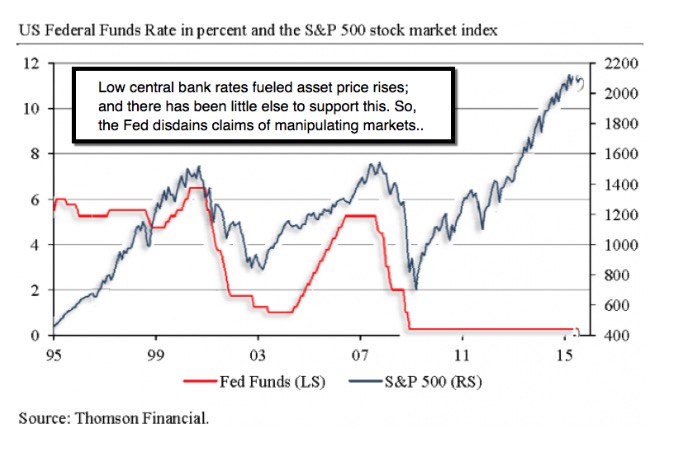

Overloaded 'capital market' - debt, remains the 'secret sauce' of this decline, that is masked by excessive talk about Fed policy or even short-term trading. If you look at record high Credit Default Swaps of some huge commodity firms (a Glencore comes to mind); you can see the risk of heavy sensitivity not only to the commodity slide; but (like oil too), denotes the 'structure' by which most all are financed. (Discussion of industries impacted as examples; reserved for our subscribing members. Now home in the USA; I warned of this in recent weeks from Europe, and yes had great experiences especially in France, even while taking time to issue our reports from Paris, Bordeaux, Biarritz and Amsterdam .. with the toughest being during the Med cruise from Spain to Italy; but did get a decent cellular signal in most ports, enabling my reports; even videos.)

(Nearly everything going on has media -even St. Louis Fed- acknowledging the trigger factors, ranging from China to the Fed QE / Keynesian policy error, as we have forewarned held great risks absent the Fed propping the market; so it would have to catch-down with reality; the heart of our argument during what we called an 'historic distribution' through most of 2015.)

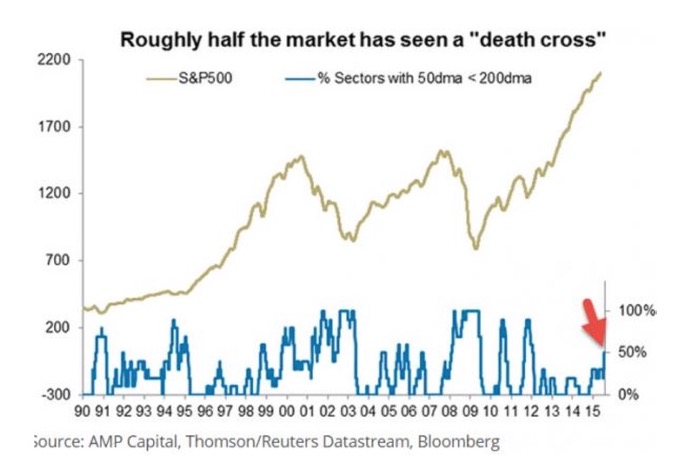

Everything is set-up for a disaster, for reasons not attributable to common risks noted; although those matter too of course. That doesn't mean disaster occurs in the full definition of that; but it does mean a large number of stocks entered bear market territory; and more are following. Most Oil stocks (some were just recommended by a major bank/broker) are cratering anew; and they should if you noted my comment about PE's. Now high PE's will be seen at highs and at lows too (low earnings so high PE even when down); so that's not a preferred approach to analysis. Even when we got our projected 100 / bbl price, I noted it was solely geopolitical concerns; there was 'no demand' to justify the price. We just think oil stock bulls are early, ultimately right; but that's a good bit off.

Speaking of timing; the pundits are scared. You know why? The most vocal get on television today to extol the benefits of buying if you have patience. That's a cop-out when coming from a present or former trader, because the focus really should know this is among the more difficult times for the market to rally, even in a time of 'actual' growth, rather than the 'stagflation' that dominates now.

The 'debt' issue, combined with far lower revenue and earnings forthcoming vs already-lowered guidance (for many not all firms), means the longer timeframe of the range we're finally breaking down from (it is the 3rd time is a charm 200 Day Moving Average hit; not the 4th time), gives more bearish evidence that supports a more sizable decline.

In tonight's main video we'll discuss momentum; not just our warning of thinner breadth (also a warning) on all recent rebounds on light volume. (To those not regular members we invited you to join believing this was already an accident happening; with more volatility ahead. Not to mention intention to recognize value for investors, once that is reestablished. So join us now; most big funds are still overloaded with some serious concerns still ahead.)

Daily action - first thanks the market for rallying to welcome me back from my travels at the week's start; and then for faltering significantly as expected after.

Technically the market (delayed reaction) followed China and commodities; Oil and more, down; breaking the 200-Day Moving Average nominally; having the requisite rebound attempt; and then flailing with a desperate post-FOMC rally; followed by a two-stage semi-capitulation in the final two hours of the day.

To our stance, expecting failing rallies in-context of an ongoing decline; there's no reason to take further action to certainly no reason to be buying stocks just because some pundit questions 'why' anyone has anything to fear. There is a lot to fear; beyond the technical pattern; (balance redacted).

In recent weeks, while the market mostly-eroded during my travels, we pointed out that the volume dried-up on rallies, but expanded on declines. That, plus a generally poor breadth-profile on the rebounds, was bearish technically and in that it affirmed our continuing view of money managers selling the rallies.

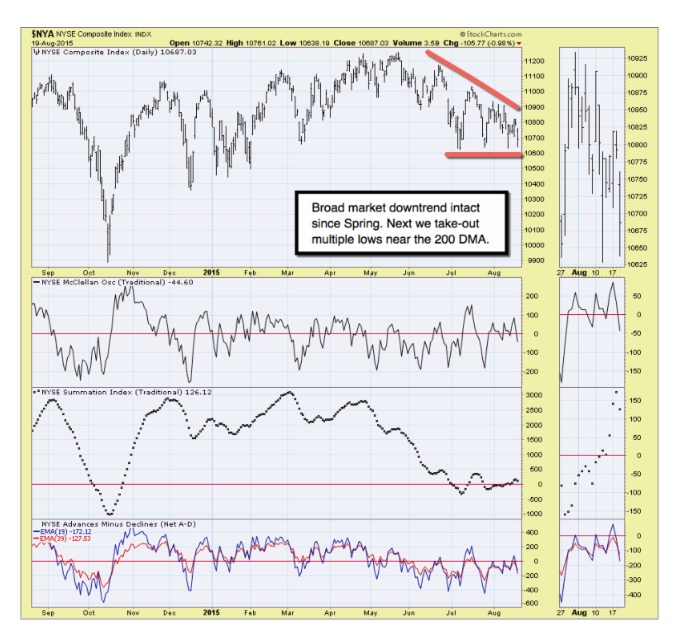

So now; Thursday we probably move below the 200-day Moving Average, as part of a 'downward continuation pattern' that I've outlined for weeks. Bulls efforts to again surmount the Sept. S&P 2100 area last week, and this week, were hollow, light volume rebounds; hence destined for abysmal failure.

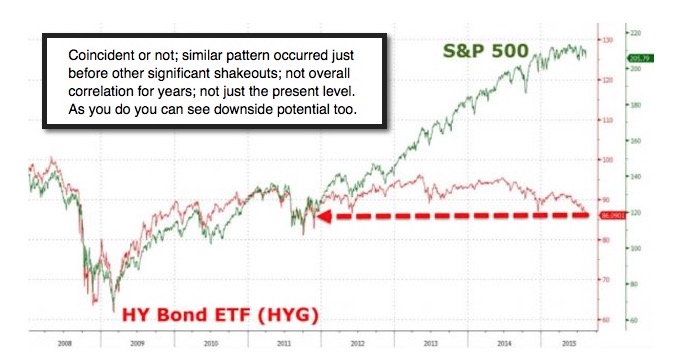

The 'Battle of 2100' was won as proclaimed weeks ago. Recent 'attacks' on the 2100 'financial Maginot Line' of sorts from below the zone, were destined to fail. The underlying commodity and serious debt issues are rarely cited; but are a reason true professionals know there is exponentially-increased default risk besides finance structuring issues I noted. As these prices cascade lower even more industries are thrown off their game (balance for members only).

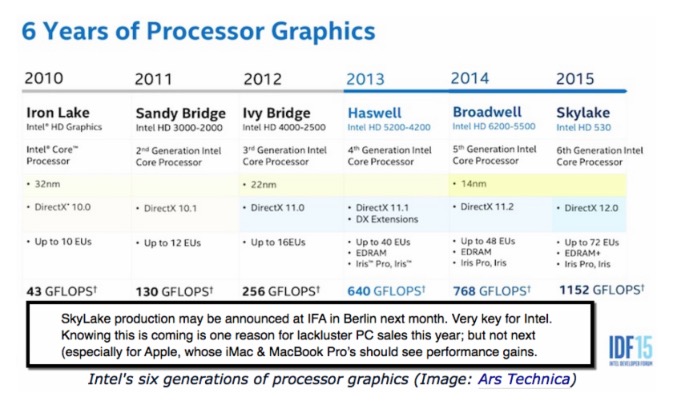

AND, my thought about China's hoarding being a non-recurrent event; hence the prices unlikely to recover in-general to the preceding levels, is another risk element, as again, the world might be set up for a given commodity fluctuating between (we'll redact the rest of this topic; but share a technical glimpse of the future, but for Intel and truly faster higher capability co-components.)

Primary trend is a breakdown from a trading range and ongoing broad decline.

Prior highlights follow:

Market instability - actually is a characteristic even in a firm turnaround like Monday's. Everyone of these 'save the trend' rebounds has had a relatively mediocre breadth spectrum, and usually on lighter volume than preceding dips too. This gets dismissed by some, citing August's holiday season, especially in Europe, but gyrations are beyond typical 'dog-day in August' muted action. Of course they are wrong; as there is great risk of another break any time now.

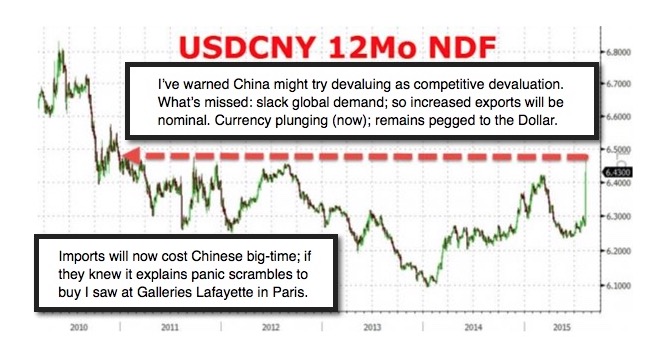

Chinese devaluation; the plunge in Oil (but not so much Oil stocks, which are thus at a higher PE multiple now incidentally); the focus on nominal sentiment improvements (but not actual data); and the effort to ignore global threats of a variety of manners, typify the effort to 'manage continued complacency'.

With Expiration and the FOMC Minutes ahead; as well as the market ignoring the high rates of inventories and currency ranges easing a bit; you've got scant or limited underpinnings for the advance just seen. Red alert basically.

Interest rates are almost beyond worthy discussion at this point. (The liquidity issues are the topic that is redacted in this portion of last Monday's report.)

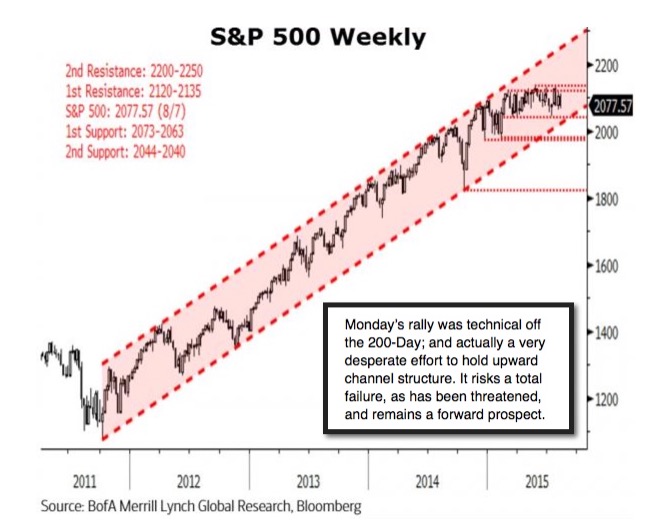

Abysmal recession logic - coming from comments suggesting Goldman has contended Yellen will shoot for a December rather than September rate hike; at the margin is the primary excuse for the ridiculous Monday upside thrust. It was primarily technical as they needed to bounce off the trend breakdown or 200-Day area; and that has less to do with China or the Fed; but portfolio guys genuinely fearful of letting the market have a much-overdue full-blown drop.

The economy is not behaving significantly different of-late. We have QE still in force in Europe and Japan; and we should be afraid of a pending bond bubble. The price/earnings ratio is very unstable and certainly not a a normal level as would be related to interest rates (much less earnings & revenue prospects).

(In sum): out-of-the-box rallies, especially on affirmation the economy still is doing poorly, are to be suspect. The battle 'under' the 2100 S&P area tries to reestablish strength and deny a trend breakdown. We think it's just buying time so doesn't change the outcome; a capitulation. (Last weekend's report.)

Bottom-line: the internal top's been behind for months (check the NY Comp in the McClellan Oscillator chart); not a new technical revelation; as Indexes superficially recovered yet-again on poor breadth; they put in sharp rebounds (characteristic of bear trend rallies). Rallies? Just mediocre efforts to forestall technical breakdown; virtually a 'rinse & repeat'. More plunges are looming.

Increasingly levels of skepticism fight 'invested' managers who can't really be defensive; but doesn't diminish a reality of overall price levels way out-of-line with probable profits growth or monetary policy guidance.

Treacherous times. The process evolves.

Enjoy the evening;

Gene

Gene Inger

www.ingerletter.com