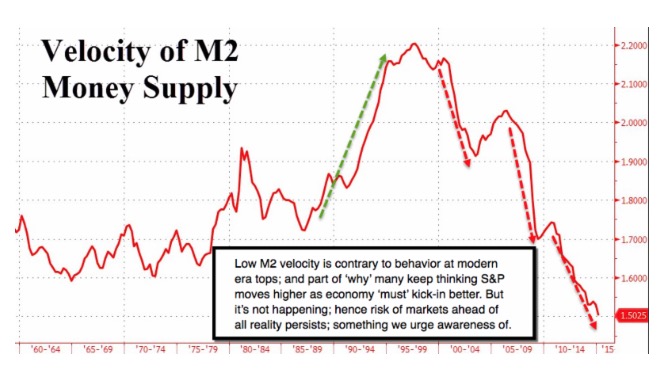

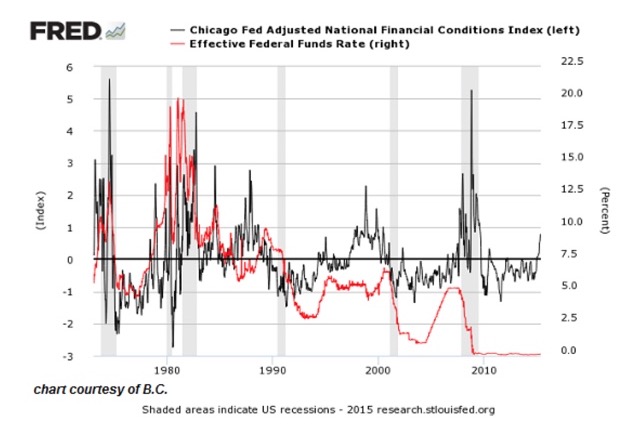

Reduced 'capital formation' - is about the last thing the Federal Reserve of course expected after their repeated rounds of stimulus; but is what they got. They often dismiss policy criticism based on 'it would have been worse if we'd not done the emergency stimulus', and we agree; but dispute benefits of any continuation beyond that point. A simple gander at the M2 'Velocity' of money proves the lack of dynamism after all their effort.

There's a seriously dangerous aspect here; aside a Fed painted into a corner (this important topic discussed with ingerletter.com members; by the way the Memorial Day rebate special expires at the Holiday's end).

Government is stuck today; an inability to fund what's needed; not simply too much money you can't get them to release. The incredible facilitation of asset price rises pleases investors of course; but at the expense of (areas holding back America versus most industrialized countries; we do mention Amtrak in this discussion; as while many talk about subsidies, they conveniently omit a fact: 70% of all New York / Washington traffic is Amtrak, and that includes the air shuttles; hence Amtrak Northeast Corridor IS profitable and lags behind all modern systems -including high-speed rail- hence funding isn't subsidizing in this case; though most nations DO subsidize efficient transport systems).

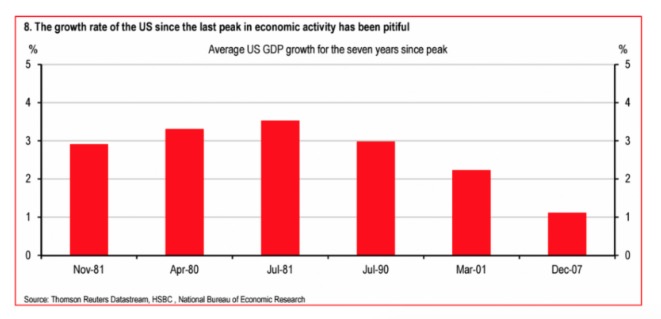

My point is Washington has been borrowing from Peter to pay Paul as we all at this point know. And they won't get out of it by more stimulus. That means, if we're right, that growing our way to levels justifying current S&P multiples is a tall task; and one that leaves that 'open jaw' (per our chart the other day).

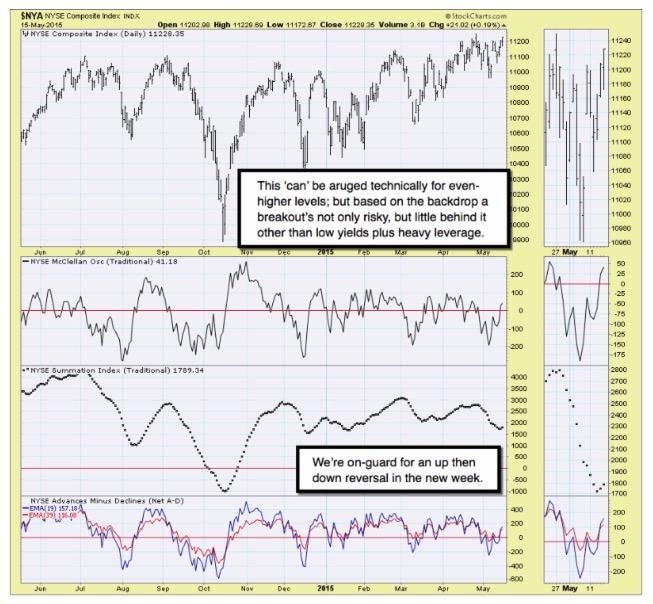

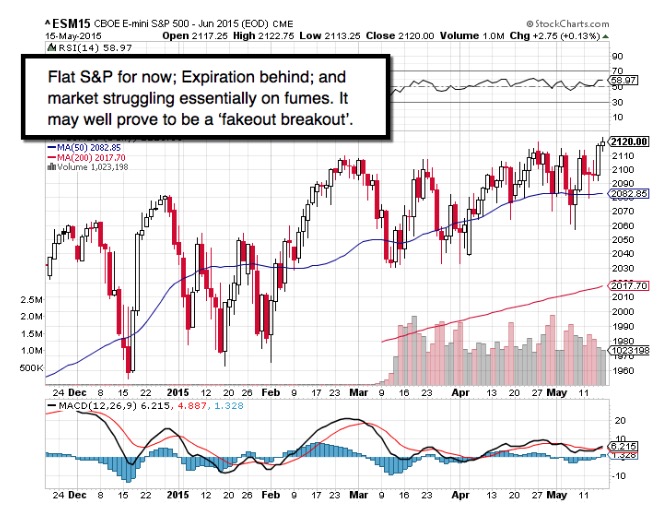

Yes a cursory glance at indicators shows the recovery and new high assault in advance of and during the nominal Expiration; and yes we haven't had the typical sell in May and go away kind of decline. But on the other hand, that old saw means look for (forward progression discussed with our members).

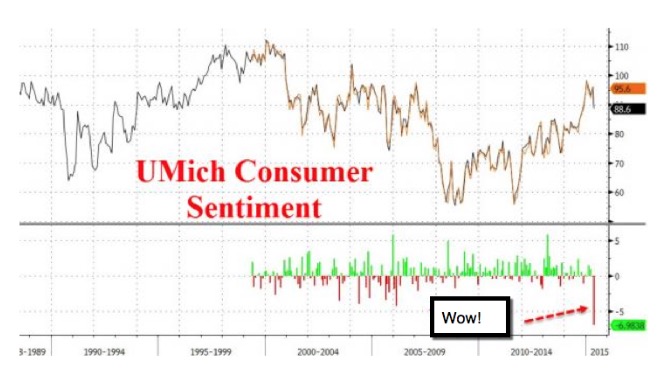

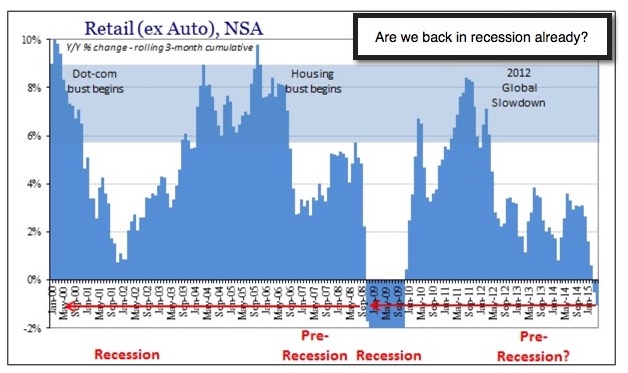

But let me leave this weekend reflection with an M2 comment again; as unlike previous recoveries following recessionary declines, central banks didn't build up any urgency to borrow or spend (by business or consumers) by raising any interest rates during the so-called recovery. That lack of 'velocity' suggests we are still in (or going back into) a sort of recession rather than the huge buying binge the bulls keep counting on. They have no basis in their forecasts, but of course persist in arguing it (balance of topic redacted).

Bottom-line: whether or not this market tops literally in (timing prospects); it's overwrought, pained to advance, and subject to (redacted), whether Europe (where Bulls are counting on a Greek settlement to buy time); the Middle East (as Bulls and Bears praise the US Army Delta Force for eliminating one of the key barbarians in ISIS), as reprisals and fights go on especially around cities like Ramadi and nearby refineries (and perhaps soon an Egyptian incursion into Libya to clean up the Islamists there); and of course a lack of confidence about earnings and sales from many businesses, all of which generally tends to be ignored by the market strategists. We aren't ignoring it; (what we do).

Daily action - my point above about banks, was that they looked at profits far too much than their traditional function within the private sector economy. By contributing to elevating stock prices they set-up the ability for companies to position buy-backs, using bond issuance in many cases; but drained capital I contended, that otherwise might have been channeled into the private sector.

Now with a market disaster (redacted important topic about 'credit lines' being established by ETF's); and thus the implications in-event of a 'flash crash'.

In sum: central bank care must be taken, and preventative actions so far are inadequate to change the risk profile. (Policymaker topic next for members.)

Prior highlights follow:

Trillions of Dollars are sloshing around - which buttresses a complacency that allows many to expect as many tsunamis of hot money that it takes, just to keep financial markets extended. It never worked that way before; even as the advocates of real estate or stocks 'never' coming down tried to argue that.

For this market not to at-minimum correct; at maximum considerably more; is (a low odds prospect that isn't our expectation, but we'll outline regardless).

The key to this approach is other economic indicators and trends allow a slew of analysts to proclaim no bubble so this trend can continue exponentially. Hardly I counter: (reasons redacted).

Government has remained profligate; and encourages consumers (they don't call us citizens) to spend more, and save less. Irresponsible sure; but easy to understand the motivation. (Reserved for regular members.)

Bottom-line: despite the S&P actually achieving new highs; the market's internal top has been behind for weeks; not a new development. Rebounds basically appear to be efforts to forestall the technical breakdown threatened many times of late; not affirmations of anything favorable.

Treacherous times. The process evolves. Join us THIS week if you'd like the rarely offered 'rebate', and in a particularly crucial time for the markets.

Enjoy your weekend!

Gene

Gene Inger

www.ingerletter.com