With the Dow getting ready to test its January lows, things are really getting busy here at StockCharts. Our market commentators have all the market angles covered below, so I wanted to take a couple of minutes and update you on our progress with SharpCharts2 - our soon-to-be-released replacement for our current charting tool.

Our Beta release program is winding down now and we have been making great progress incorporating everyone's feedback into the newest version. We are hoping to have the final Beta version out before the end of the month with the final version appearing shortly thereafter.

On of the key pieces of feedback that we received from our last Beta release was that we still weren't there with respect to chart colors. While it is true that colors aren't as important as, say, calculation accuracy, having attractive, easy-to-view charts is one of our hallmarks so, as promied, we've been putting more energy into improving the use of color in SharpCharts2. That work isn't finished yet, but I did want to get everyone a sneak peek at where we stand right now.

Here are some partial snapshots of our newest color schemes - Blue, Night, SeaGreen, Sand, Monochrome, and BlueGray. (You can see complete versions of these snapshots on this page.)

Hopefully, you'll notice the improvements we've made in terms of contrast, definition and clarity with these schemes versus similar schemes in the Beta 6 version. Again, this is just a taste of things to come. We'll have lots more color schemes and color options in the next Beta release. Stay tuned...

THE ECONOMIC NEWS ISN'T GOOD ... It's interesting to see the media put a positive spin on recent economic reports. It was reported this week that fourth GDP growth was lower than expected while prices were higher than expected. That was described as good for the economy. Earlier this morning, the government reported that March non-farm payroll numbers were only half what was expected. That was reported as good because it lessened the chances for higher interest rates. A report of lower consumer confidence was viewed as a non-event. The ISM report showed a weakening in manufacturing activity coinciding with surging raw material prices. That apparently is why companies haven't been hiring. It was reported that although the ISM number fell to 55.2, it was still above 50 which is good. My question is how can a slowing GDP number, slowing manufacturing activity, lower consumer confidence, higher raw material prices, and fewer jobs be good for the economy. The market is telling the truer story. Sector rotations during the first quarter paint a bearish picture for the market. After suffering a bad first quarter, the market fell sharply again today and threatens to get even worse. A number of stock indexes are testing chart support at their 2005 lows. I suspect they'll be broken sooner or later. Since the market is also a leading indicator for the economy, economists might do well to pay more attention to the message the market is sending. Unfortunately, it's not an optimistic one.

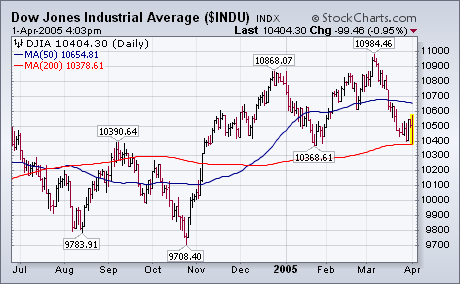

DOW THREATENING JANUARY LOW... The daily Dow chart shows the market at a critical juncture. The Dow fell 99 points today and is threatening its January low, its 200-day moving average, and its September peak at 10390. I suspect all will be broken. There's always the possibility of an April bounce. But seasonal factors then turn negative until the autumn. My best guess at this point is that Dow is headed toward its fourth quarter low near 9700. I would continue view any short-term bounces as selling opportunities. Two of the best places to be right now are energy and cash. If you haven't already done so, take a look at some bear market mutual funds. They'll allow you to make money in a falling market.

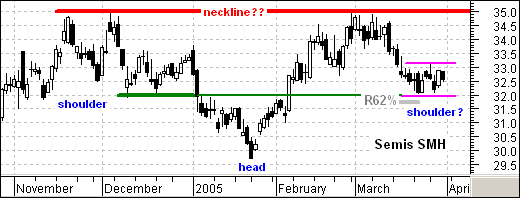

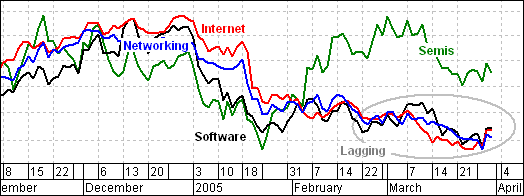

It remains a one horse race among the key Nasdaq industry groups. The Networking iShares (IGN), Software HOLDRS (SWH) and Internet HOLDRS (HHH) are weak and trading near their lows for the year (gray oval). However, the Semiconductor HOLDRS (SMH) are holding up the best and still well above their January low. Strength in semiconductors is certainly positive for the tech sector, but even semis need a little help from their friends.

SMH shows potential, but remains short of a minor or major resistance breakout. The big pattern at work is an inverse head-and-shoulders. These are potentially bullish patterns that require confirmation with a neckline breakout, preferably on high volume. Also notice that SMH is consolidating at the 62% retracement mark (magenta trendlines). A consolidation breakout would be the early bull signal and further strength above 35 would confirm the inverse head-and-shoulders. Moves like these would no doubt help the tech sector, the Nasdaq and the S&P 500.

The Rydex Asset Ratio measures the amount of bullish and bearish sentiment by tracking and comparing the total assets in Rydex bull and bear funds. Decision Point also calculates the Rydex Cash Flow Ratio, an indicator we developed that accounts for the actual cash flowing into and out of the funds by canceling the effect of changing share prices on total assets.

On the chart below we can see that bulls were not nearly committed at the March price top as they were at the December 2004 top. I have drawn a line across the corresponding Ratio tops to illustrate the negative divergence.

The two Ratio lows in January and March represent short-term oversold points, but the real benchmark is set by the Ratio lows in August 2003 and August 2004. When this level is reached again, it will probably mark an intermediate-term price low.

The Ratio has maintained a pretty steady range for the last two years, but it could shift higher or lower based upon the longer-term trend of prices.