Gene Inger's Daily Briefing - for Friday, September 9, 2016

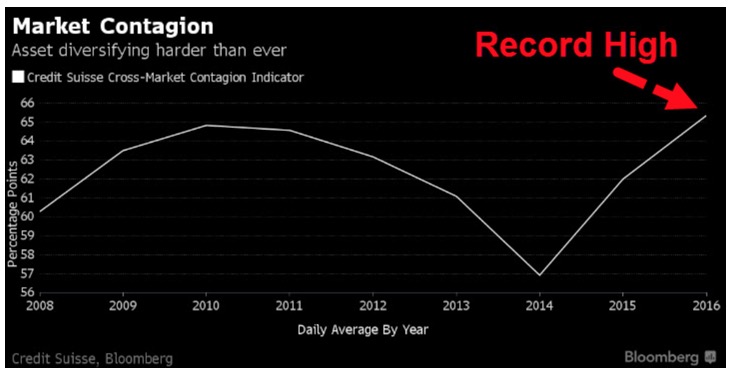

Cross-asset 'contagion' risk - grows increasingly by virtue of central banks that constantly intervene to sort of 'drive everything'. As we mentioned a couple days ago; Japan is 'evaluating' whether to continue their monetary policy. Yesterday an odd remark from ECB suggested the same may follow the next stimulus round so I put traders on-alert to prepare for yet-another (this time more enduring) break.

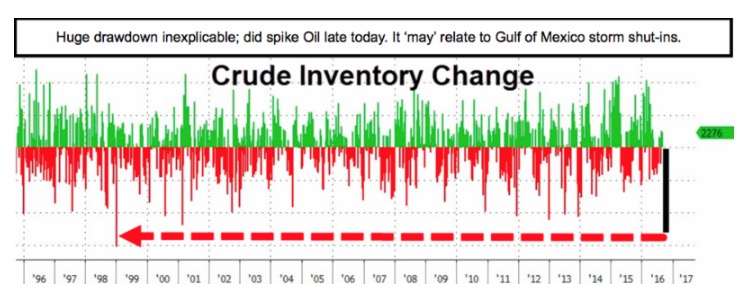

I also noted that Oil moved up not because of Hurricane Hermine so much, as the soaking floods over several weeks impeded refinery operations in Louisiana, and Texas; and that (not the Hurricane particularly) interrupted deliveries to and from refineries for both oil inbound, and gasoline outbound. This also impacts markets beyond Oil stocks; interesting as it comes as a disconnect from global supply. It's just one of many disconnects or aspects as the market persists in a high range. It was 'not' increased demand as permabull pundits pretend.

Tonight we have a two-part final as all week I believed Thursday the last good day in the morning to get short (we've had several trading gains earlier in the week) to my reflections on what I consider increasingly a new 'Epic Risk' from several types of bubbles, that generally have unfolded through decades, including those years of our extreme bullishness (majority of my market years while calling the 1987 break; the 2000 'crash'; the 2002 low; then bullish into 2007; shakeouts in-between).

Tonight we have a two-part final as all week I believed Thursday the last good day in the morning to get short (we've had several trading gains earlier in the week) to my reflections on what I consider increasingly a new 'Epic Risk' from several types of bubbles, that generally have unfolded through decades, including those years of our extreme bullishness (majority of my market years while calling the 1987 break; the 2000 'crash'; the 2002 low; then bullish into 2007; shakeouts in-between).

After 2002 we were again bullish for five solid years until my February of 2007 call for a 'liquidity and credit' crisis, which I escalated to an 'Epic Debacle' call in May of that year, before either Bear Sterns or Lehman of the ensuing year. Back in the 2005-'06 time, we talked of collapsing real estate pushing money into stocks, say for another year or so, because money's always looking to go somewhere.

As it turns out that happened. I'm recalling this because of the Wells Fargo fine for incredible fraud in their mortgage operations; which had a massive scope. (More.)

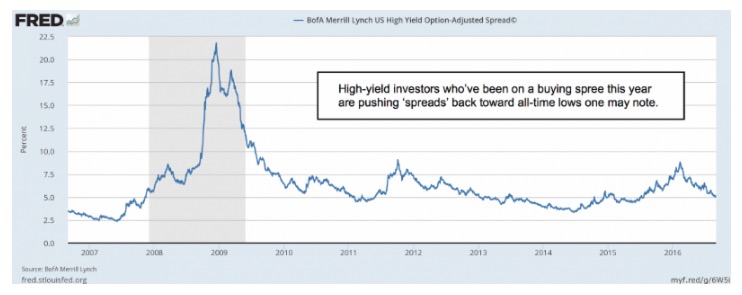

So it's not just this; but it strikes me recent market overall behavior is ever-more a dangerous leveraged bubble that can be popped by any of several factors. We may not even need a 'black swan' interloper; as all it takes is algorithmic selling in any condition (it could be the BoJ changing policy; but doesn't have to be); to prick this bubblelicious market. Risk is rising as the inability of the Street to take it higher when they try, is increasingly evident. So I am going ahead and suggesting what I'll just call a 'Cycle Shift' debacle warning. 'This is an 'Epic Cycle Transition'.

Bottom-line: the videos describe it technically. Generally I've previously described distribution; noted risk of a super-cycle ending; and this week, in a projected post Labor Day rally, we expected it to fail to ignite, and anticipated this week as a point worthy of quantifying this into more of a warning that risk is rising not ebbing.

This is based on everything from overdone monetary policies to demographics as (redacted) gasp of trade advantages that can be massaged by politicians to justify the ongoing relationship with China (and that's not helped by Alibaba's Jack Ma suggesting a China threat to the United States, and he used the word 'war', if we attempt to impose restraints or tariffs, ie: protectionism, on Chinese goods -more-). Good for him defending their stance; but recognize where this is going. It's a threat should we at this late date start unwinding (reserved for our subscribers; join!).

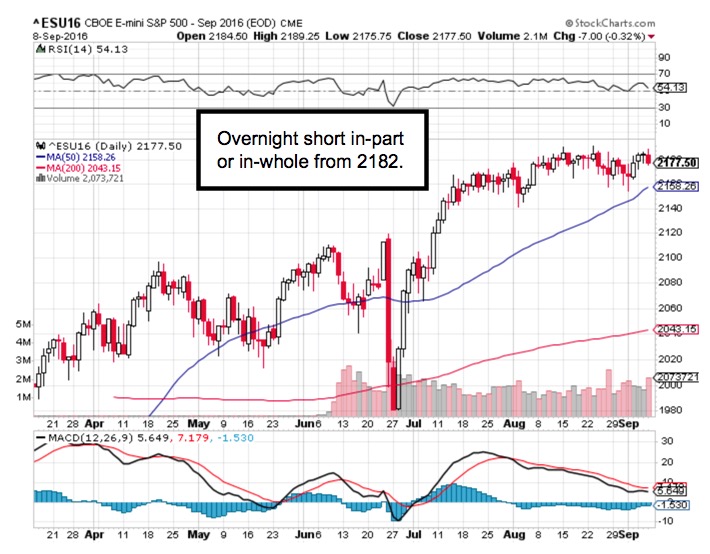

For now we're short Sept. S&P overnight from 2182 or so; with a breakeven stop.

Daily action - the benchmark for this market is the lower lateral supports we've outlined for the S&P. The upside potential is seriously irrelevant for now. (More.)

An intraweek rally after Labor Day was the expectation; the idea was it could fade as soon as Thursday. (Reserved); so we're thinking the market fades going into the weekend.

An intraweek rally after Labor Day was the expectation; the idea was it could fade as soon as Thursday. (Reserved); so we're thinking the market fades going into the weekend.

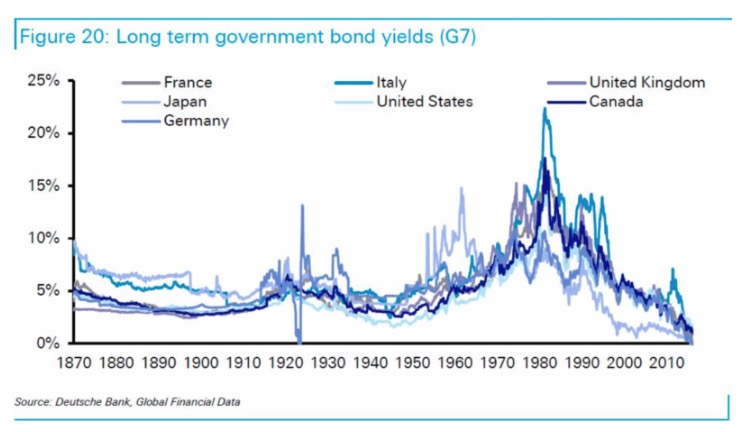

A 'bloodbath' is too strong a term to describe the Bond sell-off today; but gives just a hint of what is out there should rates rise (note the short term Treasury moves). I note it's not just Apple or the non-reporting of first weekend sales (they'll sell out, especially of the iPhone 7 Plus in Jet Gloss Black 128 GB we'd presume for a bit). (A couple paragraphs about Apple's product and warning of decline reiterated at the same time I explore 'benchmarks' of iPhone 7 Plus; which I order annually as I appreciate performance and camera improvements more than mere design style.)

Oh we were talking about Bonds. You had what looked like panic selling in Japan (I should say out of Japan) which combined with Draghi's not moving, to increasing pondering over monetary policy. That's potentially global disruptive. We warned.

For now holding short (in-whole or more-likely in-part) Sept. S&P from 2182.

Prior highlights follow: (generally the early week build-up to what I summarized and is mostly redacted in fairness to subscribers... I won't call others 'freeloaders', but do appreciate understanding we should be compensated for our work in what has been an incredible year during which we've correctly assessed market 'tension' and distribution; including the sell-offs from various spikes. Kindly join us.)

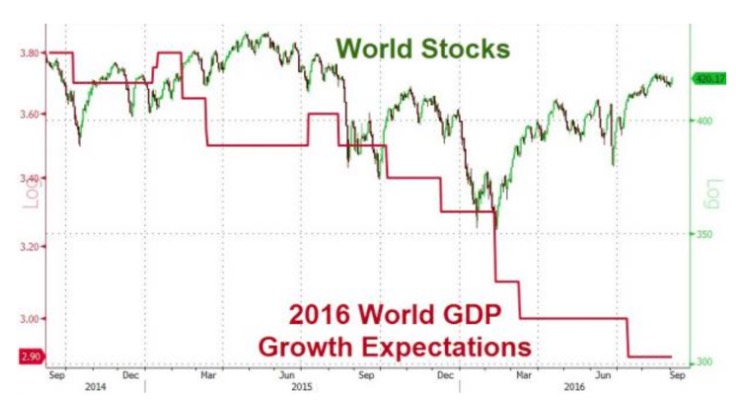

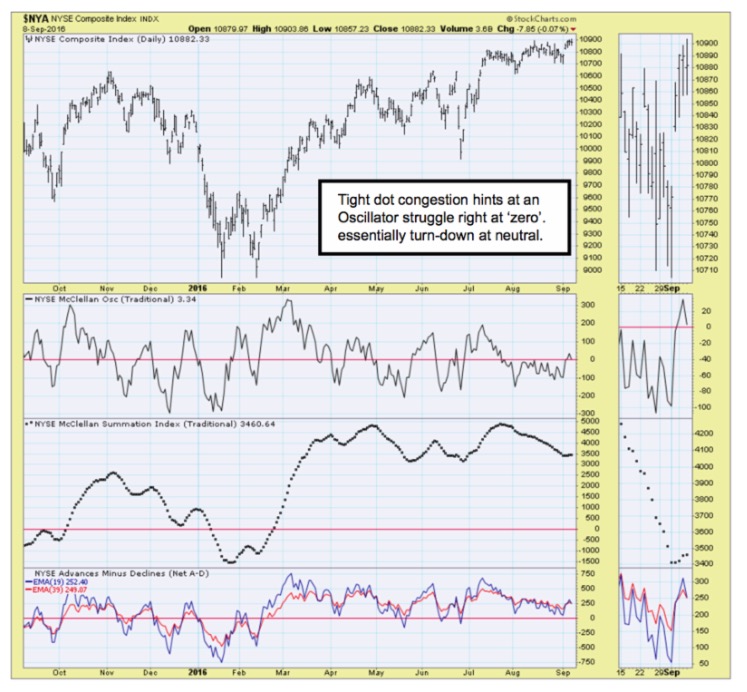

Tension on the tape - has masqueraded as 'serenity' over the past two months, in which S&P moves have actually traded in the tightest pattern of over 20 years!

Little noticed, is that the overall trading range of this year since the rebound from our projected huge January swoon that started the year (an enormous downside gain) achieved the lowest volatility for such a multi-month time in over 100 years. We suspect the January swoon (and a smaller one in the Spring) will prove not to be just isolated experiences. That's a fear tension prevailing more recently subtly conveys concern, which is interpreted as 'climbing a worry wall', but it isn't.

That's because there are low expectations; enough fear to run-in shorts whenever the market shakes-out a bit, and little follow-through, because investment-horizon investors are looking to build liquidity (or reduce their own exposure) on the rallies.

To wit: you get downside probes like twice in the past two weeks that are nullified by rebounds; and then you get rebounds that even breakout slightly (like Tuesday) with no meaningful follow-through. Beneath the serenity there is palpable tension.

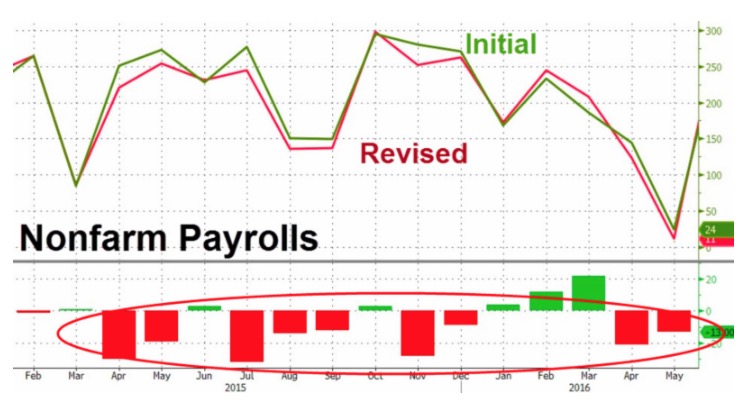

Bottom-line: markets are too 'serene' on the surface, while tension on the tape is masked by institutions applying a liberal dose of 'leverage' whenever needed. It is exactly how you get 'drawdowns' by wealthy investors from funds recently; while the Indexes manage to hold up. That suggests that while 'retail' margin may have eased a bit; 'institutional leverage' (excluded in retail margin data) increased.

Bottom-line: markets are too 'serene' on the surface, while tension on the tape is masked by institutions applying a liberal dose of 'leverage' whenever needed. It is exactly how you get 'drawdowns' by wealthy investors from funds recently; while the Indexes manage to hold up. That suggests that while 'retail' margin may have eased a bit; 'institutional leverage' (excluded in retail margin data) increased.

A 'September to remember' - may be in the cards. Tonight's focus in on the Fed; and was intended to continue our exploration of their impact on our economy, and global prospects, even before today's ruckus between the politicians as to whether or not the Fed belongs in the campaign (it absolutely does, as I'll delve into a bit). I also want to review this for new members (redacted here; as summarizes it all.)

(Large redaction) That's why I've said monetary policies are not only dangerously counterproductive after 'emergency' needs years ago; but reflect what the Fed has done 'to us' rather than 'for us'.

(Reserved section, as) they've got to, as this isn't going to be a placid world with the business cycle outlawed. So complacency and ignoring the topic won't fly well.

In-sum: we've discussed these issues for a long time; and been critical of political restrains against discussing the disconnect between markets and economic reality for the American people 'overall'. I began preparing this topic before' all the furor erupted between Trump & Clinton's views on discussing monetary policy. Leaving it 'as is' may seem promising for the monetarist/globalist crowd; but dangerous as hell; is my interpretation of non-partisan Congressional Budget Office reports.

Why in a nutshell? High and rising debt (entire redaction); as the Chairman of the Joint Chiefs once said; economic stability is a key National Security issue.

Battlegrounds continue 'fluid', with multiple dynamics unfolding with downside risk now.

If you're a long-time guest 'highlights' reader, kindly join as a regular member during the anticipated 'process' of increased market volatility.

Enjoy the weekend!

Gene

Gene Inger