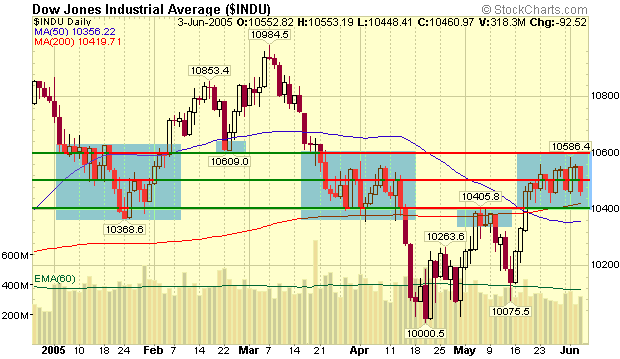

This week saw the markets move "violently sideways" as large up-days were immediately followed by similarly large down-days. Essentially, the Dow is continuing to lurch around inside of its 10,400 to 10,600 trading range. Check out how much time the Dow has spent in or around that range since the beginning of the year:

The good news? The rising 200-day Moving Average may push the Down up above 10,600 soon.

The bad news? Recent declining volume argues against any upside breakouts soon...

Now let's see what our other commentators think...

...

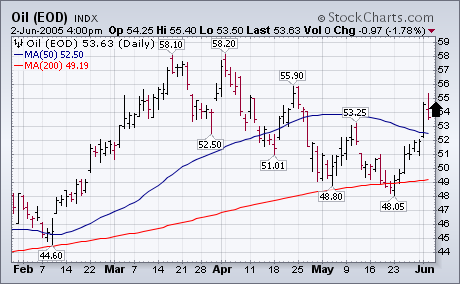

A lot of recent optimism on the stock market and the economy has been predicated on the view that the historic rise in oil prices has probably ended. A lot of economists have also declared the major bull market in commodities over. Both of those predictions may prove to have been premature. Over the last two weeks, the price of crude oil has bounce off its 200-day moving average and then risen to the highest level in more than a month. After a pullback yesterday, it's trading back over $54 today. The chart below reflects the recent improvement in the price of crude and suggests a possible retest of its early April high. That explains the recent move back into energy stocks. It may also explain why the recent market rally is running into some profit-taking. Crude isn't the only commodity that's turned up recently. The CRB Index of commodities is rising again after bouncing off major support levels.

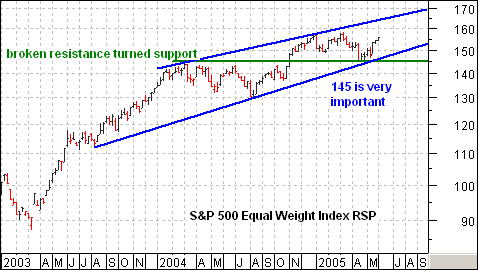

As its name implies, the Rydex Equal Weight S&P 500 Index (RSP) treats all component equal, regardless of market capitalization. This means that ExxonMobile (XOM). with market cap of $369 billion, counts the same as Teco Energy TE), which has a market cap of just $3.64 billion. This makes the index a good representation of the average Joe (Joe Stock that is).

RSP remains in a long-term uptrend and has yet to break down. The going is getting tougher, but momentum is still up overall on the weekly chart. First, the index broke resistance at 145 with a surge in Nov-04. This resistance level hounded the index most of 2004. Second, resistance turned into support with a successful test in Apr-05. Third, the trendline extending up from Aug-03 also confirmed this support level and the index remains near its all time highs.

Even though the index has not made much head way over the past year, there is a clear upward bias on chart. Support at 145 holds the key. As long as this level holds, pundits can expect a trading range at worst and a move towards the upper trendline (170) at best. A move below 145 would turn the big trend down and be bearish for the broader market.

Decision Point tracks actual cash flowing into and out of Rydex mutual funds, and, while cash flow normally runs parallel to price, divergences can often appear ahead of price reversals. For example, let's look at Rydex Energy and Rydex Energy Service Funds.

During the last four weeks of the price correction that began at the March top you will notice how cash flow went relatively flat, indicating that the bulls were holding their ground and that accumulation was taking place. However, since the two-week rally that began at the May price low, cash flow has been rather tepid, and was even flat during the first week of the rally.

It is probable that energy stocks have completed a medium-term correction and are poised to move higher, but the lack of sponsorship and overhead resistance warn that we could see a partial retracement of recent gains, particularly in the Energy Service sector.

Cash flow divergences provide valuable clues that can help us prepare for price action others are not expecting, but they don't always result in the kind of price move they imply. Always wait for prices to make the expected break before acting.

My observation is that these cash flow divergences only have short-term implications. Also, it is important to remember that the Rydex sector funds only account for a small slice of the total market in a given sector, and this small picture may not be representative of the big picture.

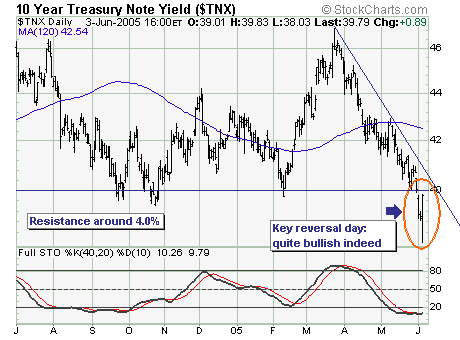

Rarely do they ring a 'bell' at the bottom, but Friday’s reversal higher in bond yields argues strongly for a sustained move higher in interest rates. Quite simply, Friday's employment report was clearly on the 'weak side'; with the 10-year note yield trading lower and then reversing and trading sharply higher. This 'key reversal' to the upside is likely a 'watershed event' in which bond yields will march higher over the short and intermediate-term time horizons. This pattern is one that we nearly trade with 'blind faith upon', and we did so on Friday by becoming short.

If one chooses to trade this pattern; one can short the 10-yr. or 30-yr. futures contract – or – short the Lehman 20-yr+ bond fund (TLT), but shares appear difficult to borrow at some brokerages – or – buy TLT put options. We don’t recommend options for those who haven’t had experience with them; and those that do must understand the risks.