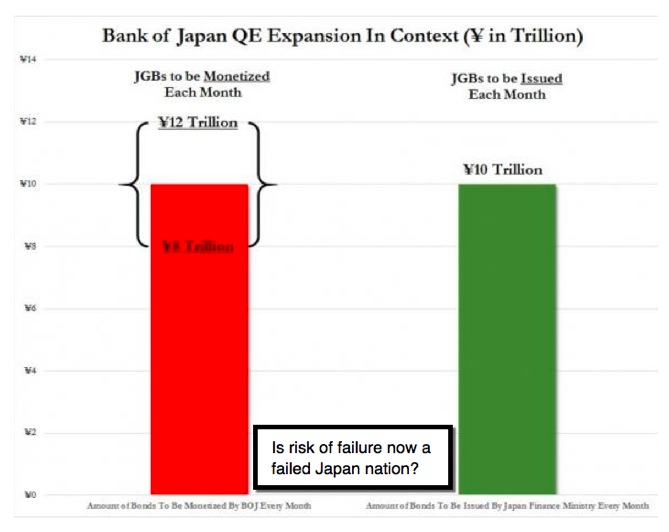

'Banzeinomics' - set-the-stage for Friday's rolling capitulation (a migrating blow-off) first in Tokyo; then Europe; and finally in America. It really got to such extreme assumptions' of 'first Japan, then Europe, then the USA'; that it was necessary for even the German Finance Minister to intercede, and say 'nein' to new EU QE excesses. Later even Goldman Sachs questioned it. But, to no great surprise; most pundits failed to recognize this is a symptom of desperate Japan; not beginning a rolling new equity-lifting QE spasm series.

My view was that this played-into the 'fiscal year-end' mania; perfectly. While I discussed this in video 2 this weekend, note that the Japanese effort being so 'celebrated', is really a response to 'terrible' economic news; and a desperate response. Because institutions pretend this benefits markets (regardless of impacts on society or debasing of currency); they chime-in; debt and the future be dammed basically. Technically this breaks-out to higher highs; with a degree of complacency that's intriguingly-interesting in overbought territory.

Bottom-line: the market moved on fiscal year-end 'massaging', which they will not describe as 'mark-up' rallies, since they really can't say that. But everyone knows fund pricing is based on fiscal-year-end levels; so manager's best interests are served by having Friday close at the best possible levels. This of course relates not only to 'peer' and 'Index' relational comparisons (useful for their marketing too); but in some cases relates to performance compensation. So our analysis felt this was a technically-expected thrust up; more for 'structural' market internal (fund pricing) than usual indicator shifts.

The above aspect is now done; now we have Mid-Term Elections coming up Tuesday. As of Saturday, looks like Colorado is giving a hint; over 100,000 more Republicans than Democrats having voted early or by mail, according to surveys. According to the AP, Republicans usually lead, but not by such 'hefty margins'. Markets will reasonably view (for ingerletter.com members only).

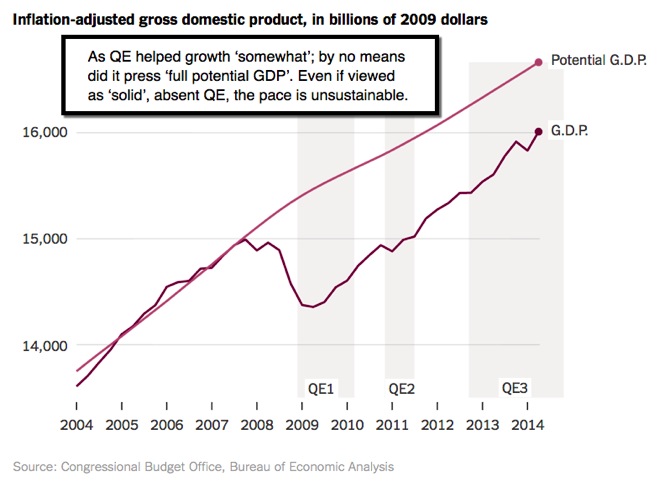

That's inferring attempts to get a better handle on spending; perhaps enabling the Federal Reserve to say 'their job is done', since the Congress can finally end gridlock and assume the fiscal legislative duties.

In-sum: market thrust on 'let's give another Hail Mary on panic monetization by Japan', tied-into fiscal-year-end typical firming; to extend a dangerously priced market even more. We expected this upside phase; suspect that with a market now (outlines what's likely after Elections). Stay tuned.

Finally, the proximity of the 'fiscal yearend' for many funds contributed both to prior liquidations, then recent buys and leverage increases as anticipated. Of course they were in races to enhance overall performance pictures; for many it relates to compensation; not merely S&P peer-matching, as prevails most of the year. That's part of why a unanimity of beliefs that markets get (future).

Enjoy the trading week ahead!

Gene

Gene Inger

www.ingerletter.com