The markets are getting very interesting these days! Last week saw some big declines that were mostly erased by Friday's rally.

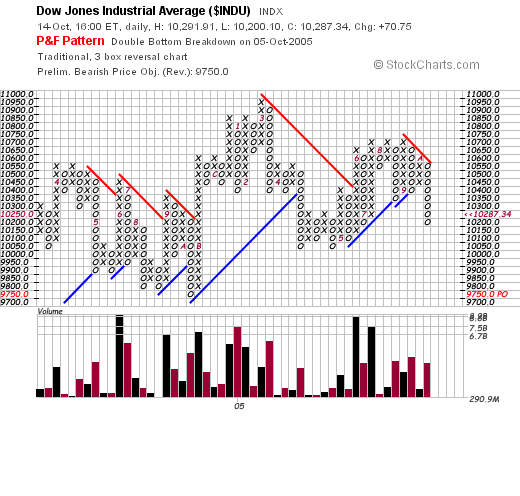

If you're looking for bearish signals, look no further than our Dow Jones Industrials Index P&F chart:

I draw your attention to the volume bars at the bottom of the chart. Note that the last three red volume bars are much higher than the last three black volume bars. That means that the market has been more active during the last three significant downtrends than it has during the intervening uptrends - a sure sign of growing market pessimism. In addition, the simple P&F price objective - based on the double-bottom breakdown signal from last week - is now at 9750. While I doubt that prices will get that low anytime soon, there's a good chance the major support level at 10,000 will be retested soon.

Our other authors are decidely bearish also. John looks at Bear funds, Carl calls this market "dangerous", Arthur thinks the Nasdaq's RSI is oversold, and Richard calls the S&P 500 "weak". Read on for all the details.

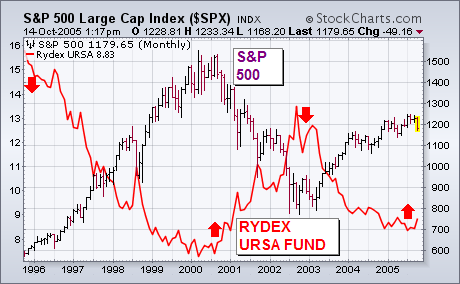

My Wednesday message on bear funds wrote that they should be used as trading vehicles and not as a long-term investment. One of our readers asked why. That's because the market has a history of rising more often that it falls. To hold a bear fund in a rising market ensures unnecessary market losses. Since the start of 2003, for example, the bear fund would have lost 28% while the S&P 500 gained 34%. In other words, a bear fund would have been a bad holding over the last three years. The picture is even worse the further back we look. The chart below compares the S&P 500 monthly bars to the Rydex Ursa bear fund (red line) for the last ten years. The bear fund is designed to move in the opposite direction of the S&P 500. The bear fund fell from 1995 to 2000 as the market rose. After rallying from 2000 to 2002, it fell again from 2002 to 2005. That means that the bear fund fell for seven out of the last ten years and three out of the last five. It would have done a little better than the S&P 500 since 2000. But it would have lost a lot in the three years since 2002 and a lot more over the entire ten-year period. That's why it shouldn't be used as a long-term investment. A bear fund can and should be used, however, when the market looks like it may be turning down -- as it is now. In my view, that makes bear funds trading vehicles and not long-term investments.

This week 14-day RSI for the Nasdaq became oversold (below 30) for the first time since April (gray oval). Even though securities can become oversold and remain oversold, the odds of a bounce increase with oversold conditions. The question is not whether there will be a bounce or not, but rather how far will the bounce extend and when will the bounce end.

Previous extremes in RSI occurred in pairs with an intermittent move to around 50. Notice that there were two oversold dips in March and April (green circles). The last overbought reading also featured two moves before the Nasdaq peaked in July (blue circles). The first overbought (oversold) reading serves as a warning to prepare for a pullback (bounce).

RSI usually finds resistance at 50 on an oversold bounce and support around 50 on an overbought pullback (black boxes). It is these moves to around 50 that provide a second chance to partake in the ongoing trend. To partake in this downtrend, I would wait for a bounce back to 50 in RSI and possibly 2100 in the Nasdaq, which marks broken support.

The Price Momentum Oscillator (PMO) is an expression of internal strength for a given price index. In the chart above we summarize three important PMO characteristics for the individual stocks in the S&P 500 -- the percentage of PMOs rising (very short-term), the percentage of PMOs on crossover buy signals (short-term), and the percentage of PMOs above the zero line (medium-term). The chart tells us that the S&P 500 is technically oversold in all three time frames. (To read more about the PMO click here).

We normally think of oversold conditions as signalling the next buying opportunity, and as you can see, oversold conditions such as this normally lead to some kind of rally once a price low is in place. Normally, but not always. During a bear market, oversold conditions can result in even more selling.

I don't know if that will happen this time -- I can't say with certainty that a bear market has begun -- however, there are good reasons for extra caution. Most obvious on the chart is the breakdown from the ascending wedge pattern, which is bearish. And spanning a much longer time frame is the declining tops pattern on the PMO, which diverges from the rising tops of the bull market.

Looking beyond the chart, we know that bull markets do not go on forever, and this one is three years old. Based upon my cycle work, the 4-Year cycle is due to crest, leading to a bear market decline that should last until about this time next year. Also, we have sell signals on all but two the 17 major market and sector indexes tracked by our primary timing model. The exceptions are Energy and Utilities, but they are under pressure as well.

Bottom Line: A bounce is likely, but I do not believe it will lead to new price highs. Rather, it will work off the oversold condition and set things up for a continuation of the decline. Worst case is that there will be no bounce, just more selling, and the market will become even more oversold. In either case, it is a dangerous time to be making bullish assumptions.

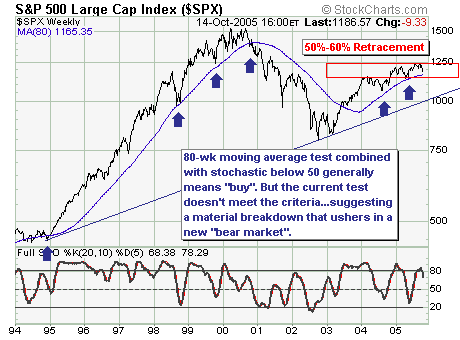

Today, the simple technical picture is breaking down in our opinion. If we look back to 1994, we find the 80-week moving average has been an excellent swing trading tool as it holds the data as near perfect as can be expected. Our concern focuses upon the current decline from the normal 50%-60% retracement level back to the 80-week moving average. Normally, we would be buyers of its test for a move to higher highs, but given the 20-week stochastic isn't below 50 - thereby confirming at least modest technical neutrality - this indicates that prices have still lower to work. Therefore, a breakdown below the 80-week moving average would signal the countertrend rally off the 2002 lows is complete, and an overweight and aggressive short campaign to "short the rallies" should be undertaken. We don't make these claims likely, but the probability suggests further S&P 500 weakness ahead.

2005 Performance

ETF Portfolio: +9.1%

"Paid-to-Play" Portfolio: +19.2%