Holding short over 'a weekend of risk' - was not a huge gamble, given the sizable paper gain in our 'live' Sept. S&P / E-mini 2115 short-sale. While we retained the mental stop to lock-in at least 15 handles gain for traders, and of course warned investors to stay away from the market's long-side; we may not see that mental stop challenged at all immediately, based on Saturday news.

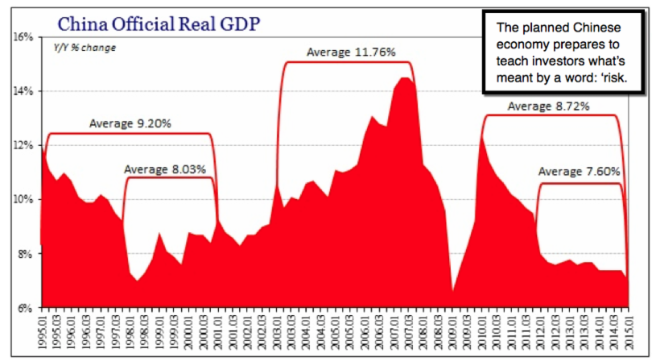

You may review the 'prior highlights' to see the set-up which had us unusually retain an intraday short for several days, not hours this past week; and why we based the retention in-part on possible Greek headline news; but also China. In the latter they just moved to lower 'reserve requirements' and more, trying hard to prevent a downside vacuum (also known as a 'crash', as already occurred to a degree). In the former; we thought the political split in Germany, as well as a recalcitrant constituency in Greece, made resolving this quickly, improbable.

So this Saturday, we'll just summarize what's happened, at least as of now, as we are positioned for the downside, should that unfold, as best imaginable:

a) 'Close Only' declaration in FX (Euro) markets (in Friday's final hour and into post-midnight hour Sunday in Europe, at least; "Due to uncertainty surrounding ongoing Greek debt negotiations, ahead of a potential announcement over the weekend that could lead to high volatility on the market, please be informed we have decided to decrease your risks by temporarily moving all Instruments to 'Close Only' mode (balance redacted);

b) 'assuming' no surprise deal, some currencies/fiats may rise dramatically as of if the Euro tanks dramatically (Dollar rally too). If so it means that the major currencies/fiats markets won't be closed, but an absence of bids might prevail;

c) the currency brokers apparently realize they take the other side of the trade; so 'close only' means they have to 'absorb' liquidations. Perhaps they're trying to minimize 'their' risk, as NO new positions or pending orders get executed;

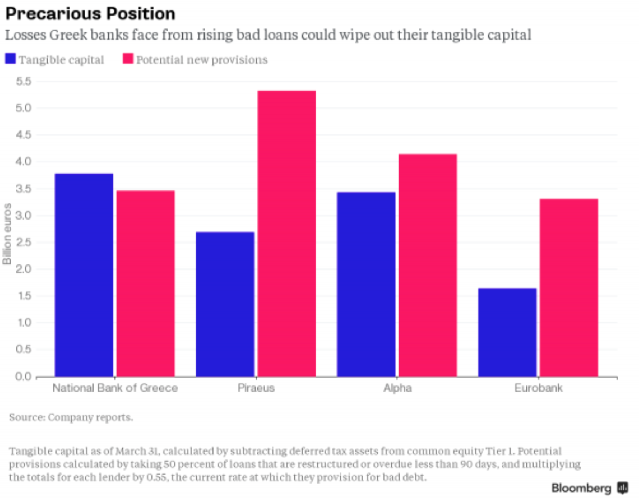

d) "possible Greek default on debt due to the International Monetary Fund next week would trigger cross-default clauses (balance redacted);

e) early this morning we heard Varoufakis quoted as saying he would ask the Eurogroup for a bailout extension of a few weeks to accommodate a Greek referendum. He purportedly accepts that if Eurogroup says no, then the entire Greek gambit, which has been a bet that to Europe the opportunity cost of a Grexit is higher than folding to Greek demands, collapses.

(Redacted.) Then, the only question is whether ECB will also end the ELA at midnight June 30, adding insult to injury, even risking the collapse of the Greek banking system ahead of a referendum whose purpose would now be moot;

f) the EU ministers REJECTED an extension after about an hour's deliberation, and are continuing talks without Greece present (Plan 'B'?);

g) the 'news conference' was cancelled; no more releases for now; per AFP;

h) appears (and that's no surprise) Athens expected this outcome, and while all efforts will be made by the ECB to stabilize the Euro, it may move further in the direction of 'parity to the Dollar', which I've said is out there for over a year (we have been stalwart Dollar bulls since the 79 area for over a year and a half).

Greece wants to be rid of existing austerity and they want freedom from debt; perhaps means a couple years of suffering (like Iceland), then a new Greece slowly emerges on a path to stability absent and apart from the Troika, ECB; and even 'capital markets' likely reopen to them, regardless of warnings from ECB, IMF and so on. We've speculated about this for some time.

i) this may NOT involve the worst-case fears of Greece entering Russia's orbit or leaving NATO, (redacted). It may be shaped in the form of (reserved).

and finally:

j) we'll have to see if Eurogroup makes it official (hasn't as of presstime) to the extent of Greece being excommunicated in a sense from the group.

In sum: here's the final statement as of now (redacted for these highlights):

Bottom-line: barring some unexpected reversal of Greece's (or even Germany's) stance before the S&P opens at 6 p.m. ET Sunday; you would presume a gap-down heavy decline.

Whether that continues (and then rebounds or something unpredictable, like closing of any FX or equity markets anywhere in Europe, much less a bank run which is probably too late in Greece), is going to determine the veracity of a decline or even a recovery. For now it's all leaning to the downside, but it's not over until it's over.

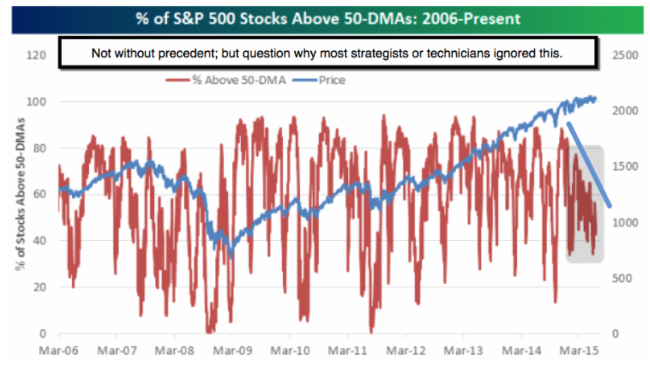

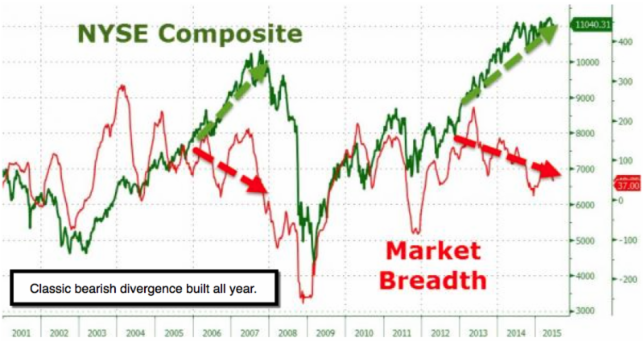

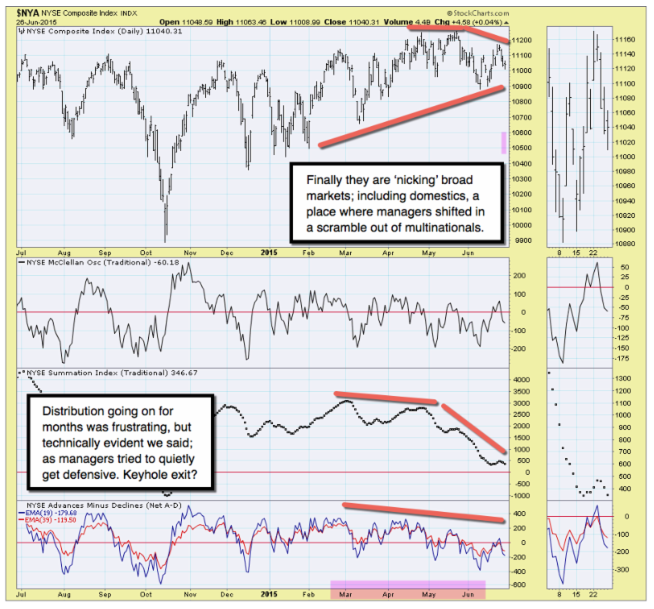

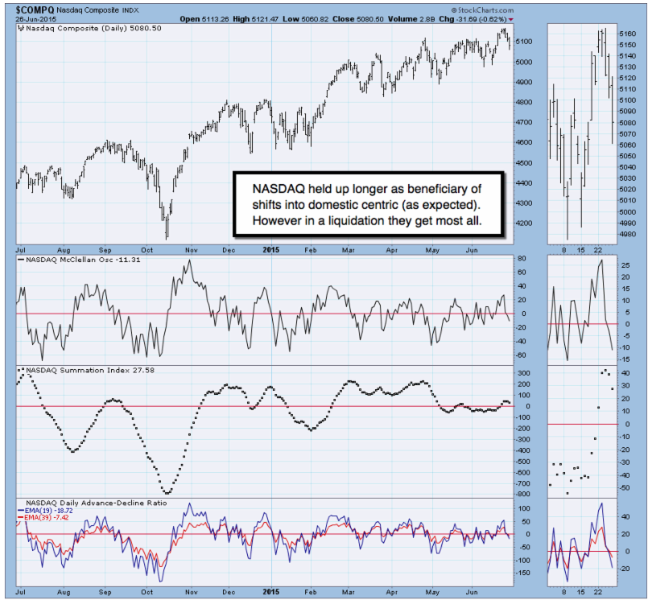

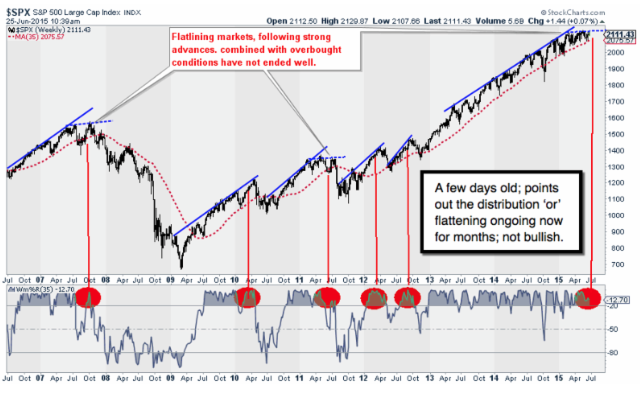

The market's technical distribution here in the USA has been evident for months now; and of course fatiguing, even as the vast majority of S&P trading efforts have been successful. We felt we'd not get through June without a swoon (ensuing rebound or not); then, irrespective of Grecian Formulas.

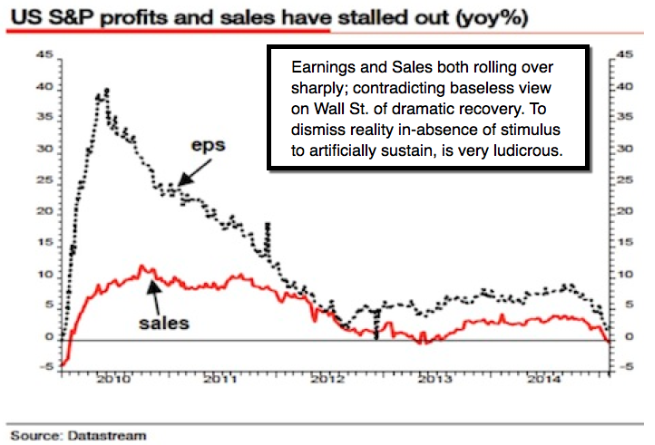

This is of course the primary reason for our various shorts; mostly on spikes allowing gains if well timed. The current one was deemed technically important too; not merely related to the Greek Crisis; but the overall global economic situation; China included. (Rest redacted.)

We're holding short Sept. S&P from 2115, and very pleased, though we won't say relieved at Europe's moves; because we don't wish hardships or disunity to anyone. But as I'm often mention, Europe is a 'confederacy' not truly administered like the United States, and that's a problem given economic differentiations and retaining financial power of each 'sovereign'.

Daily action - allows us to preliminary take a slight bow (we spent weeks upon weeks dealing with the trading range and implications) for winning many of the 'skirmishes' in the fight; while now apparently on the edge of declaring 'Victory of the 'Battle Royale' around S&P 2100 that has raged for some time.

We think many arguing for investors to 'hold steady' and constantly shift from Indexes into individual stocks, were 'marketing' not analyzing, and hence knew the reality of the situation, or at least the implicit risks. The bond managers that were intellectually candid about not only liquidating but in a couple cases even embracing 'physical cash' were revealing the real thinking that must go on in of course the biggest 'bubble market', that being bonds. High Yields? Hah.

We called over a year for more of Dollar overall strength.

The crisis apparently (if not we'll address it) has commenced in-earnest. We do feel sympathy for the Greek people; sort of lament a 'Marshall Plan' approach not being taken (though in a sense it was, since Eurogroup had to know poor prospects of repayment existed long ago). We understand Germany's stance; but ironically suspect temporary suffering.

We go into Monday short Sept. S&P as you know wonderfully from 2115; and I have tried to go through what's happened Saturday more than I usually would, as financial media in the US is not covering this crisis at all today.

Now I'll enjoy the weekend too, with an eye on developments and Sunday S&P (more for members; unfair to ask forecasts without joining). Thanks for fighting the 'Battle Royale' considering the overall narrow range the market allowed traders to work in; while our urging investors to just build and hold cash and not buy into pricey stocks or ETF's, was also the right thing to do.

Prior highlights follow:

The highly combustible stand-off - at Europe's version of the 'Gunfight at the OK Corral' (seems resolved while Eurogroup confers within itself).

The pro's and con's are hotly debated; but policy is retention with a deadline of 'before Monday's opening' (Sunday night US time). This subject, along with at least some background on the slight distancing between Merkel and Schauble, is covered in an overview provided in tonight's second video. (Most redacted.)

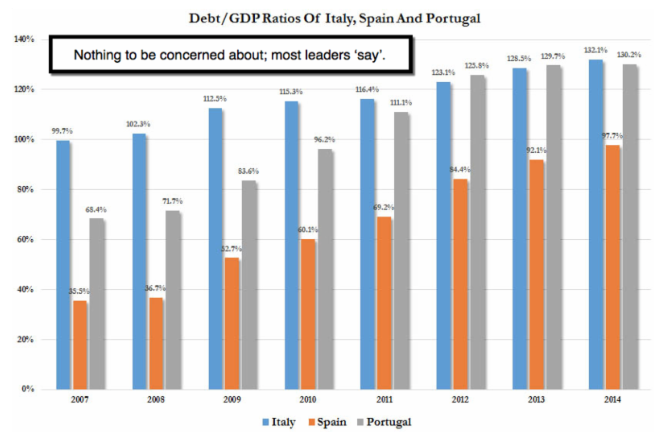

There are other tripwires out there. One we've mentioned (and shared charts of comparative risk) is China. Today I chatted a bit with a friend who is right in the midst of Shanghai (fabulous city he rightly calls it), and a money manager in California well connected to interests from there. There were distinctions.

Over there, and perhaps there's a lesson in this for 'elitists' here too, is what's afoot when volatility arrives that erodes an increasing charade of 'entitlement'. It's reminiscent of an old folk song refrain that goes something like: 'when it all comes down, hope it doesn't land on you'.

In sum: that will be the case.

Retained: the new Sept. S&P/E-mini 2115 short.

Many believe that this goes down with a whimper rather than a bang; or that it may even bolster the Euro if Greece leaves. Perhaps that's too simplistic, as a number of 'banks' are involved in this; so as usual in this modern world riddled with intertwining financial relationships, (redacted 'magnitude' discussion).

Bottom-line: the internal top's been behind for weeks; not a new technical development. Rallies evolved as efforts to forestall technical breakdown, as threatened many times; never affirming upside prospects. Now you can fight more, or cave-in, technically affirming a bearish picture 'after' the keyhole exit has closed, just as we forewarned.

Treacherous times. The process evolves.

Enjoy the weekend!

Gene

Gene Inger

www.ingerletter.com