Stagnation and deflation - will never be affirmed by the Fed; though indirectly they've done that by lowering the Fund's forward target for 2017. Vulnerabilities in the global economy were addressed by Chair Yellen; and in our view are 'real' reasons they cowered in the face of concerns. (Our technical pattern analysis in the past two weeks accurately set-up the false rallies preparatory to decline.)

Ignoring China's devaluation (3rd recent time was last night and barely reported) and fears of competitive devaluations or other currency and credit market issues globally were part of their hesitation. The US Fed apparently fears blame for the brewing global challenges; although the outlook would be uncertain either way.

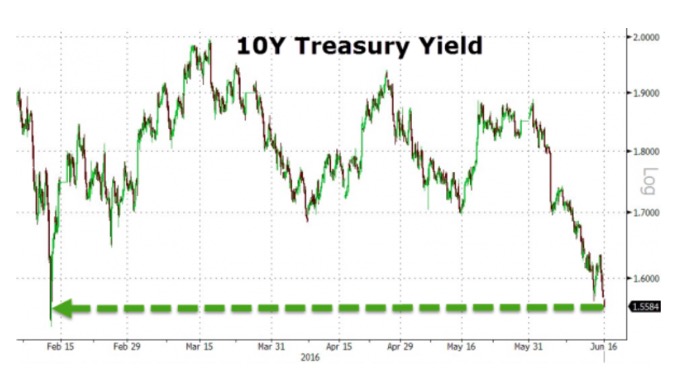

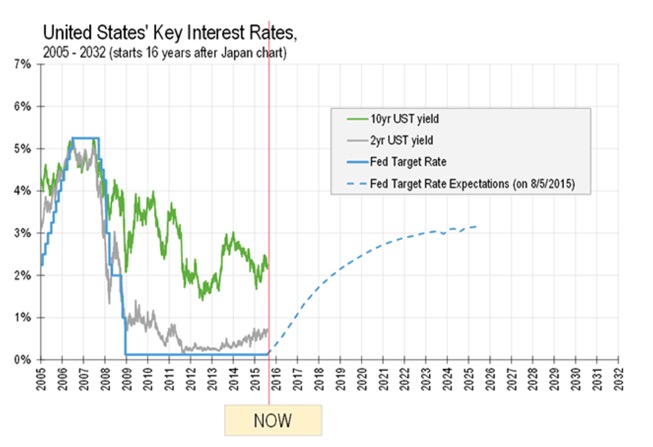

The error by the Fed is continuing to 'spin' their expectation to hike on what's of course called 'data dependency'. In fairness we doubt they have a mandate that directly allows them to say that they stay painted in a corner due to international influences or concerns, but it comes down to that. (Taylor Rule chart below.)

We thought they 'should' hike but wouldn't; and that remains the case. However we realized that Brexit did play into the factors holding them back; and the Chair said so. Consequences will nevertheless be felt and long-lasting. Whether Janet realizes it or not, she acknowledged it's an unusual situation; indirectly admitting the economic 'emergency' is essentially ongoing.

The comment that 'risk appetite, while unlikely, can change abruptly' was a key acknowledgement that the Fed might have to essentially play 'fast catch-up' via a series of rate hikes. Now she ignored the impact on credit and equity markets;

In-sum: the Fed took a giant step towards admitting what we've contended still is the 'reality' of the world these days. It acknowledged more than softening of a sort around the edges (the way they wanted it to be taken); but parsing it just a bit more; you get from this a belated admission of a 'global deflationary spiral'.

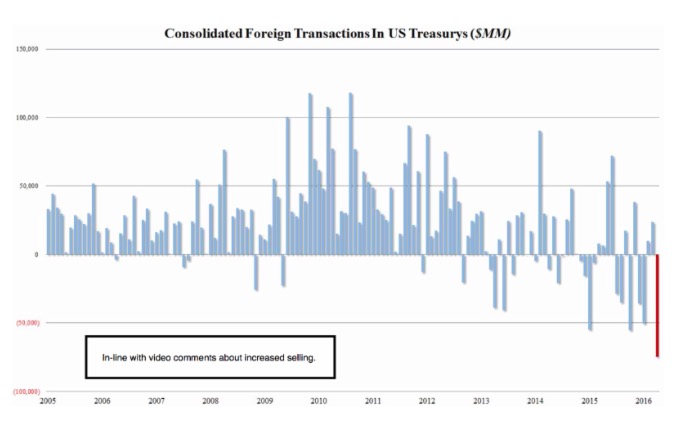

It's definitely a non-virtuous cycle; the opposite of how bulls interpreted dovish Fed policy they so desired. It also means a probable broader recognition that a lot of the financial asset gains (including real estate not just equity index levels) have come from first 'yield chasing' and then foreign money seeking 'any return' at all; as some return beats no return.

The two primary stances above means the stock market remains way-extended relative to forward expectations. (How dire is a redacted comment). Because most bears are more than 'net long' (many still heavily 'leveraged' net long) you have market vulnerability that's been simmering probably since the first signs of a new Recession, that in my view I've said will be traced roughly from last July.

All the efforts to recover in markets since then have been based on hope; on trying to eek-out gains based on rotation and foreign inflows seeking yield; not growth in earnings or meaningful revenue increases. And by the way the Fed discussed much more than their official mandate today; implying what we have contended all along; they're deciding based on (reviewed concerns).

Analysts and politicians in some cases similarly covered-up delays in economic recovery that a sensible application of funds might have assisted. Their 'spin' extended stock markets while the overall economy languished; preparatory to the market catching-down, with where reality has been for some time now, and which periodic shakeouts have been warning of for about a year, as we noted.

Conclusion: confidence in the upside (or revival) will frey over the near-term as the majority of previous bulish interpretations were artificial to a great degree.

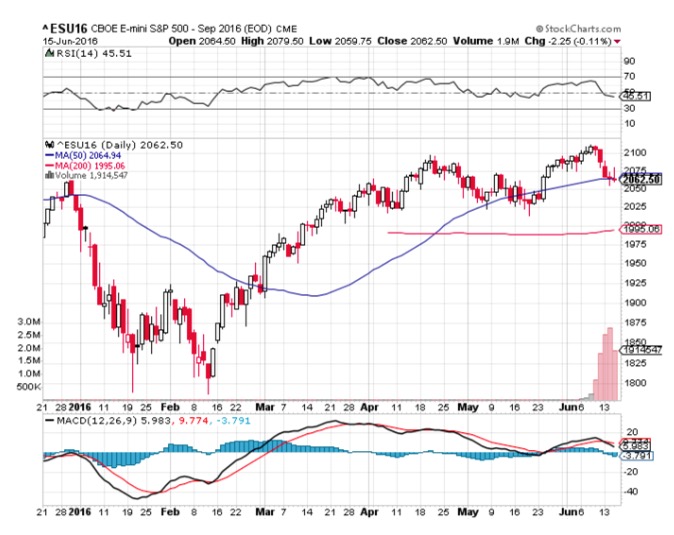

We continue the latest short-sale basis Sept. S&P from 2092. Now we have to contend with Quadruple Expiration; then Brexit. (Members now the impact we're suspecting will occur in markets and currencies.)

Daily action - is discussed in several videos above; so we'll abbreviate anything else here; with a clear view of lower prices regardless of interspersed rally tries.

We have our ongoing Sept. S&P short-sale guideline (live from last week's rally) at 2092; and it's ahead by a theoretical nearly 30 handles or so. Also I did note it might be low-risk to retain an intraday short-sale overnight made on a post-Fed second-effort spike; and certainly that's decent odds for early action Thursday.

Of course the interloper to all this could be the Quadruple Expiration; followed at the tail-end by both an S&P re-balancing and something similar for the Russell. So it's hard to say what little bubbles one might get accordingly. We're just very convinced (as we have been since last week) that this works lower with rallies at best interruptions within the context of a developing downtrend. (More follows.)

So presumably we'll have an even better (redacted) prospect for the S&P as this evolves; and if-and-as on-balance selling occurs in the credit markets, one won't be able to say that the Fed policy stance being dovish keeps sellers of our notes and paper away. This is troubling (more reflections).

If inclined review the day via the videos (last one has the intraday closes), and join us tomorrow in the Expiration. We hold short Sept. S&P from 2092.

Prior highlights follow: (generally reserved in fairness to members)

Incredible agility - is required to 'trade' a market facing what we'll call a flock of swans (black or otherwise), that gather like a 'swarm' that challenges markets. I am pleased, amid the chaotic backdrop (including coping with the massacre by an angry bisexual closet-case radical Islamic extremist who couldn't reconcile his sexuality with his warped fundamental Islam upbringing that teaches hate), with a trading approach focused on staying short overall this past week.

Technically one has to include so many concerns we've generally highlighted in these reports as developing.

Next week we have Brexit and more impact on FX (Foreign Exchange) markets as I've noted; although that concern is why European markets are defensive in almost all cases. Remember, in her wisdom, Prime Minister Margaret Thatcher pressed Great Britain to stay out of the Eurozone, which most believe was very necessary from a British perspective. It also means (Pound Sterling forecast.)

For the United States; the Dollar moves further (we've been bullish overall for a few years; but short-term again for some days more including fluctuating Oil or currency moves).

It could also in-part relate to fears that the Chinese market, given the enormous 'debt structure', could endanger global markets even more than other issues.

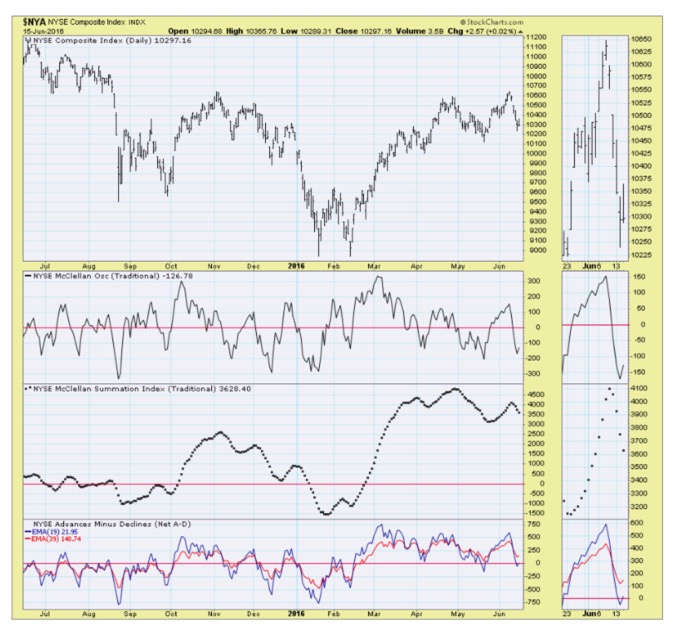

Overbought and extended; market began last week with on-hold (and typical pre-Expiration week rebounds) with our view of it 'at risk' for late in the week. This continued (for a myriad of reasons besides technicals) on Monday; with a fluctuating downward consolidation on Tuesday, ahead of the Fed decision; of course then the spike and opportunity to again fade it for downside action.

With prayers for victims,

Gene

Gene Inger

www.ingerletter.com