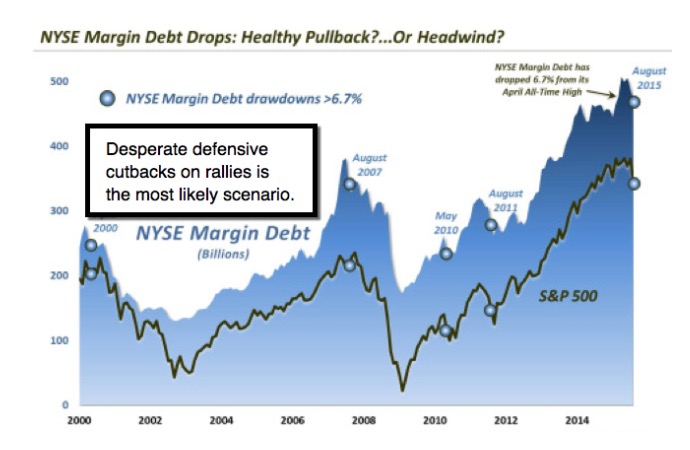

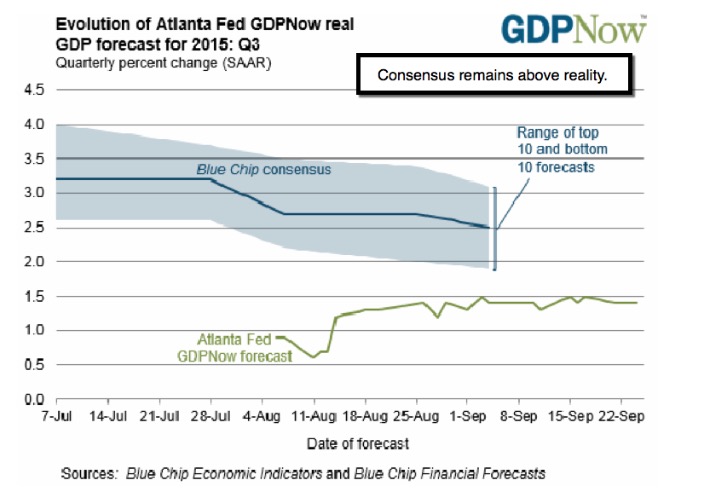

'Denial' is not a river in Egypt - as market price behavior has affirmed over at least a few months now. Despite months of distribution with lower volumes on most rallies, and higher on declines; despite leveraged buybacks masking the erosion of 'real' earnings, by virtue of reducing share floating-supplies; despite a deteriorating global economic picture, including downgrades by World Bank, IMF, and even such markers like the Atlanta Fed's GDP 'Now'; despite failure to accept lower commodities as a reflection of a post-China-hoarding era, plus a failure to recognize how financing structures of most projects globally are for the most part thrown into misalignment by the pricing level structure declines; despite all this... the majority of analysts 'still' call this a Bull Market. It's not.

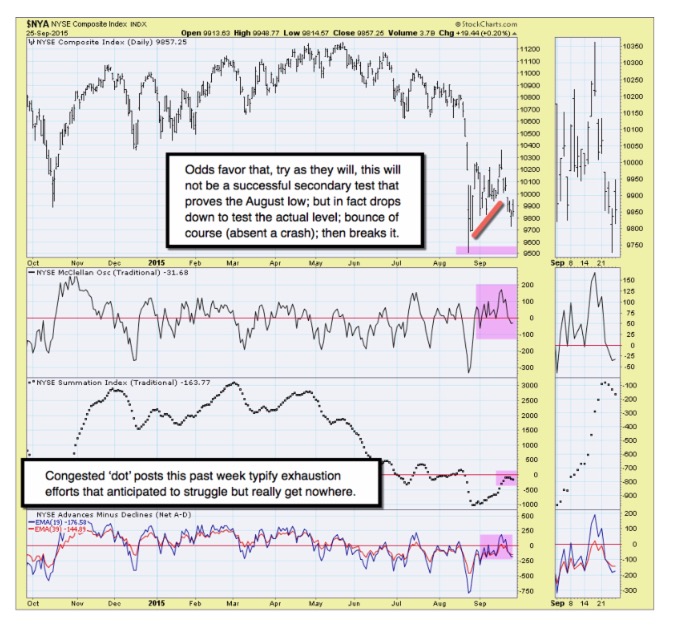

On top of it all (because this was one of history's lengthiest distributional tops that ended basically in the Spring, with a rebound into the Summer, concurrent with a 'Titanic deckchairs' rearranging from multinational into domestic stocks) you emerge with what I've expected: desperate bounces into early-mid July; a period of erosion peppered with feisty but unsustainable snap-backs; and then the August decline into what I projected as 'no-mans-land between the range that prevailed for months, and approaching the October of 2014 S&P lows.

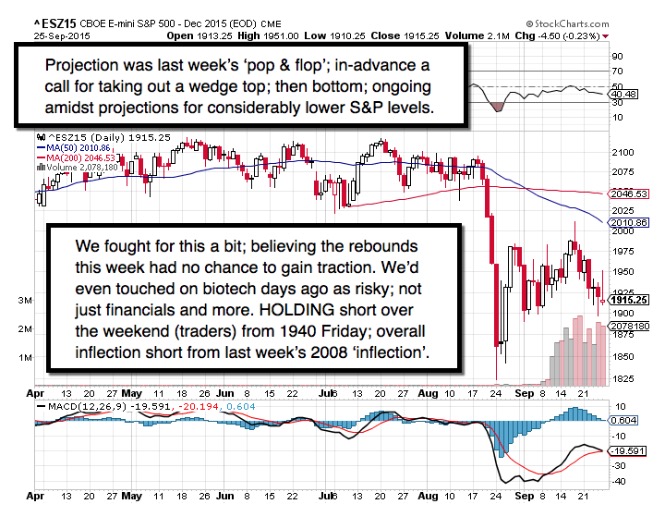

Just one more 'despite': despite all that and the relatively persistent rebounds over the weeks just past (which have been ending since the FOMC meeting; as represented by our Dec. S&P 2008 short-sale 'inflection' guideline that's not a daily guideline now (that's from Friday's at 1940 and continues into the Monday afternoon trade); reflecting overall expected 'pop & flop' transition or reversal points of the rebounds) ... with failing holding efforts (more redacted).

Daily action - began the week suspecting failing rally attempts followed by the weak finish to the week. Chair Yellen's speech on Thursday was sobering to a lot of folks, as she represented her remarks as 'her view' now, versus just the 'Committee's' last week. Translation: the idea of low-balling recovery by calling for a slow 'year or two' ahead, may be accurate, but didn't enthrall Wall Street.

For investors we continued advocating caution and not catching falling knives, in almost any sector. Remember many pundits focused on buying biotechs or financials, have had to backtrack as momentum stocks (waned per forecast).

If you add the credit, monetary, economic and earnings concerns; domestically or globally; you have potential vacuum (forward technical evolution redacted).

Combine an absence of bids with faltering rotation, and you have an issue that isn't suggesting any sort of sustainable low point envisioned for the S&P in the immediate future. Combine the Russell 2000 Small-Cap Index about to test its August low, and realize that is primarily 'domestic-centric' so many counted on to resist decline; and you can see the ingredients for a broader (reserved).

Besides the ongoing (just over one week) position-posture short-sale guideline that was a superb live intraday guideline at the time from Dec. S&P / E-mini at 2008 or so; for traders we retain the Friday intraday guideline 1940-42 short; at an incredible paper gain of around 25 handles or so based on Friday's close. It of course is each traders choice; we simply retained all into Monday (more).

Treacherous times. The process evolves. Likely akin to 'surfing' as it passes well past what's often called 'point break'. (Call for prior rebound rolling over.)

Enjoy the trading week!

Gene

Gene Inger

www.ingerletter.com