The troops are mustered. The swords are out. The orders have been posted. The pieces are in place. The die has been cast. (The metaphors are getting lame.  ) However you want to say it, the battle line for the Bulls and the Bears has been drawn. Can you spot it on this Dow chart?

) However you want to say it, the battle line for the Bulls and the Bears has been drawn. Can you spot it on this Dow chart?

13,200.

Going back to early May. That is the major support level for the Dow. It was sorely tested last week and was broken on Friday. Will it bounce back this coming week? With the MACD clearly negative and the Chaikin Money Flow crossing below zero right now, things don't look promising. At the risk of abusing yet another metaphor, in the coming days astute ChartWatchers should be treated to all out war between the Bulls and the Bears.

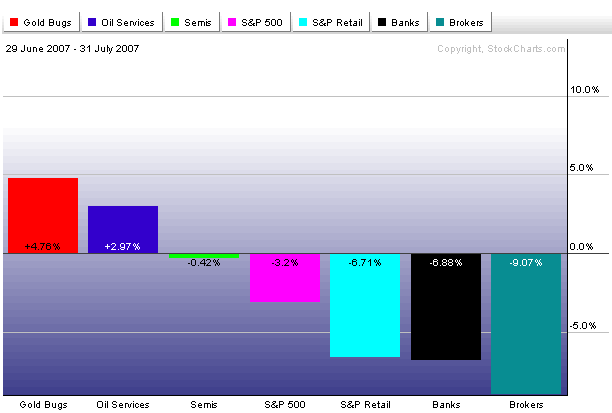

The chart above shows "John's Latest Performance Chart" that reflects the market's stronger and weaker groups during the hightly volatile month of July. All are plotted around the S&P 500 which lost 3.2% during July. [The S&P can also be plotted as a zero line]. The bars to the left of the S&P did better than the general market. The two top gainers were gold and oil service stocks. The AMEX Gold Bugs Index ($HUI) gained 4.5% in the face of a severe market downturn. Oil Service stocks held up well on the back of rising oil prices (although the've started to slip during the first week of August). Semiconductors lost a small -.42%, but held up better than the S&P. The bars to the right show where most of the weakness has been. Brokers, banks, and retailers were among July's weakest groups. [Homebuilders and REITs were even weaker]. I did a story on Thursday about how relative weakness in retailers was tied to housing problems. The beauty of the performance bars is that they can tell us in one picture where investors might be looking to invest (like gold) and what to avoid (financials, retailers, and anything tied to housing). That juxtaposition of the performance bars also carries a negative warning for the stock market.

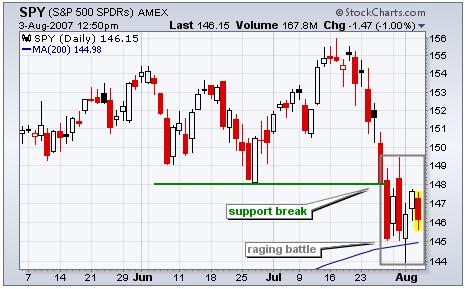

The S&P 500 ETF (SPY) firmed this week and found some support. The ETF hit support from the 40-week moving average and broken resistance. The 40-week moving average is equivalent to the 200-day moving average and this level is important to the long-term trend. Resistance stems from the February high and SPY broke this level in April. Securities often return to the their breakouts and this marks an important test as well.

A bull-bear battle raged this week as SPY shot up to 149.5 on Tuesday and fell back to 144 intraday on Wednesday. That is about a 3.5% swing high-low swing in two days. The bulls are trying to hold support and the ETF has basically consolidated this week. The boundaries of this consolidation hold the key to the next move. A break above 149.5 would be positive and revive the bulls. Conversely, a break below 144 would signal a continuation lower and decisively break support.

A month ago I wrote an article stating that I thought that the 20-Week Cycle was cresting and that we should expect a decline into the cycle trough that would probably break down through the support provided by the bottom of the trading channel, setting up a bear trap. So far so good. As you can see on the chart below, the S&P 500 has broken down through the horizontal channel support, as well as an important rising trend line. The trend line break is not decisive (at least 3%), but this break down has gone farther than I had expected.

In the process of the recent decline the market has become very oversold, as demonstrated by the next two charts. The first is our OBV suite, which includes the CVI (Climactic Volume Indicator), STVO (ST Volume Oscillator), and VTO (Volume Trend Oscillator). All three of these indicators have hit very oversold levels, levels from which rallies normally emerge.

The same is true for the ITBM (IT Breadth Momentum) and ITVM (IT Volume Momentum) Oscillators, which reflect a substantial internal correction, and tell us that we should start looking for a bottom.

As usual I would caution against trying to pick a bottom. For one thing, our primary timing model switched to neutral on July 31, which I think is a good place to be while the market is still displaying weakness. Another thing to consider is that the bears could be right about new bear market just beginning. If this is the case, oversold readings are extremely dangerous and can actually signal the likelihood of even more severe declines. To reiterate, oversold in a bull market means a bottom is near, but in a bear market it means "look out below!"

Bottom Line: The market has become very oversold, and I expect to see a bottom forming over the next several weeks. I am still overall optimistic because of the 20-Week Cycle alignment with the current decline, and because we are still in the beginning of the 4-Year Cycle; however, caution is recommended until our timing model switches back to a buy signal.

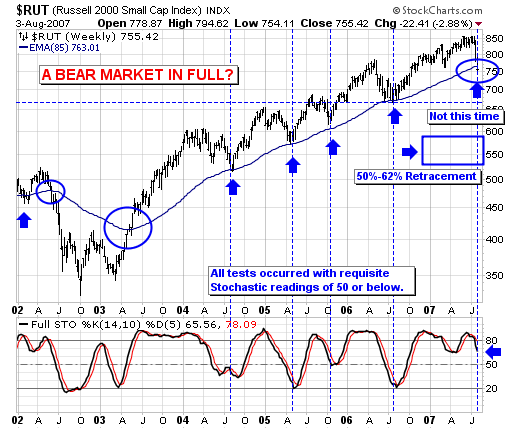

Last week was a treacherous week indeed, with stock prices falling universally. That said, one of the "weakest indices" was related to the US small cap arena, and specifically to the Russell 2000 Index ($RUT). In the past, RUT led the market higher, but that changed last year as a bottom was forged against the S&P 500; however, we now see sharp absolute weakness has caused RUT to breakdown below its 85-week exponential moving average. This moving average during the bull market from 2002 has provided an excellent "buying point" â especially given when the 14-week stochastic has fallen below 50. Unfortunately, that isn't the case at present, as Friday's weakness caused prices to break through this important moving average, which to us suggests a "bear market" in small caps is now confirmed, with further downside price action likely in the months ahead.

As a result, a reasonable "first target" is 670, which is another -10% lower from current levels. But in the fullness of time, we would expect the decline to find major support at the 50%-62% retracement of the entire bull market, which on a worst case basis would be -30% from current levels. Moreover, if the decline looks anything like the April-to-October 2002 decline, then we could very well obtain our "worst case scenario" by the end of this year.

) However you want to say it, the battle line for the Bulls and the Bears has been drawn. Can you spot it on this Dow chart?

) However you want to say it, the battle line for the Bulls and the Bears has been drawn. Can you spot it on this Dow chart?