'Gunfight at the o.k. corral' - might adequately describe ongoing snipes from all sides in Europe; except what you have had is more like 'Maginot Lines' that waver almost daily; but leave results of the battle 'somewhat' still in doubt. (At the same time the 'Battle Royale' around Sept. S&P 2100 is alive and well; as we even successfully traded the long-side before the 'live' E-mini 2118 short.)

Of course Greece remains the 'headline risk' going into the new week; and this report need not review what members already know; and the 'emergency' calls being set-up by EU leaders to deal with 'actual' responses dependent on final decisions seemingly forthcoming as this comes-up against a deadline, with the compromise proposal by Athens being readied for the 'high noon' shoot-out.

The general 'calming' approach in the financial press centers around avoiding panic, and giving assurances as to abilities the European Court authorized, to deflect concerns about peripheral EU members following any Grecian default or exit. We also suspect the meet with Russia was Athen's effort to impress on EU leaders that there are alternatives, 'if' arrangements fail to be made.

Many believe that this goes down with a whimper rather than a bang; or that it may even bolster the Euro if Greece leaves. Perhaps that's too simplistic, as a number of 'banks' are involved in this; so as usual in this modern world riddled with intertwining financial relationships, one shouldn't dismiss the magnitude an actual default or withdrawal would have.

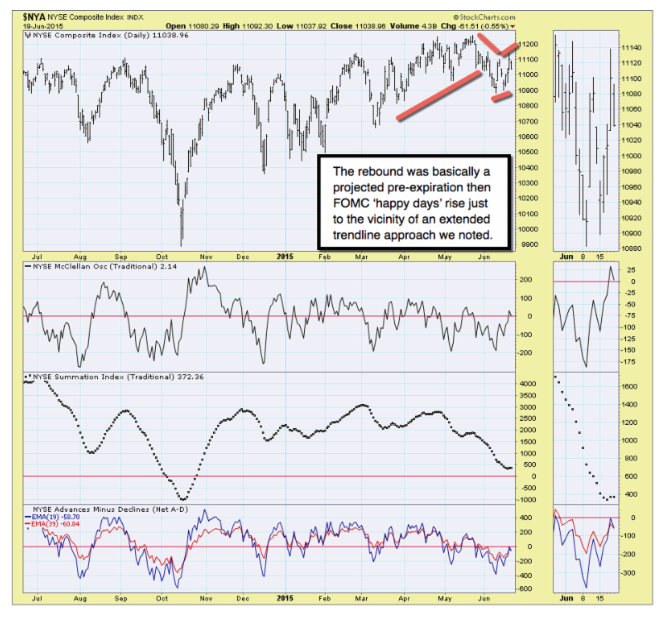

The way the S&P finished Friday for sure says some are not so calm. That was lots more than the late fade all week expected for Friday's Expiration finale ahead of a nervous weekend; and of course we're pleased to have fully retained Thursday's Sept. S&P 2118 short guideline throughout Friday and with the lowered mental stop for Monday; just to ensure totally solid downside gains, regardless.

In sum: is Greece on the verge of leaving the Euro (we opine on prospects). Believe Eurozone capital markets will deliver initially muted responses?

On Saturday afternoon, as I prepare this report; JP Morgan issuing a statement (nicely after markets closed of course) summarized this way from in context:

"If no agreement is reached on Monday, then the ECB will have little reason to show further flexibility and it will likely freeze its ELA limit on Greek banks. As a result capital controls will become almost inevitable after Monday."

Sure; and we had essentially the same story and conclusion Thursday; part of why we stuck with our short-sale. As is almost always the case, should things 'really' get out-of-hand, the distribution will have preceded the breakdown, and those selling into weakness will find they are after the keyhole exit closed.

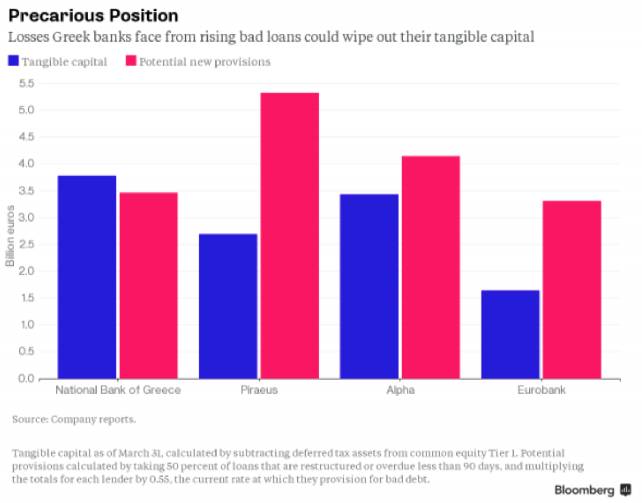

Bottom line: traders are perfectly positioned in-event of a plunge; and if not; a good gain anyway. Investors should (specific) be prepared that regardless how Greece goes, or interest rates, something may come along (issues noted). As a couple credit managers are sometimes advocating Cash; it denotes banking or financial structure concern (overextended or intertwined banks noted).

That's why in the UK you even hear calls to hold 'physical cash' and nothing in custodial names essentially; as account coverages are lower, and Government already said they wouldn't bail-out UK banks if a systemic event occurred. U.S. banks are safer in theory; but foreign intertwined exposure is great; hence not oblivious to risks globally.

Daily action - all week believed the rally above a declining tops was possible, but would be a reaction to the Fed (sure was; and rediculously so); and run-in shorts before a late pre-weekend fade, amidst an absence of bids basically.

Without at least an understanding among the political chiefs, Greek banks will reach the limits of their available collateral for more ECB aid. So common logic suggests they'll bite multiple bullets, and try to sort out this mess, via the EU's version of a 'Financial Gunfight at the O.K. Corral' coming right up. If not, then Katie bar the door; which is sort of what Friday's late S&P fade implies. We'd suggested nobody would want to buy (absence of bids) late Friday; sure was.

(Charts redacted.) For now we retain the relatively irrelevant position-posture short (inflection is all it represents; a great live guideline at the time) from June S&P 2131; about 2122 or so if you roughly adjust it to the Sept. contract now.

The great part is that our 'current' (from Thursday) Sept. E-mini / June S&P 'live' short-sale guideline at 2118 is pretty darn close; and is retained this weekend. We're using a (redacted) mental stop for the first half hour Monday; should any deal (if any is that quickly) codified prior to New York's opening; as the issues to sort-out are so complex.

Prior highlights follow (vast majority redacted; a courtesy report intends to convey a sample nature of our work; not forward strategy. Join us during this unprecedented market and potential upheavals beyond just Greece):

Blissful times, or rose-colored glass optimism - are alternatives debated. We've explored all that's known (that's pertinent), as Grecian headlines shift by the hour now; and a domestic market probably benefits from (people wonder where the liquidity has come from and then vanishes; we delve into that a bit).

Pretty much markets and Europe are either at a 'dead-end' or 'decision-point' and that's reflected by the ECB admitting (redacted) pressing a tipping point.

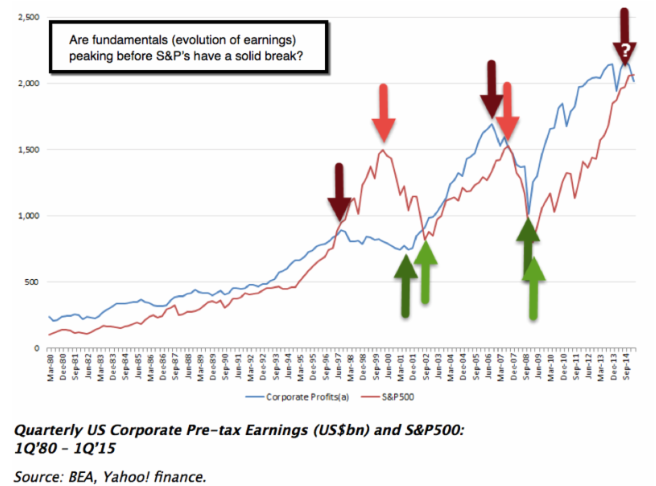

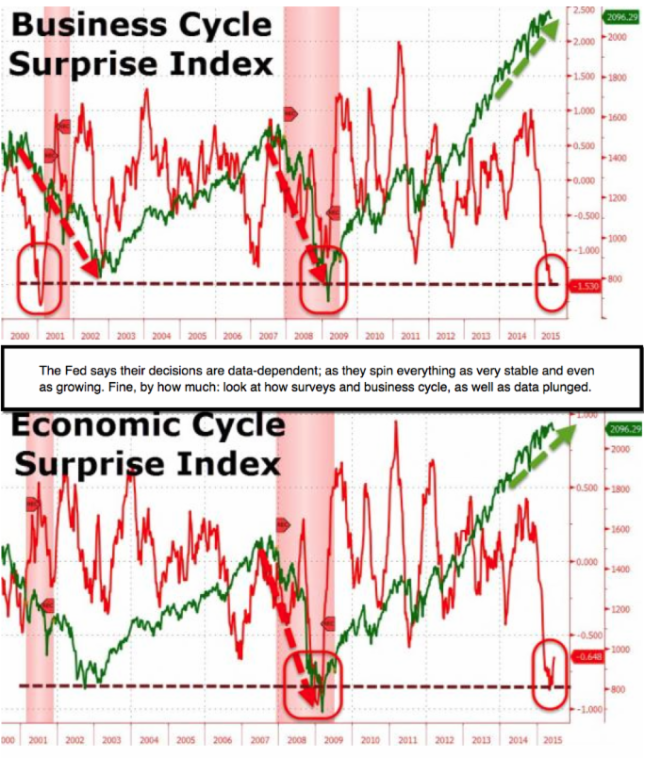

Massive overvaluations - in both equity and credit markets are front-burner concerns; minimized as best the Fed, and most reporters at the Conference, are able to skirt the real issues. Nobody risks questions about 'derivatives' risk (or perhaps like 2007 it's a time when 'some things just aren't discussed').

It's clear from Yellen's view of economic projections that conditions (redacted).

In sum: this was not 'really' a news conference; it was canned as obviously she looked down after every question (at talking points presumably) and was quick in response. I doubt there was a single question not known in-advance.

Bottom-line: past Quarterly Expiration; VIX Expiration; and the FOMC meeting. So, with all that behind, one looks next week to (redacted). But, given Greece and China (many overlooked that!); traders need to stay nimble.

Bottom-line: the internal top's been behind for weeks; not a new technical development. Rallies evolved as efforts to forestall technical breakdown, as threatened many times in recent weeks; and didn't affirm upside prospects.

Treacherous times. The process evolves.

Enjoy the weekend!

Gene

Gene Inger

www.ingerletter.com