The markets are rebounding strongly right now and trying to put the declines from February and March behind them. Most of the major averages moved back above their 50-day Moving Average on Friday (not the Dow though...). Smart ChartWatchers will be watching closely this week to see if this rally can continue to gather steam in the face of rising gas prices.

I'm on hiatus this time around. Be sure to check out what John, Arthur, Richard, and Carl have to say below. Catch you next time.

10-YEAR YIELDS SOAR OVER 4%... While today's surprisingly strong jobs report was good for stocks, it was very bad for bonds. Bond prices fell more than two full points. The 10-year T-note, which rises when prices fall, surged all the way to 4.14%. That certainly seems to confirm the idea that long-term rates are finally starting to move higher. There's good and bad news in that. It's good for economically-sensitive stocks that do well in a stronger economy. It's bad for rate-sensitive stocks that are hurt by rising rates. In time, rising rates can be a bad thing. Over the short-run, however, rising rates are viewed as confirmation that the economy is getting stronger and the job picture is finally improving. This week's sector rotations showed a more optimistic market. The top sectors were technology, materials, and industrials. The weakest were financials, energy, utilities, and consumer staples. That rotation is reversing the more cautious mood of the market during the first quarter when consumer staples and energy were the leaders and technology was the laggard.

The Philadelphia Gold Index, $XAU, is usually a better predictor of gold than gold is of $XAU. The top chart shows $XAU relative to gold or the "price relative". Notice that XAU performs best when the price relative rises ($XAU outperforming gold) and the price relative can be used to confirm or not-confirm strength in $XAU.

$XAU advanced from 73.41 to 112.75 (mid July to early Dec) and outperformed gold over this period. While $XAU went to a new reaction high at 113.41, the price relative formed a lower high for a bearish divergence (red arrow). This was a clear sign that $XAU was underperforming gold and led to the double top.

More recently, gold moved to a new high and $XAU failed to follow suit. $XAU managed to find support at 95 and break above 105, but the index remains well below its January high. $XAU is underperforming gold and this should be a concern to gold/XAU bulls.

Does the world really need another indicator?

Well, this is one we have been collecting data on for years, but we

just recently started charting it because we discovered it presents

a good picture of internal market strength or weakness.

Our Price Momentum

Model (PMM) is a simple but effective mechanical model that we apply

to all the stocks, indexes, and mutual funds we track. The PMM is

always on a buy or sell, and it generates new signals when: (1) price

moves 10% in the opposite direction of the signal extreme and (2) crosses

the 200-EMA. For example, if the model is on a buy signal, a sell

signal will be generated when the price index drops 10% from the highest

price recorded during the buy signal and crosses down through the 200-EMA.

(See http://www.decisionpoint.com/Glossary/PriceMomentumModel.html

to learn more about the model.)

Since we track every stock in the

Dow, Nasdaq 100, and S&P 500, we can calculate the percentage of the

stocks on PMM buy signals. The resulting indicator is similar to the

Bullish Percentage Index, which uses point and figure buy signals,

but our PMM indicator tends to be a bit less volatile because a PMM

signal change is harder to generate.

Currently, the indicator for the

Nasdaq 100 (NDX) shows that considerable damage was done to the

stocks in the index during the correction, as our indicator dropped

below 50%; however, it is bouncing back nicely.

When the Percent PMM

Buy index is above its 32-EMA, we generally consider the market environment

to be positive because it shows a persistence in stocks being

able to generate PMM buy signals. When it is below the 32-EMA, more

caution is warranted, although it is possible for a market index

to advance with only half its components participating (on PMM buy

signals) because most indexes are capitalization weighted.

I think this indicator is most useful

in evaluating the validity of major bottoms. If it can't move above

its 32-EMA, it says the rally is not broad and is being led by a few

large-cap stocks. Note how participation rose to over 90% within the

first months of the 2003 bull market advance. This was also the case

with the S&P 500, Dow, and the 112 Dow Jones US Sectors (which

moved to 99%!).

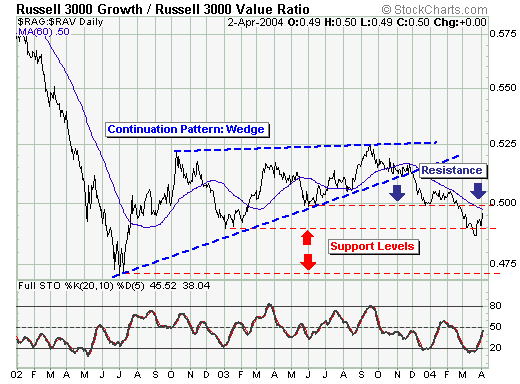

In terms of gauging the current substantial

rally, we should look at the relative performance of the "growth" and "value" components

thereof. In effect, if we are bullish, then we want to be long that

which is outperforming. This is fairly simple.

Thus, when we look at the Russell 300 "Growth

vs. Value" Ratio - we find the longer-term pattern is a confirmed "bearish

wedge" continuation pattern, which augurs for lower lows than that

seen during June/July 2002. However, a good short-term level in which

to become sellers or buyers happens to be the 60-day moving average.

In fact, Friday's sharp rally in the growth stocks has taken prices

right back to this now important resistance level. If prices break

above it - then one obviously wants to be long growth stocks over the

next several weeks. But, if resistance proves its merit...then growth

stocks will lag, and one could reasonably become short selected growth

shares. In any event - any growth rally will be short-lived given the

bearish wedge interpretation...which should translate into lower equity

prices overall.