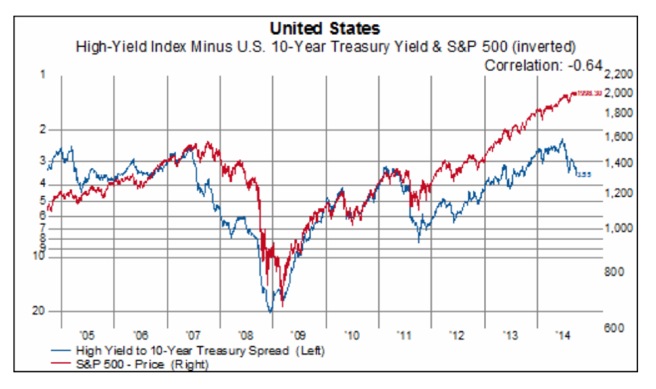

It contributed; but the real story was something warned of before: behavior of the High-Yield market, as continues plunging. Hedgers and a few others look at this closely (though rarely mentioned in mainstream press) as there are hedge funds heavily involved, which could be pushed into what is called a 'liquidation', just to offset obligations and damage from that area.

Wednesday I mentioned the vulnerability of the 'whole market' to slippage in Apple and Alibaba; as both had held-up tentatively at best in recent days and both came under subsequent pressure. (Specifics on these followed.)

The main technical point was attacks on the 50-day Moving Average; then a slight rebound; resumption of lower prices; and breaking the 100-day MA in advance of a rebound; etc. It's what we'd been on the lookout for all week; first outlining that pattern along with the short-sale in the E-mini / December S&P from 2007 last Friday morning. The idea: the last Sept. 'open interest' settlements (or margin calls) impact; a rebound; then a key technical battle.

Gene

Gene Inger

www.ingerletter.com