Proximity to rate-hikes - reflected upon by a couple Fed Presidents, didn't halt the midday selling-reprieve, which suggests (no surprise) traders are trying very hard to deter an approach to the 'edge of a precipice', which is fairly obvious just by noting levels from which every recent bounce of significance has occurred. It is notable; as technically a longer-term broadening-top occurred last year; thus it may be frustrating; but all of these bounces have been faltering rebound tests.

Technically the market repeatedly bounced right from where it needed too (take a look at the S&P daily-basis chart or the video). Additionally we indeed got the expected late Thursday fade; a set-up for more downward action on Friday.

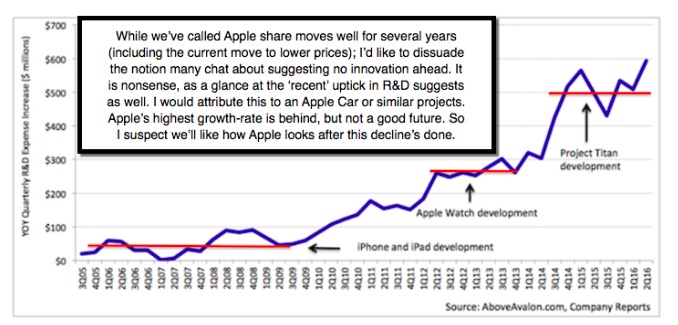

(Note we were bullish on Apple from around 70 in 2014; then shorted it around 125 a year ago; prior to covering and going long around 57; split-adjusted for all of course. More recently suggested a sale at 120; as well as the rebound falter around 107 last month, when I called for ideally a move to 80-85 or even lower.)

This evening charts and video tell the story; plus a few comments in the second video about Apple, which continues projected softening; and that is besides our expectation they will have a marvelous iPhone redesign; later in 2017 (their 10th Anniversary model incidentally, not the upcoming iPhone 7). Apple's price drop can impact the overall market because it's a bit of a market proxy these days.

After the Close Thursday, Nordstrom reported and 'missed'; which should not be a surprise to any who recognize the pressures the retail market has witnessed, and is not merely everyone traipsing-off to Amazon instead of brick and mortar. Of course that's part of it; but generally people are spending more on technology and a bit on entertainment, and less on clothing, or least high-priced clothing. (A higher overall retail number misleads; just cull-out the merchant segments.)

It's been quite a while since I mentioned the growing threat from style-conscious lower-end merchants, when first discovering stores like H&M and Forever21 and Zara in Europe (discussion on retail reserved for subscribing members).

Bottom-line: the market is working its way to lower levels. It's got no amazing tale to bolster monetary policy or oil markets or much else to prevent breaking of these high level S&P support levels, as the most-watched Index gradually works towards (how we know this is discussed with our subscribing members).

Incidentally the global picture is slightly deteriorating. The United States already had planned 'missile defense' for Europe, initially based in Romania. Well today the U.S. activated those systems, with a ribbon-cutting ceremony. I suspect the latter was intended to get Moscow's attention as they protested loudly and quite immediately uttered threats of how they could turn Bucharest to ashes. (More.)

It's a bit similar with China; who has harassed USN and Australian 'freedom of navigation' flights and warship passages in waters that are more Filipino than Chinese. That too is problem of China's own making by pushing territorial claims in Asia; not unlike Russia trying to press to reclaim former captive nations. Not that we expect any conflict (balance in the full daily report)

In-sum: we hold short June S&P from 2104; no changes.

Daily action - generally adhered to the down-up-down pattern suggested, even if the first hour was squirrelly. Then down; lrebound; dip; another bounce; then late fade (all as outlined to deliver the realized end-result).

The proximity of breakdown and the edge of that precipice is within proximate range, really at any time. NASDAQ and the NYSE are already there. S&P needs a bit of capitulation; (how imminent this is or isn't is outlined to members).

We had thought that we would see a downward consolidation and that's what it was. To wit; drop but not definitively quite yet; which is more negative than just consolidating, but not so negative that it breaks the key supports. That the S&P bounces repeatedly off that same general area is telling (projection follows).

The 200 day moving average is now trending down for S&P, many European or Asian markets, and South America is a disaster (poor Venezuela not just Brazil). Furthermore, yield curves in the US, Japan and Europe have flattened. Recent failed rallies were (trading conditions and forward expectations redacted).

Such characterizations are not bullish. We hold short from June S&P 2104. It would not surprise me if this Friday and next week (perform a certain 'dance').

Prior highlights follow: (generally redacted as details our overall analysis).

Rotational 'distribution' not 'accumulation' - has been how we've viewed the series of faltering recent rebounds, consistently contending that deterioration, as opposed to preparation for rallies, was the operative trading characteristic.

Battlegrounds are fluid - with multiple dynamics ongoing. Downside bias rose in the April-May time-frame; as did shorts, periodically run-in despite the validity of increasingly risky forward dynamics. We urge investors to remain wary; while traders stay nimble.

Battlegrounds are fluid - with multiple dynamics ongoing. Downside bias rose in the April-May time-frame; as did shorts, periodically run-in despite the validity of increasingly risky forward dynamics. We urge investors to remain wary; while traders stay nimble.

Enjoy the weekend,

Gene

Gene Inger

www.ingerletter.com