We are super busy preparing the new release of our SharpCharts2 charting engine (see the "Site News" section below for more details). That means I haven't been paying much attention to the market recently. Fortunately, John, Carl, Richard, and Arthur have been, so let's get right to their commentary...

LOOKING FOR 62% RETRACEMENT AT 1250 ... With the S&P 500 having broken out of its recent trading range, and trading at the highest level in more than three years, it's time to revisit my earlier Elliott wave interpretation and came up with some possible upside price and time targets. Let's start with the monthly bars in Chart 1. As far as the technical indicators are concerned, the monthly MACD lines are still positive. The buy signal given in early 2003 is still intact. The monthly RSI line, however, is in overbought territory. That's of some concern, but doesn't prevent the market from moving higher. The question is how much higher. The horizontal lines measure the percentage retracements of the 2000-2002 bear market. The S&P has already moved above the 50% level. That makes the next upside target the 62% retracement level which sits near 1250 . There are some other technical measurements that confirm a move at least to that higher level.

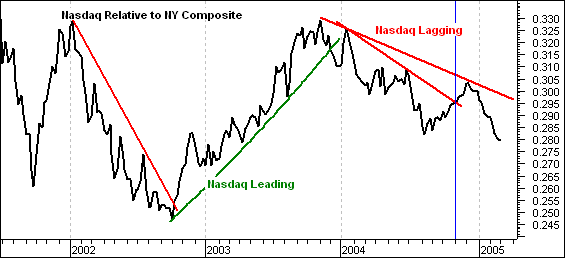

This chart shows the performance of the Nasdaq relative to the NYSE Composite. The market as a whole usually does better when the Nasdaq leads (green trendlines) and worse when the Nasdaq lags (red trendlines). Even though the NYSE Composite is performing well in the face of Nasdaq weakness, it would be doing a whole lot better with the Nasdaq leading – or at least participating.

Nasdaq outperformance peaked in Nov-03 and the price relative has declined steadily for over a year. There was a trendline breakout in November 2004 (blue line), but the price relative failed to move above the prior high and formed a lower high in December. The latest decline forged a new reaction low and it would take a move above .30 for the price relative to turn in favor of the Nasdaq again.

The recent problems within the Nasdaq are threefold. It is a one horse race and three of the top four industry groups remain under pressure. This has been the case since late January as the semiconductors took off, but Networking, Internet and Software continued lower or remained flat. Until one of these three joins the semiconductor group to make it at least a two horse race, the Nasdaq is doomed to underperformance.

Many ETFs (Exchange Traded Funds) pay dividends, but only one is devoted to dividend-paying stocks -- the Dow Jones Select Dividend Index Fund (DVY). As the name implies, this ETF is derived from the Dow Jones Select Dividend Index ($DJDVY), an index constructed and maintained by Dow Jones.

The Index is composed of about 100 stocks and is capitalization-weighted, which means the top one-third of the stocks in the index represent 60% of the weighting. A complete list is available on ishares.com. It is subject to change on a daily basis.

DVY has only been trading for about 14 months. Fortunately, Dow Jones has calculated historical data for the derivative index going back to 1992, so we have adjusted the index data so as to provide a theoretical price history for DVY. Now there is enough historical data to estimate how this fund will perform over the long-term.

The most impressive thing about the chart below is the relative strength line, which shows that DVY has out-performed the S&P 500 Index every year except 1998 and 1999. These were the years when investors abandoned dividends for the tech stock gold rush. At the 2000 top the S&P 500 was up nearly 300% versus only about 200% for DVY.

Since inception to the present DVY has advanced 500% versus 200% for the S&P 500, and the bear market didn't catch up to it until 2002 when DVY had a decline of 27% (versus a 50% bear market decline for the S&P 500). Since the 2002 low DVY has advanced about 75% versus 50% for the S&P 500.

When DVY first began trading, I thought it was just another ETF gimmick, but clearly this fund was a good idea. The chart demonstrates that value and growth can be synonymous. The current dividend is about 3%, which makes the stock overvalued if we compare it to the historical yield range of the Dow Industrials (3% to 6%). There is not enough dividend history to accurately estimate what undervalued is, but I'd guess it would be a yield of about 6%.

The recent rally to new yearly highs hasn't materialized in all the major indices. In fact, the Nasdaq Composite has lagged rather badly; thus it is either 'poised to catch up' or it will become the leaders once the cyclical bull market ends. We dont know when that will be; but our fulcrum point for adding to technology short positions will be upon the Composite breaking below its 60-week moving average at 1998...only 72 points below current levels.

That said, the larger bearish wedge pattern is also looming; a breakdown to 1900 would confirm this longer-term pattern. This isn't todays business as many of the traditional bearish signals seen at tops is only just beginning to materialize. However, it pays to have a game plan going forward...and technology short exposure is a good strategy as price declines materialize.