Forces of nature have conspired to prevent the stock market from rising significantly since our last visit, however the markets have showed suprising strength considering the impact on the US economy that these storms are having. The storms are also on the minds of our regular columnists. John Murphy reviews their impact on oil prices, Richard Rhodes looks at the debt implications, Carl Swenlin looks at market beadth indicators, and Arthur Hill sees new life in the $VIX. Let's get to it...

Today's selloff in oil of more than two dollars may be completing a right shoulder in a short-term head and shoulders top in the key commodity. The September bounce has fallen well short of the late-August peak (the head) and is about equal to the early August peak (left shoulder). It's now challenging its 50-day average and may be headed for a test of the neckline near 62.50. A close beneath that support line would turn the short-term trend down. That would weaken energy stocks even further. I'm not suggesting that the long-term bull market in energy is over. I am suggesting that it's come too far and is need of some correcting. I also believe that the price spikes from the two recent hurricanes have probably been overdone. What better time to take some energy money off the table when TV stations are talking about nothing else. One TV station showed a chart of the XLE yesterday and said it was a good thing to buy when oil prices are rising. That's the "kiss of death" in any rally.

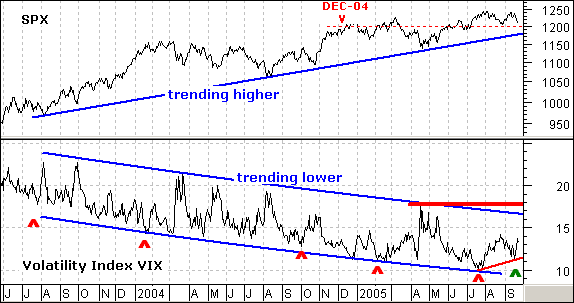

Fear is creeping into the market as the S&P 500 Volatility Index ($VIX) forms a higher low. And you thought the VIX was dead! Well, actually, it is pretty dead as volatility slows to a crawl. The VIX has been spot-on when it comes to calling market risk (volatility). The S&P 500 recorded a four year high in early August and the VIX recorded a 10 year low. The S&P 500 has gone nowhere since December 2004 and the VIX declined from 15% to 10%. This simply confirms the dullness of the current market environment.

As the red carets show, it is lower low after lower low for the last few years. The VIX remains within a falling price channel and clear downtrend. However, the indicator formed a higher low in September (green caret) and is poised to break its August high. A mini-breakout would show an increase in volatility, which is also known as risk and fear. With increased fear comes more uncertainty and uncertainty breeds contempt. This will result in flat stock prices at best and lower stock prices at worst. Should the VIX break above upper channel trendline and April high, a new uptrend in volatility

(risk) will begin and this will translate into lower stock prices.

Since the beginning of July, 52-week new highs have been contracting with each new NYSE Composite price high, demonstrating that fewer and fewer stocks are participating in the rally. Contracting new highs by themselves are not always problematic, and can merely be a sign of an approaching correction in an ongoing bull market; however, when they are accompanied by expanding 52-week new lows, a darker picture begins to emerge.

You will note that spikes in the number of new lows usually occur at the end of corrections, giving notice that the correction is near an end. Unfortunately, the recent spike in new lows has occurred just as the NYSE Composite Index has pulled back from an all-time high, and this is an indication that, not only is upside participation fading, but the tide may be shifting to the downside as well.

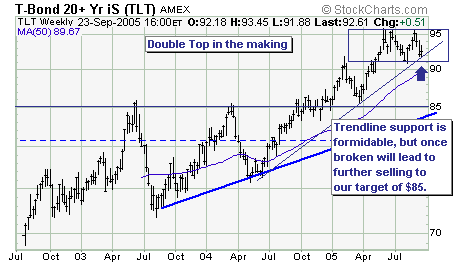

With both Hurricane Katrina and Rita now in the history books, local, state and federal government to issue more debt will need to issue debt for reconstruction efforts and so forth. This bearish fundamental coupled with the yield curve not inverting any longer suggest the risk-reward of short positions in the long-end bond is quite good.

From a technical perspective, we want to keep it simple. We note that TLT as it is forming a bearish "double top" and further resides right upon its bull market trendline. We expect lower prices to be confirmed on a breakdown through $91.25 level, with a swift and material decline towards our target at $86.

In our letter we are currently short, and will look to add to the trade in the weeks ahead.

2005 Performance:

ETF Portfolio - +8.6%

Paid-to-Play Portfolio - +15.3%