Market Recap for Monday, October 2, 2017

It was another record day on Wall Street. The Dow Jones, S&P 500, NASDAQ and Russell 2000 all closed at fresh all-time highs. Wide participation is a hallmark of a bull market rally and, make no mistake, there's been wide participation on this rally. The only disappointment on Monday was the NASDAQ 100's ($NDX) inability to join the party. Key large cap technology names did not participate and that held back the NDX. Materials (XLB, +1.09%), healthcare (XLV, +1.02%) and financials (XLF, +0.85%) led the rally and that leaderboard helps to explain the lack of participation of the NDX as it has no components in the materials sector and only a few financials - all in financial administration.

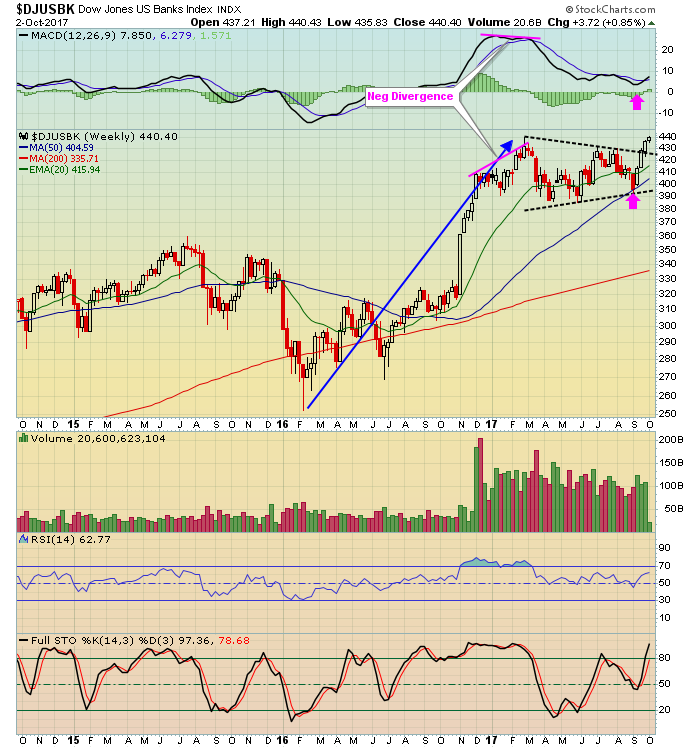

While there wasn't a huge surge in the 10 year treasury yield ($TNX) yesterday, the move to its highest close in nearly 3 months to 2.34% was enough to send banks ($DJUSBK) to their highest level in nearly a decade. Check out this bullish chart:

Banks rose approximately 75% in one year from the low in early 2016 to the high in early 2017. But if you look at the chart, that final high in February was accompanied by a negative divergence. This group needed a rest and it did exactly that over the next 6-7 months, consolidating in a bullish symmetrical triangle (black dotted lines). During that period of consolidation, note that the weekly MACD nearly reset at centerline support and price action eventually tested its rising 50 week SMA. That's excellent technical behavior and now banks appear to have resumed that prior uptrend. Higher treasury yields result in rapidly increasing EPS for banks and the market now is pricing in those higher bank profits with the technical price action.

Banks rose approximately 75% in one year from the low in early 2016 to the high in early 2017. But if you look at the chart, that final high in February was accompanied by a negative divergence. This group needed a rest and it did exactly that over the next 6-7 months, consolidating in a bullish symmetrical triangle (black dotted lines). During that period of consolidation, note that the weekly MACD nearly reset at centerline support and price action eventually tested its rising 50 week SMA. That's excellent technical behavior and now banks appear to have resumed that prior uptrend. Higher treasury yields result in rapidly increasing EPS for banks and the market now is pricing in those higher bank profits with the technical price action.

Pre-Market Action

Global markets are mostly higher. Asian markets advanced nicely overnight, including a 2.25% climb in the Hang Seng Index ($HSI) and a 1.05% rise in Tokyo's Nikkei ($NIKK). In Europe, the London FTSE ($FTSE) and French CAC ($CAC) were fractionally higher. The German DAX ($DAX) is closed today for a holiday.

U.S. equity futures, taking a cue from another rise in the TNX, are higher this morning with Dow Jones futures suggesting another all-time high at the opening bell - up 31 points with a little more than 30 minutes to go to today's opening bell.

Lennar (LEN) and Paychex (PAYX) will no doubt see heavy action after both posted better than expected results this morning.

Current Outlook

So far, the S&P 500 has not run into any short-term momentum issues. Given the breakout to all-time highs, there isn't any price resistance to use as a possible level where we might see sellers emerge. It's more difficult to predict a near-term top with blue skies (no overhead price resistance) ahead. The first potential sell signal would be the emergence of a negative divergence on a shorter-term intraday chart. Below is the past three months 60 minute chart for our benchmark index:

As you can see, the S&P 500 struggled each of the past two times that we saw a negative divergence emerge (higher price highs accompanied by lower hourly MACD readings). While I admit we are overbought in the very near-term after a solid advance over the past week, there are no real signs of slowing momentum yet as the hourly MACD continues to rise. I suspect we'll have momentum issues later this week, but for now it's difficult to be bearish.

As you can see, the S&P 500 struggled each of the past two times that we saw a negative divergence emerge (higher price highs accompanied by lower hourly MACD readings). While I admit we are overbought in the very near-term after a solid advance over the past week, there are no real signs of slowing momentum yet as the hourly MACD continues to rise. I suspect we'll have momentum issues later this week, but for now it's difficult to be bearish.

Sector/Industry Watch

Materials led the action on Monday and its best performing industry group was paper ($DJUSPP). The group closed at its highest level since a significant high volume gap lower back in February. Volume increased and finished among its top 5 or 10 volume days over the past 4-5 months to confirm this price breakout. I'd look for a test of the January high to complete the right side of a cup and test a very critical price resistance area. Here's the visual:

To the downside, look to the rising 20 week EMA as support during any selling. Technically, paper definitely looks for higher prices in the fourth quarter and into 2018.

To the downside, look to the rising 20 week EMA as support during any selling. Technically, paper definitely looks for higher prices in the fourth quarter and into 2018.

Historical Tendencies

Since 1950, the S&P 500 has performed very well during the first week of October. The annualized return from October 1st through the 6th is +37.93% and is four times the 9% annual return that the benchmark S&P 500 enjoys. Monday got this period off to an excellent start.

Key Earnings Reports

(actual vs. estimate):

LEN: 1.06 vs 1.01

PAYX: .62 vs .60

Key Economic Reports

None

Happy trading!

Tom