While last week was a really good week for the markets - Dow up 3%, Nasdaq up over 5% - it was a really lousy week for StockCharts.com. As most of you know, the site had problems creating charts on Thursday and again on Friday and then we were also down much of the day on Sunday.

Soon after the market opened on Thursday, we suddenly stopped getting data from both of our data feed servers. It was an extremely unusual and unexpected situation. Why would two separate computers suddenly stop communicating at the same time? Another frustrating part of the puzzle was that as soon as we took the web site offline, the problem went away. It would only happen when real people were using the website to create real charts while the real market was open.

Most of Thursday was spent trying the "standard" approaches to finding and fixing such a problem. Unfortunately, this problem was resistant to those techniques and on Friday, when the market opened again, the problem resurfaced. Friday was spent trying more and more "drastic" measures and eventually, around 3PM Eastern, one of those techniques worked. The site was up for the final hour of trading on Friday and, knock on wood, it appears to be back to its old normal self again as I write this on Monday morning.

"No good deed goes unpunished" as the saying goes and this was no exception. Just as we started to recover from our marathon troubleshooting sessions, something else unusual happened. On Sunday morning, for the first time in our six and a half year history, we had a long power outage in our data center. Now, you are probably familiar with the heavy UPS battery devices that you can buy to protect your computer in case of a power failure. We have something similar here - except that our UPS can keep our 40+ servers running for about 3 hours (yes, it is REALLY heavy too!). Unfortunately, this power outage lasted much longer than that and it knocked us off the air. Once the power came back on, we were able to get the site up and running within an hour, but it wasn't until Monday morning that everything was fully functional again.

Again, we really do understand how frustrating and difficult it is for our users when our site isn't working correctly. We have worked very hard to get things back up quickly while keeping people as informed as possible about this situations. Going forward, we will be conducting a "post-mortem" review of our procedures to find ways to minimize the chances of these kind of problems occurring again in the future. We will be looking into things such as secondary data vendors, large scale power generators, scheduled maintenance periods and more. In addition, we have already added one week of free service to all active members' accounts as our way of saying "Thanks for hanging in there with us." Finally, we sincerely apologize for whatever inconvenience these outages have caused.

Oh, and all of the above "stuff" also explains why this newsletter is coming out later than usual. And we apologize for that also.

OK, so back to the markets and the market commentary...

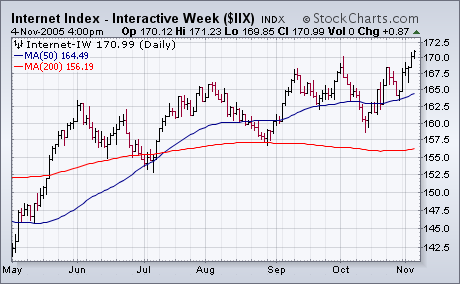

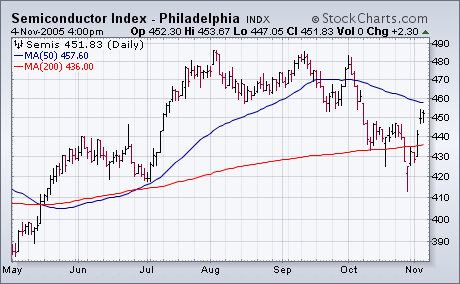

The weekly bars in Chart 1 show the improvement in the S&P 500 this past week. Not only did it close back over its (red) 40-week average, but it closed above its (blue) 10-week average as well. Even more impressive was the heavy upside volume. That strong action moved the market out of its danger zone. Having survived the dangerous month of October, the market has now entered a seasonally strong period between now and yearend. The weekly histogram bars are still negative (below the zero line). However, they have risen for two consecutive weeks (meaning the MACD lines are starting to converge). While that doesn't constitute a "major" buy signal, it does suggest the covering of short positions (or lightening up on bear funds). With oil still on the defensive, fourth quarter market leadership is coming from financials, retailers, the transports, and technology. Most of the recent technology leadership came from Internet stocks which closed at a new recovery high (Chart 2), while semiconductors have been one of the market's weakest groups. This week, however, the SOX Index climbed back over its 200-day moving average (Chart 3). It's a good sign when even the weakest groups start to show some improvement.

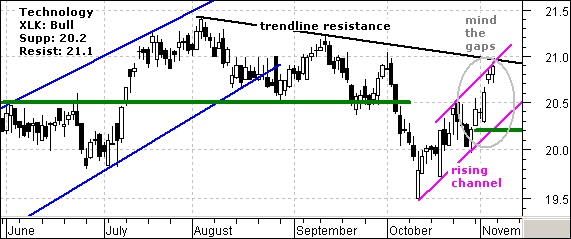

The Information Technology SPDR (XLK) broke support in early October, bottomed in mid October and surged over the last few weeks. This surge featured two gaps last week and these hold the key to recent strength. The stock gapped up on Monday and again on Thursday (gray oval). Gaps show power and both of these gaps should be considered bullish unless they are filled.

The stock is nearing resistance from the August trendline and early October high. A move above the early October high would break the August trendline and forge a higher high. This would be enough to turn the medium-term trend bullish and expect new highs over the coming months. Yes, the fabled yearend rally would be upon us.

The current advance looks like a sharp rising price channel and "rising" is the key word. The lower trendline sets the bullish tone and support from this trendline coincides with Monday’s gap. Should the stock fail to break resistance, watch for a move below 20.6 to fill the second gap and signal trouble. Further weakness below the first gap (20.2) would also break the rising channel trendline and reverse the current uptrend. Such a move would target further weakness below the October low.

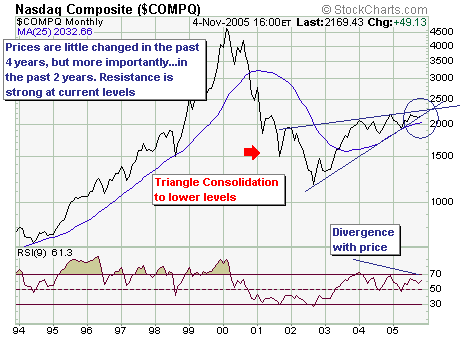

On a longer-term monthly basis, the Nasdaq Composite is very clearly forming a rather bearish "wedge" pattern. Resistance between 2080 and 2220 is quite strong, and rallies back into this zone are becoming weaker and weaker. Ultimately – and we think rather soon, this pattern will lead to lower prices…and perhaps sharply lower prices. Certainly the probability will have increased, and will initially be confirmed once prices decline through wedge support at 2098, and then through of the 25-month moving average at 2032. Then, and only then can we say with any confidence a ravaging bear market is upon us…and it is far closer than one would think.