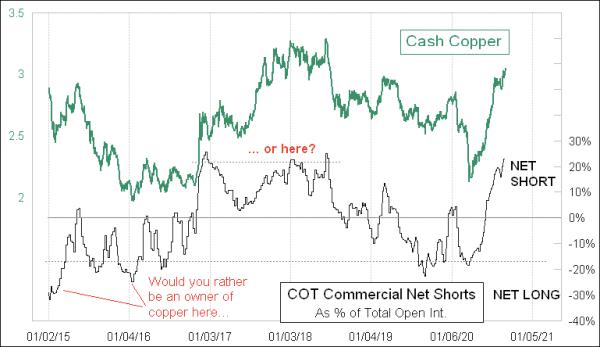

Many analysts believe that high copper prices are a bullish statement about the future of economic growth in general. I would amend that slightly to say that rising copper prices make that statement. But prices which are too high, especially without support, represent a problem - and a warning.

Copper prices fell during the COVID Crash in March 2020, along with everything else. And they have rebounded nicely since then, going well above the January 2020 high and giving a bullish vote for the economy. But as that price rebound has happened, the "commercial" traders reported in the weekly Commitment of Traders (COT) Report have been upping their collective net short position as a group. This suggests that the rise in copper prices does not have much further to go.

A "commercial" trader, under the CFTC's definition, is a person or entity which uses the subject commodity in their trade or business. So a big wheat farmer would be counted as a commercial trader, as would Archer Daniels Midland or Cargill, big buyers of grains. A lot of the commercial traders of commodities are producers, who use the futures market for what it was intended, as a way to sell their future production now and lock in the price for future delivery of what they produce. They often sell those contracts to speculators, which are counted in other categories.

So when the commercial traders as a group are showing a big net short position (total shorts minus total longs), that is a statement that they think the current price is a great one to lock in. If they thought that prices were going to rise further, they could hold off locking in their sales and hope for an even better price. That is typically what they do when prices are down. But when they are holding a big net short position, it is a statement by these "experts" that the price is pretty high and not very likely to go much higher.

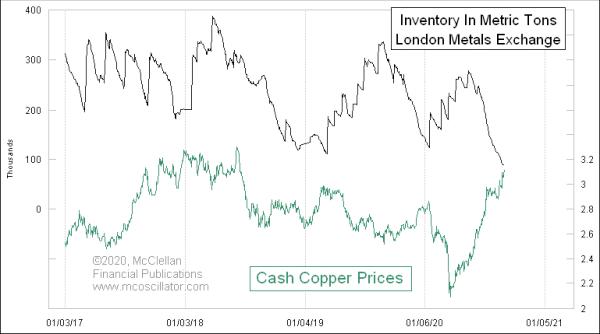

The producers can make this same statement in another way, as shown in the chart below. The London Metals Exchange (LME) operates warehouses around the world for storage and issuance of industrial metals. If a producer likes the current prices, it can sell its production in the spot market. If it thinks that current prices are too low, then it can just stockpile its production in an LME warehouse and hope for better days. So the size of LME warehouse stocks has a naturally inverse correlation to copper prices, most of the time.

The latest data show that LME stocks of copper are down to their lowest levels since 2005. The owners of those warehouse stocks are seeing the current prices of copper and concluding it is time to clear out the inventories and sell at these prices. They could hold onto that inventory and sell at hopefully higher future prices, if they thought that prices really would continue heading higher.

But that is not what they are doing. They are liquidating now, which is a powerful statement that the producers think this is a great price at which to sell. And that statement matches what we are seeing in the COT Report data.