Complacency is not an option for evaluating pandemic risk, as relates to potential economic disruption and market impacts. As I discussed with the midday video, the comparisons with the 2003 SARS virus aren't valid; as those arguing how quickly the S&P recovered "then" clearly overlook a depressed market at the time (after the then-forecast 1999-2000 peak as well as the ensuing bounce failure coincident with the barbarian attack on the United States). We turned bullish in 2002 and used that drop to buy at the time, and were solidly bullish until forecasting 2007's "Epic Debacle."

Now as to the risk of a "global public health emergency;" China continues to be pretty transparent and proactive (that's great), but it's spreading as I noted not only to Scotland now but also to Mexico City from a passenger that arrived on an American Airlines flight to LAX. So now you have personnel in an effort to decontaminate areas around arrivals in Los Angeles (patient condition or diagnosis is as yet unconfirmed).

Now as to the risk of a "global public health emergency;" China continues to be pretty transparent and proactive (that's great), but it's spreading as I noted not only to Scotland now but also to Mexico City from a passenger that arrived on an American Airlines flight to LAX. So now you have personnel in an effort to decontaminate areas around arrivals in Los Angeles (patient condition or diagnosis is as yet unconfirmed).

The point is simply that we clearly hope this is contained; but, regardless, it is taking a toll on travel and related businesses (casinos, cruise ships and of course airlines). Macau is considering closing ALL casinos temporarily if need be, and that's just an example. Load factors on all flights to Asia at this time are very light, with travel deferred where possible. The US State Department has issued a statement asking travels to China to "reconsider their travel plans," where previously State had only urged "caution."

The point is simply that we clearly hope this is contained; but, regardless, it is taking a toll on travel and related businesses (casinos, cruise ships and of course airlines). Macau is considering closing ALL casinos temporarily if need be, and that's just an example. Load factors on all flights to Asia at this time are very light, with travel deferred where possible. The US State Department has issued a statement asking travels to China to "reconsider their travel plans," where previously State had only urged "caution."

So it's a big deal and, while it may well be contained, some plans clearly change regardless; many holidays or business travel will be deferred until matters are clearer (and the safety of traveling is stabilized). Market behavior deals with overbought S&P conditions anyway, with correction prospects clearly outlined - likely in this time-frame and/or early February.

So it's a big deal and, while it may well be contained, some plans clearly change regardless; many holidays or business travel will be deferred until matters are clearer (and the safety of traveling is stabilized). Market behavior deals with overbought S&P conditions anyway, with correction prospects clearly outlined - likely in this time-frame and/or early February.

Of course, the S&P won't give up on a time, as this is a process over well a period of time. And the answer to quarantine's success in China also is not a situation that will be resolved on a dime either, but will be known in the fullness of time. Patience required.

Of course, the S&P won't give up on a time, as this is a process over well a period of time. And the answer to quarantine's success in China also is not a situation that will be resolved on a dime either, but will be known in the fullness of time. Patience required.

Midsession (intraday overview) MarketCast

Daily action found the S&P (and other stocks too) rebounding ideally in the manner outlined intraday; albeit not impressively. This was generally the idea of an irregular market struggling to recover after selling squalls.

Tonight's commentary is widely covered by videos, with expectation for more of the same irregularity on Friday. Then it will become perhaps more interesting, especially given Chinese New Years occuring; and *if* China continues to report vastly more cases (as is quite likely), they'll be able to cover the financial impact on growth (already felt in their markets) to some extent, given that most of their markets will be closed for a week.

The U.S. markets may more realistically reflect the world's sluggishness, with a more solid focus on domestic-centric stocks. While I don't know the details of *how* things will be evaluated, the story about FICO scoring to be changed in ways that will downgrade the credit-worthiness of many middle Americans; I do see that as a sobering factor in this consumer or spending-driven world.

Perhaps this is intentional to allow the Fed staying with low interest rates into the forthcoming (after we get through travel or other inhibiting factors related to the epidemic) period of global recovery and growth, without the low rates inviting consumers to overextend themselves further. We'll have more on this another time.

Meanwhile, we do take the uncertain prognosis for the virus seriously; so that I called it a "China Syndrome." The real syndrome may be avoidance of unnecessary travel and mass gatherings; that can easily affect the United States too, if we have just a handful more cases. It's psychological even if there's not a huge contagion in this country. We hope there's not anywhere; but given this was only identified 3 weeks ago, odds do favor a poor prognosis for getting a handle on this as quick as we all want.

Meanwhile, we do take the uncertain prognosis for the virus seriously; so that I called it a "China Syndrome." The real syndrome may be avoidance of unnecessary travel and mass gatherings; that can easily affect the United States too, if we have just a handful more cases. It's psychological even if there's not a huge contagion in this country. We hope there's not anywhere; but given this was only identified 3 weeks ago, odds do favor a poor prognosis for getting a handle on this as quick as we all want.

Prior highlights follow:

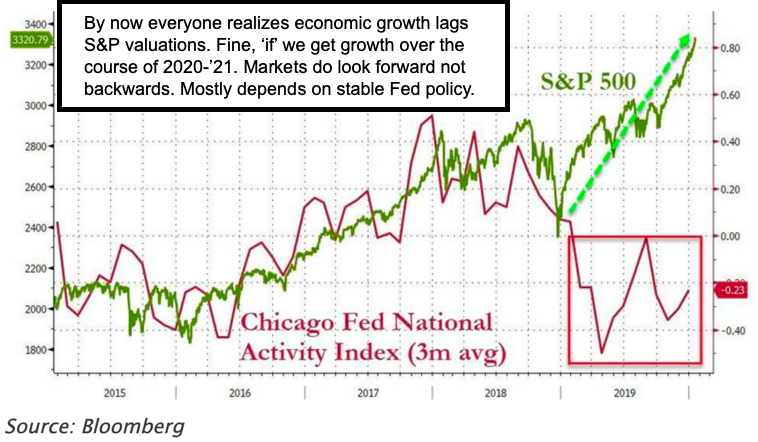

Situational awareness has lots of folks, not just market traders, slightly on edge, as they consider the expensive S&P (not so much broader stock markets) as a further restraint on growth by virtue of the Chinese virus (a notch away from becoming a pandemic) or a domestic political backdrop (probably the least of influences) as evolving into tense deliberations.

We're not advocating complacency towards these issues; but realize to a degree you've got investment managers simply buying stocks regardless of the backdrop; thus based solely on money flowing in as well as a slight glance at the technical continuation pattern that certainly does not trigger any real sell indications (part of why I said Tuesday was really nothing).

We're not advocating complacency towards these issues; but realize to a degree you've got investment managers simply buying stocks regardless of the backdrop; thus based solely on money flowing in as well as a slight glance at the technical continuation pattern that certainly does not trigger any real sell indications (part of why I said Tuesday was really nothing).

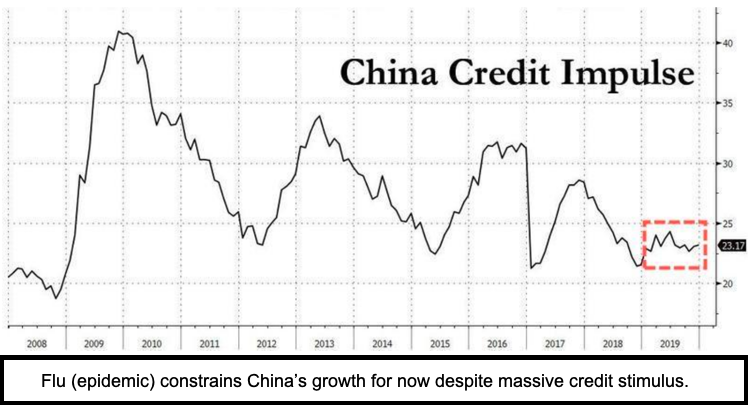

I am increasingly concerned, however, that what I will call the potential flu epidemic (pandemic or not) quickly devolves into a real threat to optimism among travelers and tourists, even if it's only for the short-term (hence its ability to take a notch out of Q1 revenues for many consumer-based firms that would be impacted; from hotels, casinos, cruises, airlines, etc.).

I am increasingly concerned, however, that what I will call the potential flu epidemic (pandemic or not) quickly devolves into a real threat to optimism among travelers and tourists, even if it's only for the short-term (hence its ability to take a notch out of Q1 revenues for many consumer-based firms that would be impacted; from hotels, casinos, cruises, airlines, etc.).

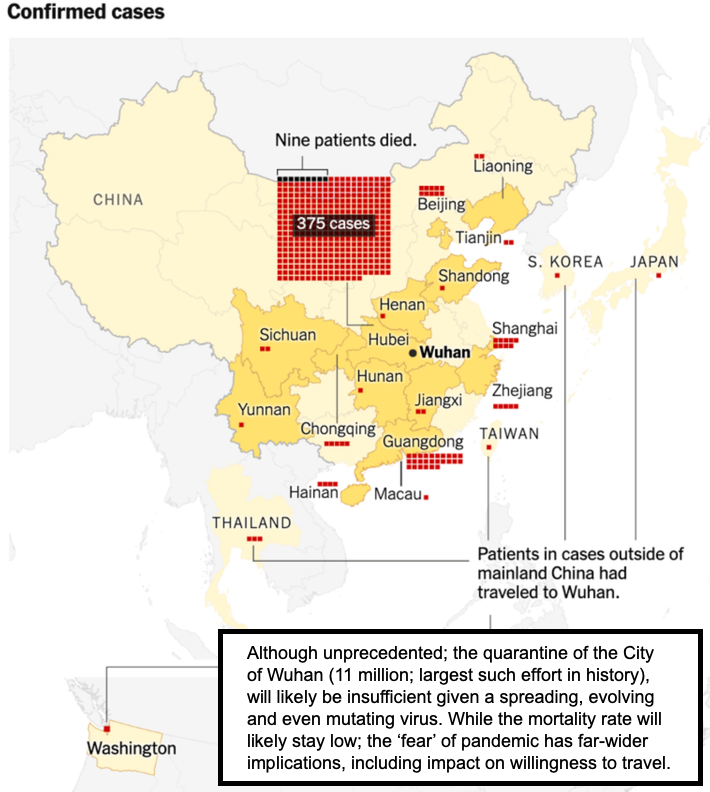

We won't know for a period of time if the sole American case near Seattle is a "patient zero" for North America. But while media notes they "checked the other travelers," since it's a 2-3 day incubation period, any passenger on that flight could not "present" with symptoms for another day or two. So, of course, our fingers are crossed that this has been contained; but, given that Wuhan in China is 11 million people, and other cities have patients at this time, with flights being curtailed later (if at all), we'd be cautious.

We won't know for a period of time if the sole American case near Seattle is a "patient zero" for North America. But while media notes they "checked the other travelers," since it's a 2-3 day incubation period, any passenger on that flight could not "present" with symptoms for another day or two. So, of course, our fingers are crossed that this has been contained; but, given that Wuhan in China is 11 million people, and other cities have patients at this time, with flights being curtailed later (if at all), we'd be cautious.

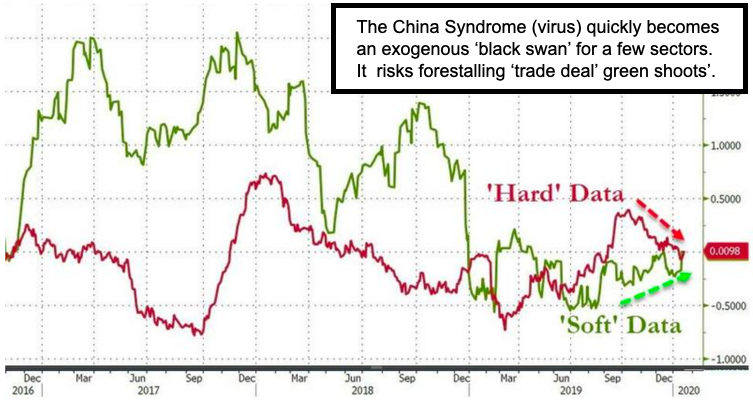

So, while the CDC is still evaluating (properly), from a market perspective I think we should declare it a potential Black Swan: a "China Syndrome." (And sure; we hope it's just an alert and no "meltdown" of the core of CDC or other healthcare efforts took place; but our first clue was a day ago when Cathay Pacific started offering hazmat suits to flight crew members. Actually, the Chinese Government has been very proactive and upfront about this, as is not their characteristic response; that suggests very real concerns.)

So, while the CDC is still evaluating (properly), from a market perspective I think we should declare it a potential Black Swan: a "China Syndrome." (And sure; we hope it's just an alert and no "meltdown" of the core of CDC or other healthcare efforts took place; but our first clue was a day ago when Cathay Pacific started offering hazmat suits to flight crew members. Actually, the Chinese Government has been very proactive and upfront about this, as is not their characteristic response; that suggests very real concerns.)

None of this recent market strength should deter prospects appearing of a more notable shakeout (even if only short-term) on the horizon, as I've discussed; somewhere in February's first half is a possibility, although there are so many variables that that's nothing to bank (or bet) on. Of course, if a pandemic is declared, it happens sooner vs. later.

None of this recent market strength should deter prospects appearing of a more notable shakeout (even if only short-term) on the horizon, as I've discussed; somewhere in February's first half is a possibility, although there are so many variables that that's nothing to bank (or bet) on. Of course, if a pandemic is declared, it happens sooner vs. later.

Now let's focus a bit on politics. Today, a Poll now has Michael Bloomberg as number 4 in the Democrat race; all that says is that more voters in that Party are leaning towards "centrist" candidates that the market would prefer. Again my personal preferences are irrelevant. The point is (like we said in 2016 with the "if Trump wins, even if you love Hillary, you have got to put your money 'in' the market, as it will go to the Moon")... the point is that *the market* is more likely to be stable if candidates on *both* sides of this contest are viewed as not destabilizing American growth prospects.

Now let's focus a bit on politics. Today, a Poll now has Michael Bloomberg as number 4 in the Democrat race; all that says is that more voters in that Party are leaning towards "centrist" candidates that the market would prefer. Again my personal preferences are irrelevant. The point is (like we said in 2016 with the "if Trump wins, even if you love Hillary, you have got to put your money 'in' the market, as it will go to the Moon")... the point is that *the market* is more likely to be stable if candidates on *both* sides of this contest are viewed as not destabilizing American growth prospects.

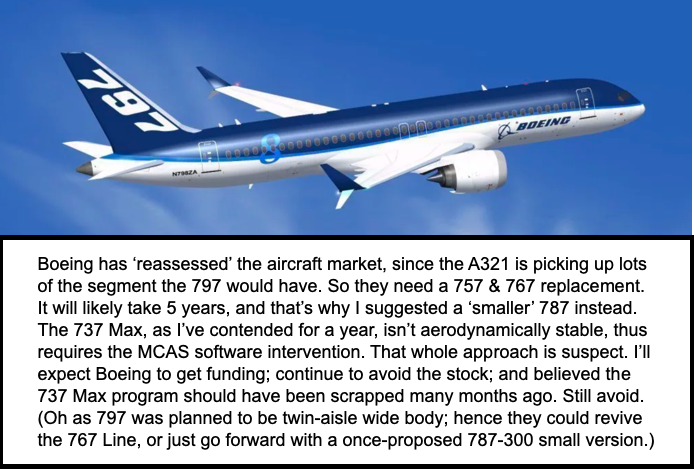

To be cute; that means not "reinventing the wheel" or hiking taxes. I could not resist that, since the President in his CNBC interview this morning did say we should support Thomas Edison and guys who invented stuff, like "the wheel." That was amusing, but I think he was referring to Elon Musk. I must also touch on Boeing, via the charts below.

To be cute; that means not "reinventing the wheel" or hiking taxes. I could not resist that, since the President in his CNBC interview this morning did say we should support Thomas Edison and guys who invented stuff, like "the wheel." That was amusing, but I think he was referring to Elon Musk. I must also touch on Boeing, via the charts below.

In-sum: Market vulnerabilities are actually increasing; more below.

In-sum: Market vulnerabilities are actually increasing; more below.

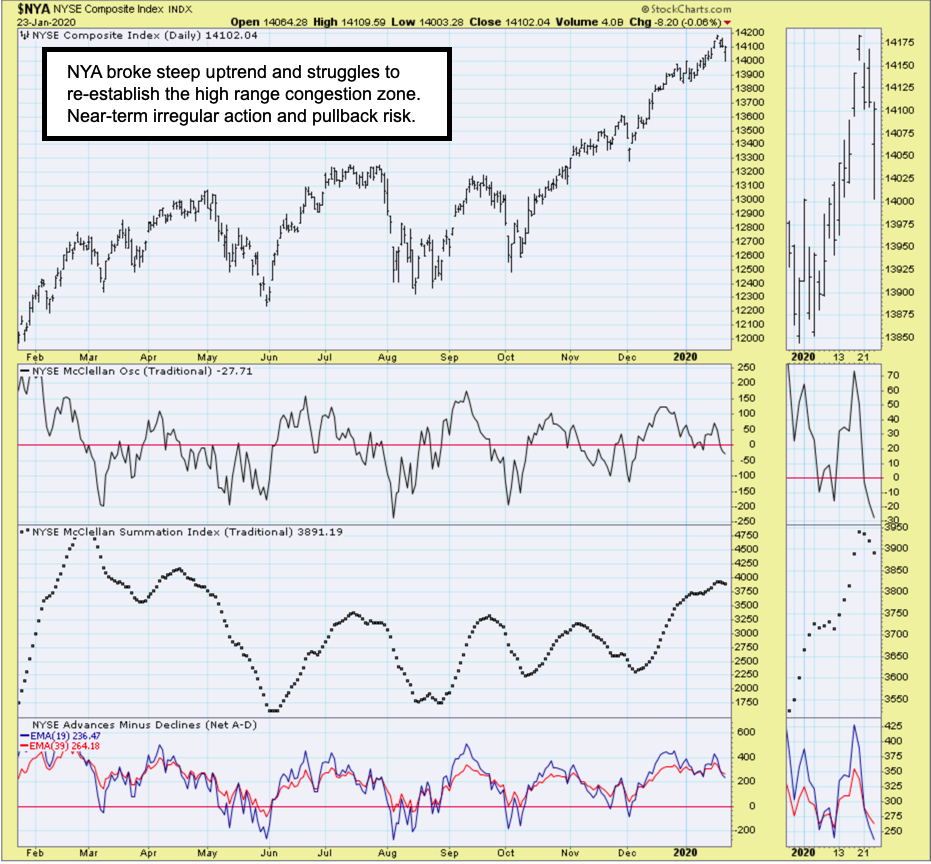

(Macro) action clearly warned about a coming correction; that might seem like what everyone suggests, except we've been optimistic throughout as regards the reasons for the technical ability to evolve and bifurcated stock market that really has not seen the classic euphoria elements to a peak.

I have nevertheless pointed-out the prospect of a correction by the first half of February, beyond the mild intraday dips seen thus far. Of course, what happens in China (and how it spreads) matters in so many ways beyond simply the near-term movement of the S&P.

I have nevertheless pointed-out the prospect of a correction by the first half of February, beyond the mild intraday dips seen thus far. Of course, what happens in China (and how it spreads) matters in so many ways beyond simply the near-term movement of the S&P.

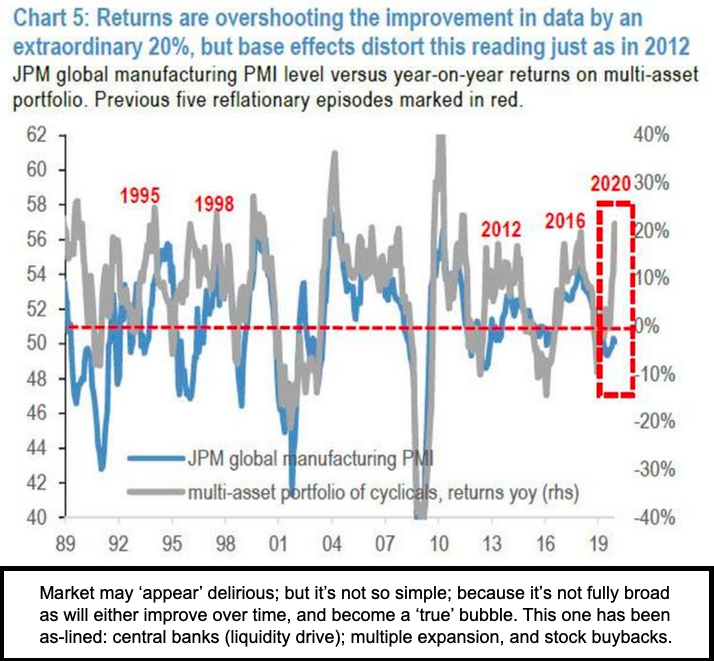

Special notes: first I'd like to express appreciation to stockcharts.com for years of allowing us to share several charts. And I'd like to thank Erin and Carl Swenlin for occasional quotes of my views over the years thru their Top Advisors column. Now I congratulate their new decisionpoint.com website, and look forward to occasionally sharing pattern analysis charts (plus my perspective at times, like in tonight's first chart).

Special notes: first I'd like to express appreciation to stockcharts.com for years of allowing us to share several charts. And I'd like to thank Erin and Carl Swenlin for occasional quotes of my views over the years thru their Top Advisors column. Now I congratulate their new decisionpoint.com website, and look forward to occasionally sharing pattern analysis charts (plus my perspective at times, like in tonight's first chart).

(I want to note Carl is a long-time warrior of markets too; we truly valued a long-ago inclusion in their DecisionPoint section of CompuServe back in the 1980's, when I was a mere child. It then moved to AOL before settling at Chip Anderson's StockCharts.com, where they continue contributing.)

Next, I'd like to thank 'The Money Show' folks for inviting me to speak at The Florida Money Show at the Omni Champions Gate near Orlando on Saturday February 8 at 3:30 pm. It's an open forum where my focus this time (as it turned into in Las Vegas) will be not just market behavior, but discussing 'cardiovascular risk reduction' as relates to Amarin.

Next, I'd like to thank 'The Money Show' folks for inviting me to speak at The Florida Money Show at the Omni Champions Gate near Orlando on Saturday February 8 at 3:30 pm. It's an open forum where my focus this time (as it turned into in Las Vegas) will be not just market behavior, but discussing 'cardiovascular risk reduction' as relates to Amarin.

I'm not a doctor; just recognize the results from taking Vascepa, so most of my enthusiasm is based on personal experience (as a patient) finding the pill before the stock, as perhaps giving a perspective on importance we discussed here often. There will be no information I've not addressed, but please say hi if attending. Besides, they have a great golf course in case the weather is inviting.

Thursday's start will primarily be influenced by news (or lack) from China, of course. However, the expectation this week has been for rally efforts of limited success, and generally a defensive (or irregularly neutral) tone to the market. We think that's still the case as we approach increased risks on the global health, economic growth and political fronts. So, for the moment, the S&P has entered an "indecision pattern," but it's more like an absence of bids than markets reversing from bubble-like conditions.

Thursday's start will primarily be influenced by news (or lack) from China, of course. However, the expectation this week has been for rally efforts of limited success, and generally a defensive (or irregularly neutral) tone to the market. We think that's still the case as we approach increased risks on the global health, economic growth and political fronts. So, for the moment, the S&P has entered an "indecision pattern," but it's more like an absence of bids than markets reversing from bubble-like conditions.

Conclusion is similar: there's no catalyst to warrant committing new funds as yet, although I expected recent extensions and leaned very clearly towards a China Deal coming, with initially higher S&P records. If anything, I've been conservatively optimistic thru 2019 and reiterated the old sayings: "don't fight the tape", and "don't fight the Fed."

It's all on top of capturing the entire gain on the number 1 stock, AMD, and presumed additional gains ahead (over time) for Amarin. And, this year, the rocky start (fling sort of an S&P flail), followed immediately by a controversial undertaking in the Persian Gulf, has various aspects or outcomes that we'll try our best to follow as impacts markets.

We remain circumspect while market stresses were notably alleviated by making a "Phase One' deal with China (superficial it is not); while, of course, near-term Middle East chaos and now the "China Syndrome" throws wrenches into the behavior of the market and more uncertainties to contend with ahead.

Enjoy the evening;

Gene

Gene Inger