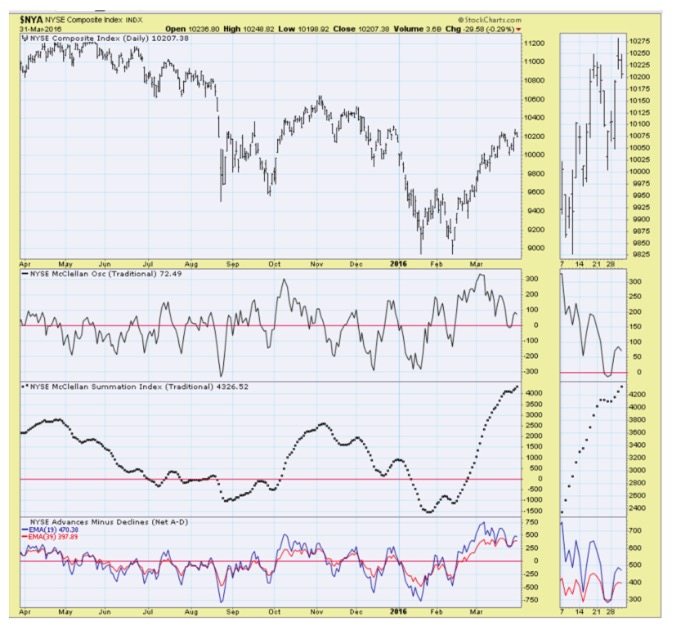

From a macro perspective - we're experiencing an S&P topping formation that may or may not turn 'south' rapidly; or persist in a distribution process. That after all, characterized the past year-and-a-half, and is again dangerously extended.

During this time we've had marvelous S&P trading moves outlined; biased to the downside (solely on spikes and not after the crowd capitulates after breaks) as it is appropriate in overbought surges (hugely profitable for the overall guidelines).

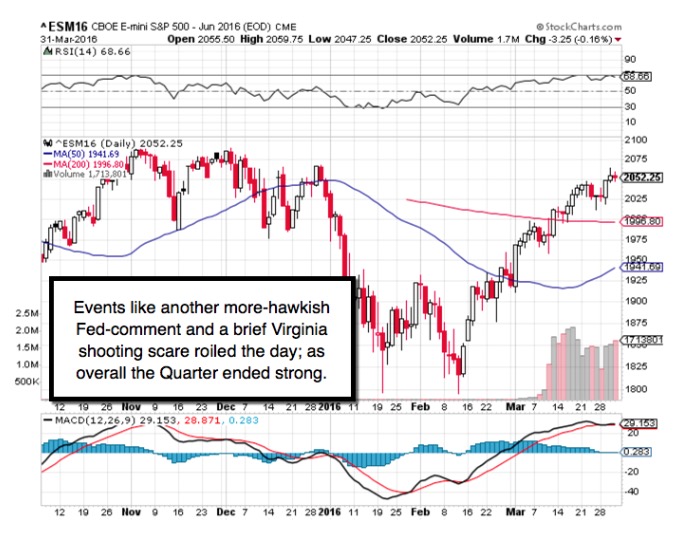

(Monetary policy discussions this week) made a point that the 'real' policy mode of the Federal Reserve began to squelch stimulus quite awhile back, initially via tapering, avoiding more QE, and then nervous firming of the 'Funds rate'; only to have trepidation's about further moves, just as heard over these past two weeks again (yesterday Fed heads made slightly less dovish, if not hawkish, comments and the markets briefly shook). Friday morning rebounds are suspicious (within technical ranges discussed with members regarding 'arc' vs. lateral resistance).

It's dangerous when a market has nothing of substance sustaining it other than dependence on Fed monetary support; and it's dangerous when the Fed tailors its remarks to transparently seem almost timed to buttress financial asset levels, which actually is not its mandate.

What does all this mean as we forge hellbent into Q1 earnings season? It likely means the meanderings of the late phase of this rebound cycle face rising risks; whether or not (a pattern continues evolving per projected ideal evolution).

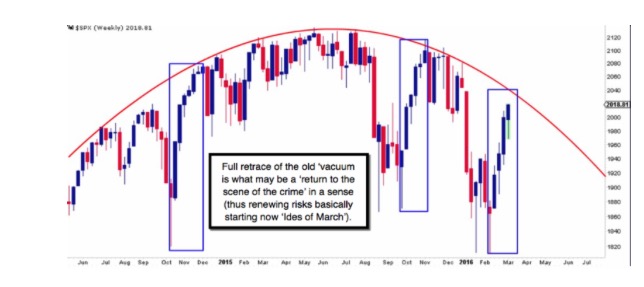

When one glances at the 'dome' we've shown at the end of these reports, or at tonight's more lateral resistance chart; what you see is a 'range' from here up to (in fairness to subscribing members, this discussed is mostly reserved).

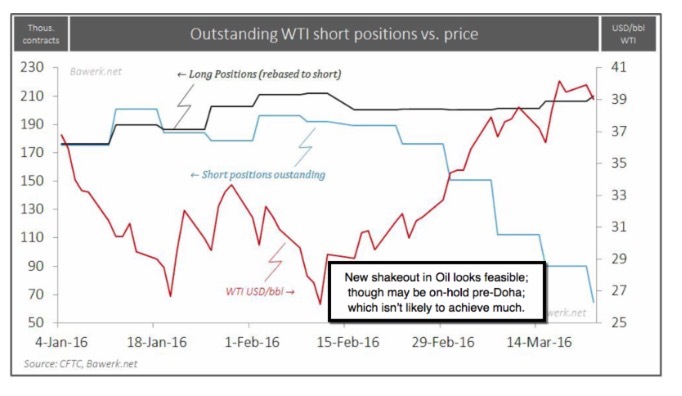

Bottom-line: the market has been gyrating in a high-level rebound range; with standard pitches about Fed influence and delusional recovery prospects heard for the most part. Buybacks are off-the-table as a support too; for companies in front of earnings; and the sensitivity to events has returned front-and-center as the new Quarter starts. The Oil gathering in Doha (redacted); though Oil stocks rebounding helped the rally, without improved earnings prospects (warning). (I have redacted the lateral flow of price and events chart for just subscribers.)

I mentioned the 'macro' picture as although we went through the worst January since 1933 (best for us; and hugely profitable); then the best month since 1933; that basically says the market eased back from overbought to oversold, only to get overbought again; setting-the-stage for (pending?).

That suggests, in a backdrop of risk and mediocre global growth, that if the next primary move of significance.

Also April is the month we've suspected the Middle East to heat up, with maybe a coordinated US / Russian move to liberate the next key city or even attack the ISIS stronghold of Raqqah. Meanwhile forces are gathering in Turkey and Iraq. (I'll include a map of new U.S. and Russian bases in the weekend report.)

Prior highlights follow (mostly redacted in fairness to members):

Perhaps more important than constant Fed chatter; may be a Paris Forum in which G20 central bankers are trying something different. Rather than the persistent (and counter-productive) stimulus efforts; they are going to contemplate how to retool the monetary plumbing to prepare for the next crisis. By even having the gathering, they're admitting it needs fixing!

A 'broadening top' of significance has been forming for some time; hence the relatively neutral action in the wake of push-up's after the Fed's dovish guidance was received in a favorable way (detailed to members).

Simply put: we forecast a couple choppy irresolute weeks mostly 'waiting' to get through event driven spots: FOMC, Expiration; Quarter's-end etc. In the midst of this; the attack on Europe's 'center of power'. Brussels, as the seat of ECB, EU and NATO, sends wider wake-up calls to member-states; though you'd think everyone was well-aware of Islamic extremist tentacles throughout Europe in an interlinked network, just as the French President noted a week earlier (and we emphasized).

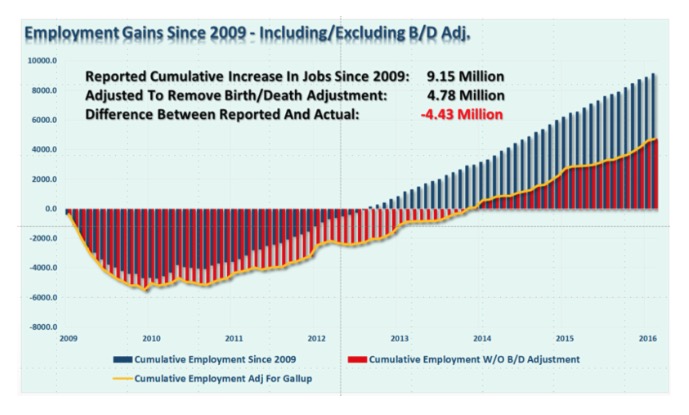

Battlegrounds are fluid - as multiple dynamics are going on in this world; with outcomes hard to ascertain. Not to mention gap vs. non-GAAP earnings show an incredible divergence. Aside monetary policy being neutralized (ran-in short sellers temporarily); U.S. stock prices will soon again focus on earnings or rates (or lack) of growth; and can set-up to take a hit in the near (April-May) future.

Enjoy the day and join us daily in coming volatility!

Gene

Gene Inger

www.ingerletter.com