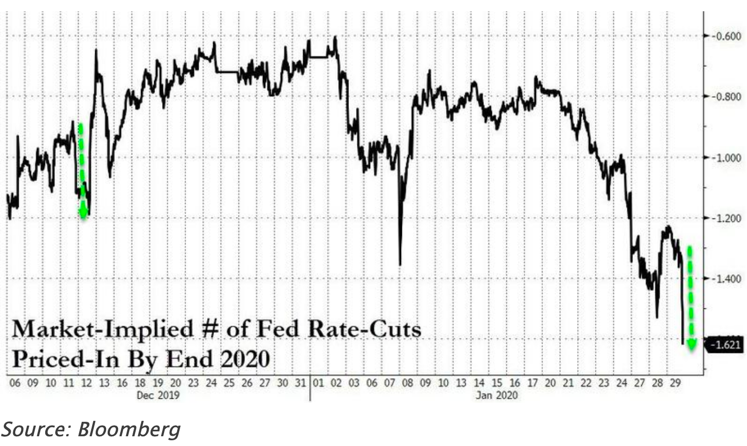

Beating around the bush with candor after the dovish Fed statement, Chairman Powell tried not to be backed into a corner about "reserve levels," liquidity injections, or their plan to start bringing things into balance later in the year (perhaps from April forward; though that may be optimistic).

Beating around the bush with candor after the dovish Fed statement, Chairman Powell tried not to be backed into a corner about "reserve levels," liquidity injections, or their plan to start bringing things into balance later in the year (perhaps from April forward; though that may be optimistic).

Clearly the Fed wants to make it all seem "administrative" in general, vs. a hands-on series of moves by the Open Market Committee; but, again, that is probably wishful thinking. The most one can draw out of it is generally, or as suspected, a Fed trying to remain accommodative, not rocking the rate boat excessively, and probably not retreating as they already would have, we think, desired (they said so too, and now just say fewer interventions while ready to do so depending on conditions).

Clearly the Fed wants to make it all seem "administrative" in general, vs. a hands-on series of moves by the Open Market Committee; but, again, that is probably wishful thinking. The most one can draw out of it is generally, or as suspected, a Fed trying to remain accommodative, not rocking the rate boat excessively, and probably not retreating as they already would have, we think, desired (they said so too, and now just say fewer interventions while ready to do so depending on conditions).

This was a very carefully balanced commentary with a focus on 2% rates of inflation; not "near" as they said before, but *to* the 2% level. Well, even that requires growth, which continues to be elusive with more unknowns related to the Chinese epidemic, and, with the lack of their contribution and timing of a recovery, fairly unknown. The Chairman was clear about that while he emphasized that about 85% of the U.S. economy is unrelated to trade (I'd not question that, because its always been 70% or more).

This was a very carefully balanced commentary with a focus on 2% rates of inflation; not "near" as they said before, but *to* the 2% level. Well, even that requires growth, which continues to be elusive with more unknowns related to the Chinese epidemic, and, with the lack of their contribution and timing of a recovery, fairly unknown. The Chairman was clear about that while he emphasized that about 85% of the U.S. economy is unrelated to trade (I'd not question that, because its always been 70% or more).

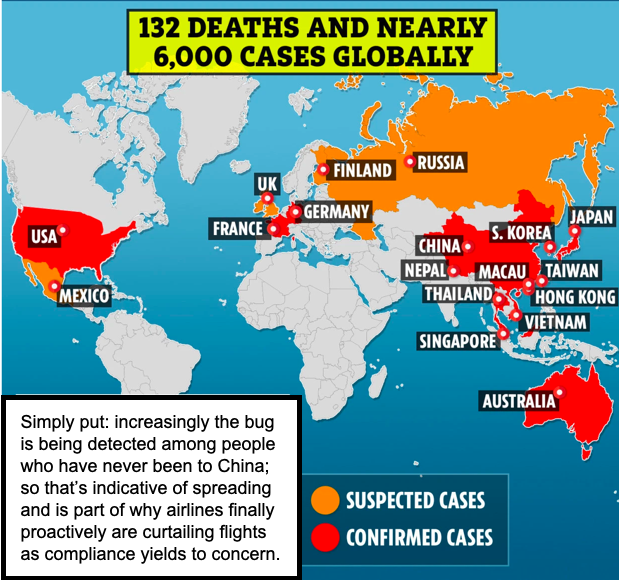

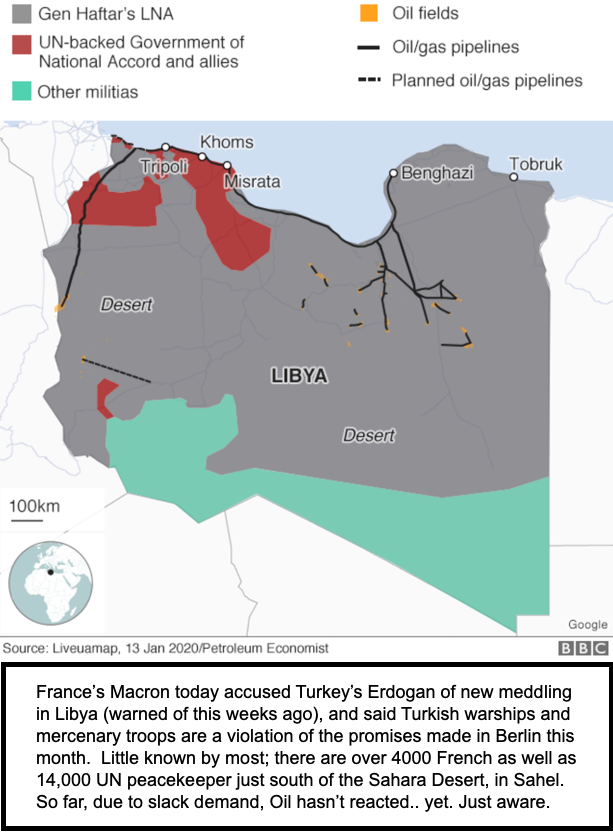

(Virus cases have increased by about 50% since this graphic.)

(Virus cases have increased by about 50% since this graphic.)

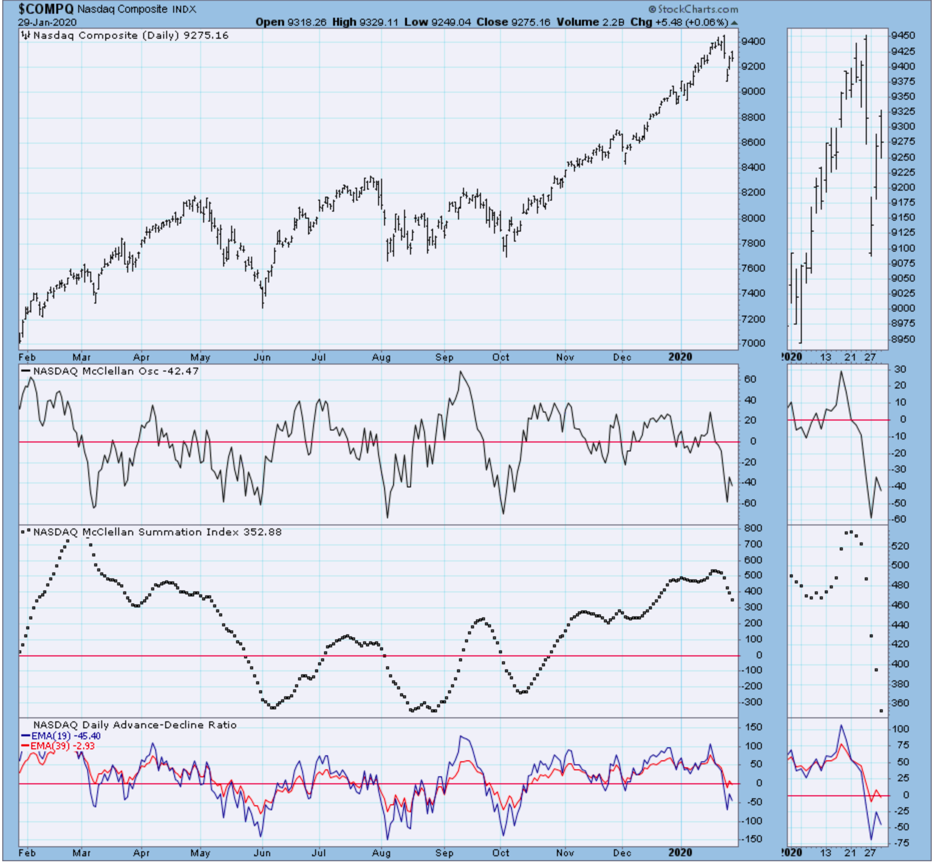

If earnings are taking center-stage in the market for now, then that's benign in a sense, given how the major Indexes and key stocks already are. In that respect, there's more prospects for accidents than victorious romps, as we look forward to February trading - a time-frame I've thought particularly vulnerable, and additionally sensitive (in either direction) to WuFlu news.

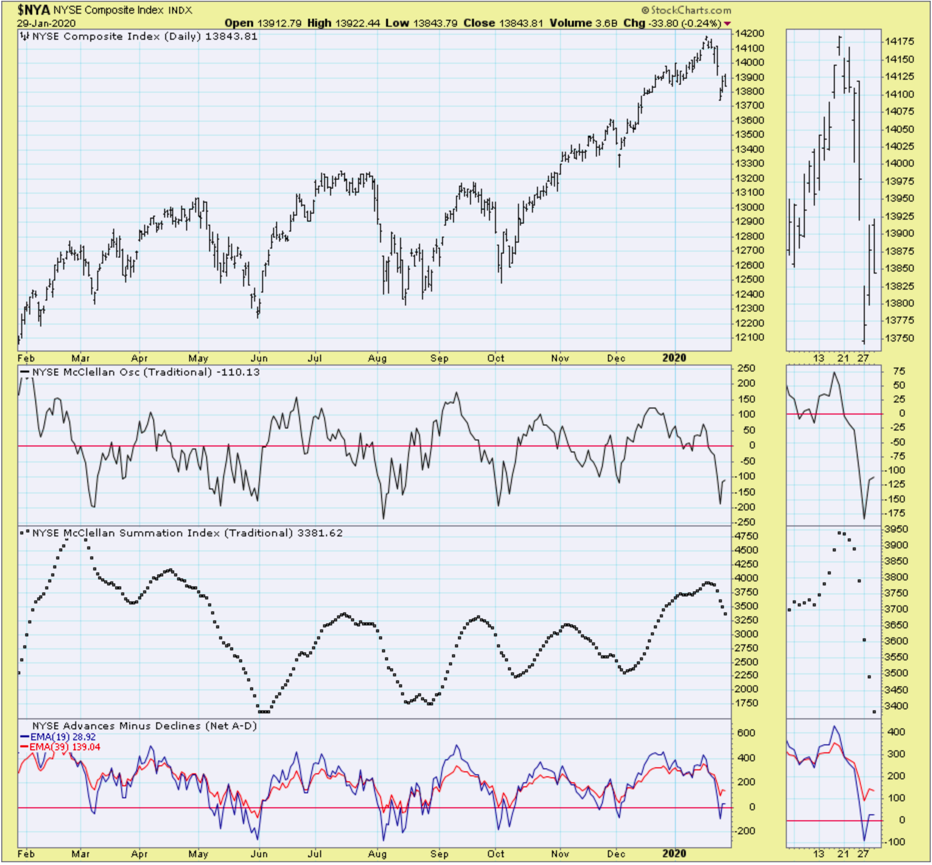

In-sum: We believed (and still do) that the market, or at least the S&P, is fairly exhausted with regard to upside activity after a moderate rebound in stock more mundane than the momentum leaders as 2020 began.

In-sum: We believed (and still do) that the market, or at least the S&P, is fairly exhausted with regard to upside activity after a moderate rebound in stock more mundane than the momentum leaders as 2020 began.

So yes, despite the short-term "rock & roll" related to the viral scare (and it matters for sure), and even rebounds should it miraculously be contained faster than most responsible folks believe likely... despite all that... we see the S&P nearer-term prospects pointing to at least a *sag* ahead.

So yes, despite the short-term "rock & roll" related to the viral scare (and it matters for sure), and even rebounds should it miraculously be contained faster than most responsible folks believe likely... despite all that... we see the S&P nearer-term prospects pointing to at least a *sag* ahead.

Turnover is amazing, so the different reactions to a Facebook and Tesla sort of reflect that today, although Apple remains the market key. There's little doubt that this is stretched - and it's because the market is dominated by ETF and "passive" approaches that you even have the Indexes holding as well as they are.

Turnover is amazing, so the different reactions to a Facebook and Tesla sort of reflect that today, although Apple remains the market key. There's little doubt that this is stretched - and it's because the market is dominated by ETF and "passive" approaches that you even have the Indexes holding as well as they are.

Overall, S&P bounced off the minimal retrenchment levels as we envision more downside as moving into February. We doubt earnings will really hold markets, so Facebook is defensive for a few reasons, while Tesla ran lots of short-sellers (that's for sure). The market is acting spiky.

Pre-close (intraday & Fed) MarketCast

Daily action retains some traction; it surrendered most as "taper tantrum" memories came back into traders' vision looking way forward (too soon in the year for sure, and maybe not even this year depending on China, plus the political considerations the Fed says never plays a role).

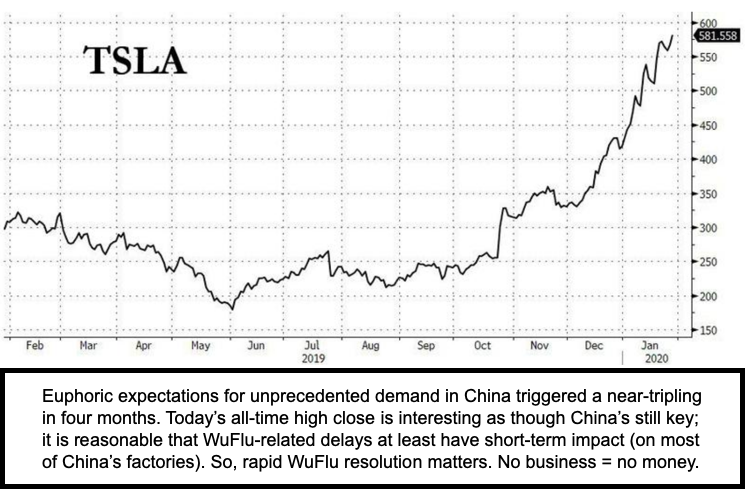

We may get another S&P and breadth shot a bit higher in the morning, on the back of Tesla's boost; although, there again, the extent of production interruption in the important Chinese market is unclear. That's not to say Tesla hasn't made it through the roughest spots; bears are now in full panic, as in not just shorts cover, but fanboys increasingly see it as a $1000 stock (and that's not out of the question).

We may get another S&P and breadth shot a bit higher in the morning, on the back of Tesla's boost; although, there again, the extent of production interruption in the important Chinese market is unclear. That's not to say Tesla hasn't made it through the roughest spots; bears are now in full panic, as in not just shorts cover, but fanboys increasingly see it as a $1000 stock (and that's not out of the question).

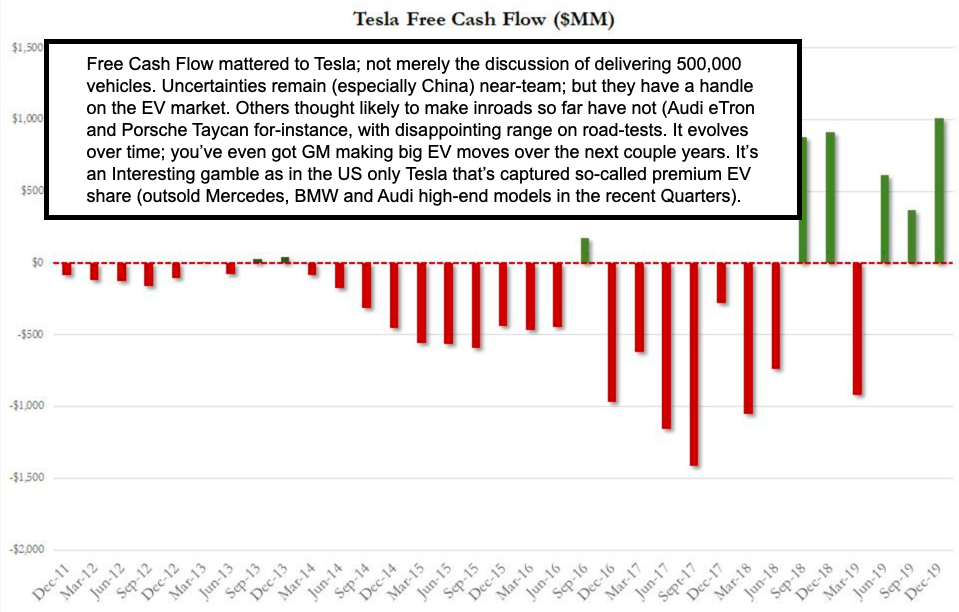

Ultimately, there will be competition in various EV price ranges, but, so far, guidance is solid, as others (despite throwing money at EV) actually are not comparably engineered. So Tesla deliveries will exceed 500,000 this year, and the new China factory *and* the coming "Berlin East" plant will of course be big deals, especially as Germany moves further to emphasize its incentives for EV, while also (little noticed in the U.S.) accelerating the plans to move away from coal-sourced power-plants. By the way, *if* Musk decides to use this move to raise more capital with a secondary, that's a possibility - but it wouldn't change the backdrop, which is now clearly more than just "buying a dream," as some still contend.

Ultimately, there will be competition in various EV price ranges, but, so far, guidance is solid, as others (despite throwing money at EV) actually are not comparably engineered. So Tesla deliveries will exceed 500,000 this year, and the new China factory *and* the coming "Berlin East" plant will of course be big deals, especially as Germany moves further to emphasize its incentives for EV, while also (little noticed in the U.S.) accelerating the plans to move away from coal-sourced power-plants. By the way, *if* Musk decides to use this move to raise more capital with a secondary, that's a possibility - but it wouldn't change the backdrop, which is now clearly more than just "buying a dream," as some still contend.

(It's not my favorite EV design now, but it has the range and experience that leaves the rest to catch it as time goes on. For instance, Volvo has 2 EVs coming, both of which I'd heard could have been out, but were delayed enough to be sure batteries are longer-range. Same for Volkswagen, after being burned by disappointing reception to Porsche and Audi's product launches. You have an interesting outlier where, at CES, a Mercedes engineer said Mercedes "isn't convinced electric is the way to go." Well his government in Berlin clearly is, so I'd say that's a spin for their delay. Oh, Mercedes' initial EV is a hybrid that looks like a regular SUV with a plug.) P.S.: it wouldn't surprise me if an up-and-down swing by Tesla associated a bit with a market reversal, but, again it's still a choppy range.

(It's not my favorite EV design now, but it has the range and experience that leaves the rest to catch it as time goes on. For instance, Volvo has 2 EVs coming, both of which I'd heard could have been out, but were delayed enough to be sure batteries are longer-range. Same for Volkswagen, after being burned by disappointing reception to Porsche and Audi's product launches. You have an interesting outlier where, at CES, a Mercedes engineer said Mercedes "isn't convinced electric is the way to go." Well his government in Berlin clearly is, so I'd say that's a spin for their delay. Oh, Mercedes' initial EV is a hybrid that looks like a regular SUV with a plug.) P.S.: it wouldn't surprise me if an up-and-down swing by Tesla associated a bit with a market reversal, but, again it's still a choppy range.

Meanwhile, for most stocks, valuation levels are generally high; even the Fed Chairman didn't deny it when asked (but shied from any decisions at the Fed they'd make that might influence markets; of course, we all know how policy-dependent this market is).

Meanwhile, for most stocks, valuation levels are generally high; even the Fed Chairman didn't deny it when asked (but shied from any decisions at the Fed they'd make that might influence markets; of course, we all know how policy-dependent this market is).

That's why it remains a TINA market. So, if China by some stroke of luck manages to contain the WuFlu spread within reasonable bounds (and I'm not yet confident of that), then the market can indeed breathe a sigh-of-relief. That would indeed reinvigorate the "There IS No Alternative" tone to market decisions. If so, speaking candidly, that might *then* be an excuse for a fairly robust Spring rally - but, in-between then and now, we have the S&P rough patches most likely to contend with.

Bottom-line: We're at a testy time for markets, certainly dealing with one of the riskiest "black swans" (WuFlu), but also preceding expectations as relate to valuation, and the last push-up; that created technical vulnerable conditions as we look into early-mid February.

Bottom-line: We're at a testy time for markets, certainly dealing with one of the riskiest "black swans" (WuFlu), but also preceding expectations as relate to valuation, and the last push-up; that created technical vulnerable conditions as we look into early-mid February.

Overreactions are even more likely than underreactions when it comes to market prospects on top of this rebound from the minimum levels we've outlined. Hence, barring some huge relief, we'd expect the S&P to horse around just a bit here and then give up some ground.

Prior highlights follow:

A rebound in stock prices, coincident with a free-fall in airline traffic, is not an oxymoron at all, but reasonably reflects the global situation. S&P futures, even Monday evening, gave hints for rebounds, both from overall movement to the rising bottoms pattern (see chart technical comments) and a degree of short-covering. Even Tuesday looks to start higher, while Hong Kong (just reopening) reflects the angst with a sharp decline.

Given this rising-bottoms S&P pattern, with extensions coming in the morning to a degree dominated by Apple's comeback (it's a surrogate for the market, as we often note), they'll try holding it together regardless of news, irrespective of nevertheless terrific earnings, and even if it takes longer than they'd like for production to normalize in China.

(FOMC Meeting is ongoing; not expecting change in rates; will assess.)

(FOMC Meeting is ongoing; not expecting change in rates; will assess.)

There's lots of effort to extend the expected rebounding market, but there are serious uncertainties looming too. It does NOT mean investors are focusing on earnings, as that's a little ridiculous - what matters is guidance at this point, and, for many global multinationals, that's pretty tough here. For Apple, it may be a plus this time of year, because they're about to wind-down iPhone 11 production and start shifting to iPhone 12 (with a next-generation, as yet-unreleased 5G Qualcomm chip set).

So, at worst, this allows them more time to enhance supply-chain prep for the assembly line and, if need be, push back the next series a bit (so now we know why the iPhone 12 will be sold-out within minutes of pre-sales in September; making it ludicrous to hear some analysts say demand is not going to be strong... it will probably be the most demand in years).

What's known today is that HHS & CDC have genuinely tried to reassure Americans in very appropriate ways, namely that WuFlu isn't rampant here at all (at least yet, and fingers are crossed that it never will be). And just after I commented that airlines will all by themselves reduce travel to China due to load load-factors, United came forth today and cut the majority of all of their flights (about 24) to all China destinations.

What's known today is that HHS & CDC have genuinely tried to reassure Americans in very appropriate ways, namely that WuFlu isn't rampant here at all (at least yet, and fingers are crossed that it never will be). And just after I commented that airlines will all by themselves reduce travel to China due to load load-factors, United came forth today and cut the majority of all of their flights (about 24) to all China destinations.

The U.S. is encouraging avoiding travel to China, but most companies for sure already have, and zero tourism is a non-issue to even mention. Late Tuesday, we hear The White House is telling airlines what I'd suspected this morning would eventually evolve: the U.S. may suspend all flights to to China. Period, full stop. (Aside from evacuation flights. China Airlines saying it may also do this voluntarily, and we've call for cutbacks for a few days now; not to mention the lost revenues from basically empty flights now.)

Where the WHO stands on this is variable; but at least (as I've mentioned before) this is a new era with Genomic Sequencing. Hence the makeup of the virus was posted as data by the Chinese, and the HIH (or associates) have already created and started to make a test-kit to definitively gauge if a patient (or even an asymptomatic carrier) has contracted the WuFlu as I term it.

Where the WHO stands on this is variable; but at least (as I've mentioned before) this is a new era with Genomic Sequencing. Hence the makeup of the virus was posted as data by the Chinese, and the HIH (or associates) have already created and started to make a test-kit to definitively gauge if a patient (or even an asymptomatic carrier) has contracted the WuFlu as I term it.

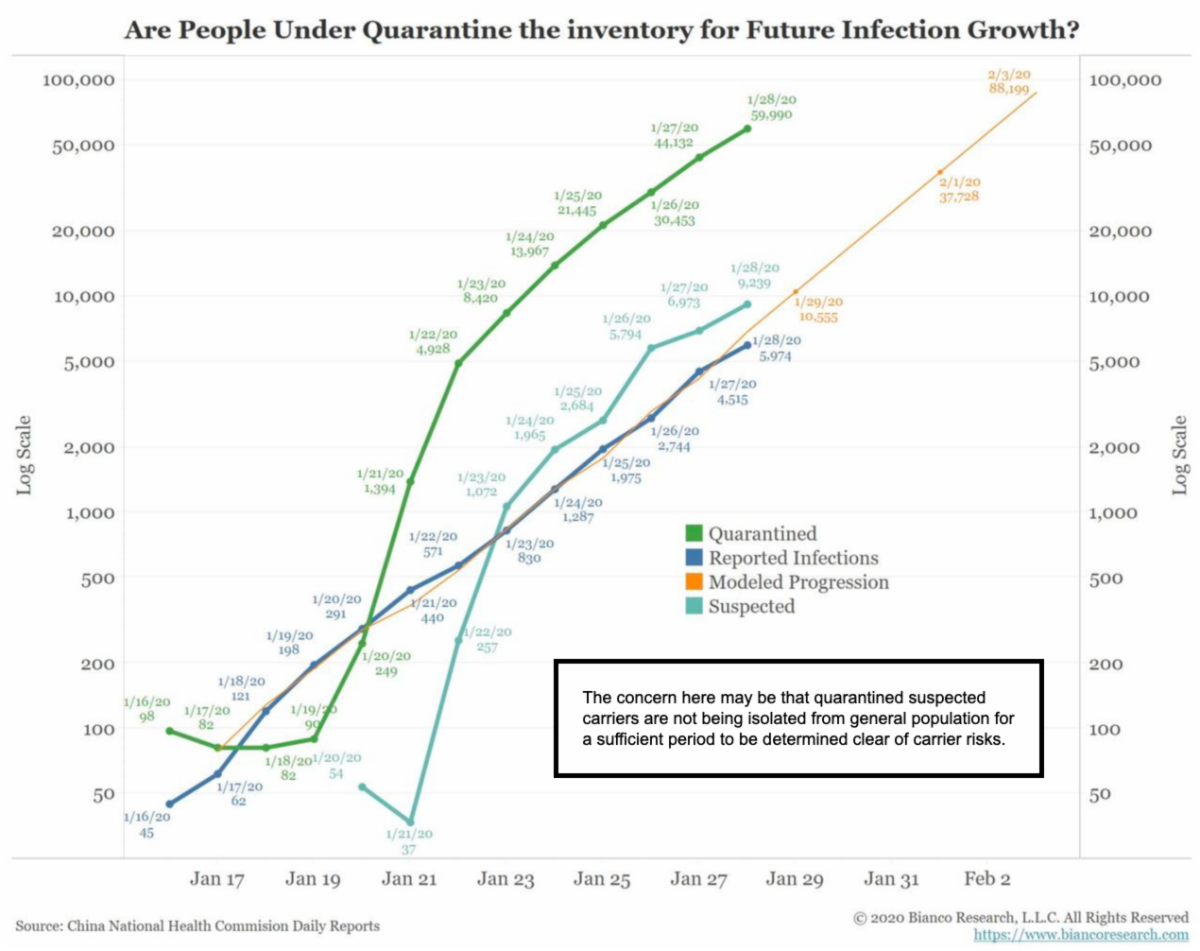

Meanwhile, the media is admitting building *more* prefabricated hospitals (we suspected the need was 100,000 beds, not a couple 1,000 bed units to be constructed), and by no means is this situation relaxed at all, even if the "shock factor" is absorbed temporarily by markets.

Remember: China's markets were scheduled to be closed for the holiday this week. One clue to how serious this remains in the view of Beijing will be the extension of closing periods for markets, which will be presented as a precaution from people gathering.

Remember: China's markets were scheduled to be closed for the holiday this week. One clue to how serious this remains in the view of Beijing will be the extension of closing periods for markets, which will be presented as a precaution from people gathering.

In-reality, that will largely be 'cover' for stress and anxiety of prices falling, given that most trading these days (globally) is largely electronic. But yes, for businesses (and virtually all factories) that require physical presence, the disruption will be enduring for awhile, and especially supply-chains.

In-sum: We were not surprised to see the rally, and expected it especially as it was a last-ditch short-term technical trend line support probe. However, that does not relate to sustainability, as many fluid factors are pending. We will highlight a few late developments (or summarize) in videos.

In-sum: We were not surprised to see the rally, and expected it especially as it was a last-ditch short-term technical trend line support probe. However, that does not relate to sustainability, as many fluid factors are pending. We will highlight a few late developments (or summarize) in videos.

(Macro) action saw a normal rebound looked-for, while having WuFlu for the most part attacked head-on is extremely gratifying to everyone. This is not a brief scare, even as markets try to make it seem that way. And it will not be surprising that the stability persists a bit longer.

Later, holding together really will depend on lack of both China and (it seems like under control in the U.S., but too soon to be clearly safe but we all want that to be the case...) what requires that degree of "confidence, not complacency" relates to worries of asymptomatic transmisability.

It is that single aspect that has medical professionals worried, and is why it will be required that even *returning evacuees* flying from China will be quarantined for 3 days before being released into the general population. And since the incubation period is estimated as 2-14 days, that might be insufficient, but who knows.

We do know that millions of people migrated out of Wuhan before it was closed down; thousands flew abroad, and not just to the USA; and we've got a few more days before one can remotely be confident that asymptomatic transmissibility isn't as worrisome as the authorities have suggested. For now, the complacency some have (including doctors reminding us of how many contract or die from the regular flu in the U.S. yearly) isn't justified.

For now, let's highlight some things of note (too many to talk of each):

- Least important first: the Super Bowl can be viewed this Sunday in full 4K resolution not on the regular Fox channel; but only if you have a streaming video service (such as Apple TV, Roku, perhaps Hulu or Smart TV) which lets you download the FOX SPORTS APP. Then, if it is partnering with your streaming provider, you can use your normal credentials when prompted to activate the App. That will be the only way to watch it in true 4k that we know of, as there is no broadcast or normal cable carriage in the 4k version, just 1080p (which is fine, but if you want to see it in 4k, you'll need the Fox Sports App, and I suggest setting it up now so you'll avoid the rush the day of the big Game);

Now, we'll go to other notable items as may or may not yet be mainstream but are worth mentioning in-brief (with no order for importance):

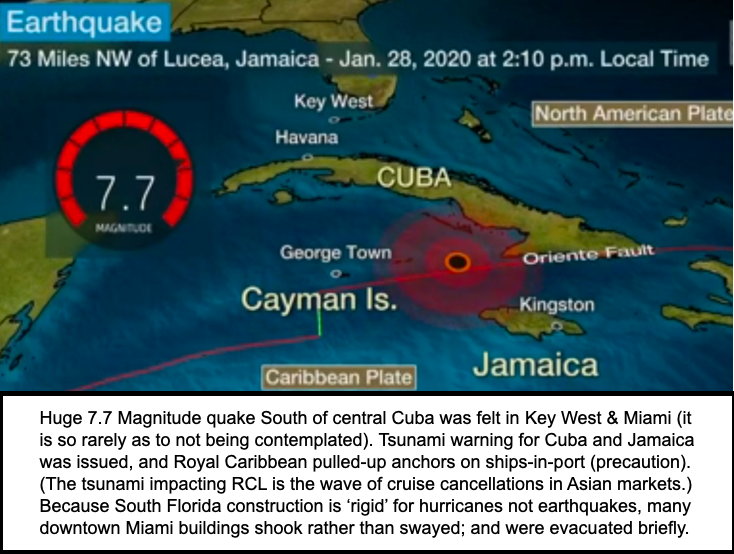

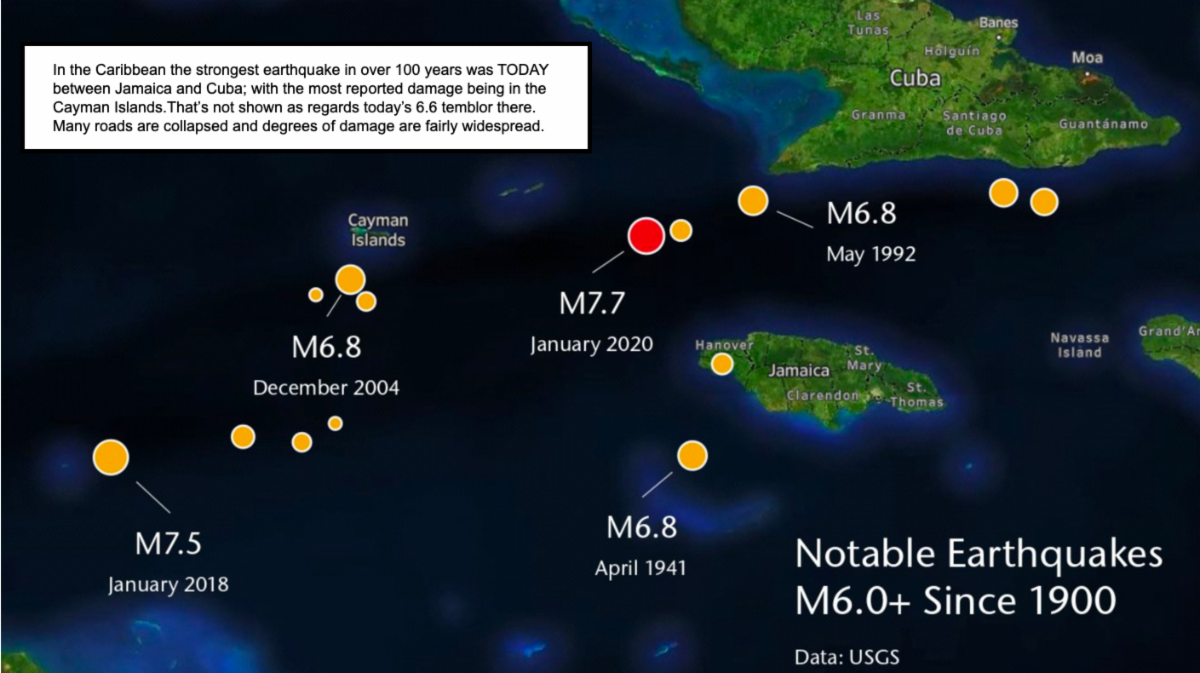

- The world continues increased earthquake and volcanic activity - not just today's huge 7.7 magnitude quake 70 miles NW of Montego Bay (south of Cuba, so no tsunami affecting low-lying Florida), but then a 6.6 aftershock way over at the Cayman Islands and a warning of the early signs of a possible forthcoming eruption in Iceland (which would not just force airliner course changes over the North Atlantic, but has implications for further melting in the far Northern Hemisphere).

- This is only 2 weeks after big quakes in Puerto Rico; same fault line.

- China has tightened international travel and border crossings on its own initiative, and that's welcome, as are Air China and other airlines voluntarily curtailing 'most' flights.

- China death toll climbs to 132 deaths, as of press-time, and more U.S. business restrict or prohibit business travel to China (some started as early as last week as we noted).

- White House puts airlines on formal notice to prepare for suspension of flights to China and return (perhaps so that there are a couple of days to get as many Americans repatriated as possible).

- Realizing that flight crews always "overnight" before rotating back on US-bond flights, some sort of shuttle situation may well be needed to facilitate transfer, such as contemplated via Alaska, then (as noted last night) to Ontario Airport East of Los Angeles (for quarantine).

- Expansion of CDC testing to 20 airports can only be a temporary and emergency measure; hence the prospect of a subsequent limitation on flights from Asia (of course, a bigger challenge if wider flu here).

- Starbucks reports good earnings, but closes half its China stores for the duration of (at least this stage) outbreak.

- A clue of jitters: surgical-style masks are selling-out in U.S. drug store pharmacies, with total runs on stores in New York City and LA (so, if in a area of heavy population and you feel it necessary, consider N95 type respirators with easier breathing valves, although they're not all certified for "wet" use - though they otherwise may work well per a friend who used them during the recent California fire situation. Online may be the only way to obtain easily and avoid price gouging... just saying, even though hopefully most Americans will not have need for these).

- Apple rallied further on making their numbers; but also expressed the doubt mentioned earlier about resuming production schedules.

- JP Morgan will cut hundreds of consumer-division jobs.

- Finally, although most earnings reports were satisfactory, that's not the concern for markets as they absorb what is still a progressing and by-no-means contained situation.

- days ago I mentioned the "real" number is tens of thousands that are sick; reports tonight suggest over 60,000 "under observation."

- Note that while mainland markets remain closed; Hong Kong has just opened with a 3% drop.

Bottom-line: While S&P futures are up this evening; I'd be careful with a too-enthusiastic embrace of this particular rebound, even though it might stick around for a bit (measured in hours or a day or two). Risk of S&P revisiting area from which it rebounded are significant "down the line."

Conclusion is revised: Although I've leaned very clearly toward some sort of short-term correction (evolving sooner than early February due to initially higher S&P records). If anything, I've been conservatively optimistic through 2019 and reiterated old sayings like "don't fight the tape" and "don't fight the Fed." The only revision is variable extents of one or more pullbacks, as clearly relates to the WuFlu progression.

We remain circumspect; while market stresses were notably alleviated by making a "Phase One" deal with China (superficial it's not) while near-term Middle East chaos and now WuFlu throw wrenches into behavior of the market and more uncertainties to contend with ahead.

Enjoy the evening;

Gene

Gene Inger