The market battled back impressively over the past week and a half and is re-testing the 10,600 resistance level that gave it so much trouble in mid-June (and May and late March).

With the CMF poised to move into positive territory, the PPO already positive, and the 50-day MA about to move above the 200-day MA, the technical signals look pretty good right now, but here's where Technical Analysis becomes more of an art than a science. Notice that on Friday, the Dow failed to climb above the high that it set on Thursday. Also note that Friday's volume was slightly below average. Experienced chart watchers know that those can be early warning signs that the current rally is fading, especially if those signs appear near an important resistance level. Because of that, my gut says that its time for a pull-back. Watch the markets closely on Monday to see if my gut or the technical indicators are correct!

A few weeks back I wrote about the close linkage between the Dow Transports and Industrials. At the time, both were threatening their spring lows. Now both are testing their June highs (see first chart). A Dow close through that barrier (combined with a similar upside breakout in the Transports) would constitute an intermediate term Dow Theory buy signal. Two of the biggest contributors to the Dow's recent strength are General Motors and IBM. The second chart shows GM trading at a new five-month high after climbing above its 200-day moving average earlier in the week. Although IBM is still well below its 200-day line, it's climbed to a new three-month high this week (see the last chart). It looks like money is starting to nibble at some previously-neglected blue chips.

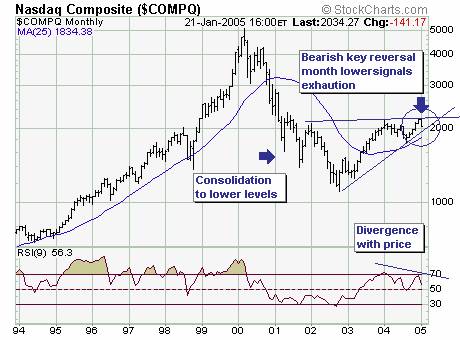

January and 2005 have not been good for the bulls. After a strong finish in 2004, stocks were hit with strong selling pressure to begin the year and have yet to recover. A look into November and December reveals early weakness in two key groups. More importantly, traders can turn to these two key groups for signs of a bullish revival.

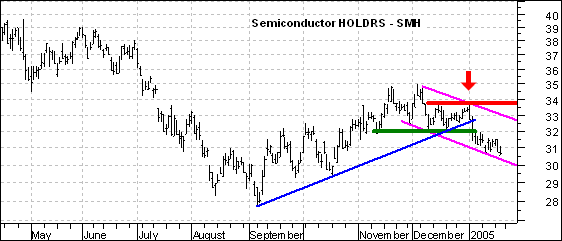

So who done it? Look no further than Retail and Semiconductors. The retail group makes up a big part of the Consumer Discretionary sector and influences the S&P 500. In addition, estimates are that retail spending drives 2/3 of GDP and exerts a large influence on the economy. Semiconductors represent a key tech group that influences the Nasdaq, which in turn affects the S&P 500.

Both stocks were keeping pace until mid November and then started underperforming in December. While the S&P 500 and Nasdaq finished 2004 near their highs for the year, the Retail HOLDRS (RTH) and the Semiconductor HOLDRS (SMH) failed to exceed their November highs (red arrows) and began underperforming.

SMH went on to break the blue trendline and key support at 32 for a bearish signal, while RTH formed a triangle over the last two months. Both need to move above their 3-January highs to put the bulls back in charge. The pattern for SMH looks like a falling price channel (magenta trendlines), but the channel is still falling and it would take a move above key resistance at 33.77 to forge a significant breakout. For RTH, a move above 100.25 would signal a continuation higher. As long as these early January highs hold for both, the broader market is likely to remain under pressure.

The Equity and OEX Put/Call Ratios generally signal overbought and oversold conditions that help identify price tops and bottoms; however, sometimes the OEX Put/Call Ratio will invert relative to the Equity Put/Call Ratio. At these times the inversion signals the opposite of what we would normally expect.

Here's how I think this works. The Equity P/C Ratio represents the activity of speculators (the little guys) who become more and more committed to price direction until it reverses on them, therefore the Equity P/C Ratio becomes oversold at price bottoms and overbought at price tops.

The OEX P/C Ratio reflects hedging activity by big money. These guys tend to lighten up as the price trend becomes more extreme, preparing for the inevitable reversal, so the OEX P/C Ratio can become overbought at bottoms and oversold at tops -- the opposite of what happens to the Equity P/C Ratio.

This is not always the case, but I have put red dotted lines on the chart to point out where these inversions have signaled price bottoms. Note that there is one very prominent inversion occurring now. Because the Equity P/C Ratio is oversold and prices have been declining, I think there is an excellent chance that the OEX P/C inversion is telling us that a price low is imminent.

My observation is that these signals can have short-term or intermediate-term implications, but there is no way to tell in advance.

The January decline to date is gaining in importance; if prices remain at current to lower levels through the next six trading sessions – then a bearish 'key reversal month' will form. This would signal 'exhaustion' of the uptrend, with any and all rallies considered selling opportunities. The last such monthly formation signal was January-2002...with the decline of nearly 50% materializing from January's high at 2098 to October's low at 1108. Now, we don't necessarily believe the decline is going to be this dramatic at this time, but we simply want to illustrate that a substantial decline is a higher probability event...even more so if the 25-week moving average currently at 1834 level is violated.