Market Recap for Thursday, December 27, 2018

The final two hours on Wall Street yesterday was quite the finish. After languishing deep in red territory throughout much of the session, the bulls took complete charge into the close. The Dow Jones, down more than 600 points just past 2pm EST, was threatening to give back most or all of its previous record-setting 1000+ point gain from Wednesday. That obviously would have been a devastating blow to the bulls, which were already heavily-scarred from a December punishing like no other. Instead, the bulls turned a very rough session into a sparkling one with a near 900 point rally in the last two hours. 500 of those points came in the final 40-45 minutes in a very impressive turnaround. It felt great, but I doubt it's going to last so enjoy it while it's here.

Listen, this is an emotional market right now. The swings back and forth are dizzying to say the least. The real battle, the one that decides what the future is for 2019, hasn't even begun. There are too many considerations and resistance levels to discuss in one blog article, so my plan is to simply take this market one day at a time. What we saw on Thursday was an unwinding of a VIX spiraling out of the control to the upside. That set the stage for a snapback rally and we're seeing it. As our major indices move higher, though, the onus will be on the bulls to show they can extend it beyond a typical oversold bounce. I'm betting they cannot. The VIX fell just 1.48% on Thursday, and that's rather unsettling as fear remains extremely high. The Dow Jones has rallied 1400 points off its Wednesday intraday low and the VIX is still at 30. That ought to tell us something about the market environment we're in. One piece of bad news could easily send us back to the recent lows, so keep that in mind if you're trading short-term.

Materials (XLB, +1.84%), industrials (XLI, +1.25%), financials (XLF, +1.20%) and healthcare (XLV, +1.20%) led to the upside. The U.S. Dollar Index ($USD) has weakened in December and that sets up well for materials during bullish market moves, at least in the very short-term. Real estate (XLRE, +0.23%) was the weakest sector as all 11 sectors did advance on the session.

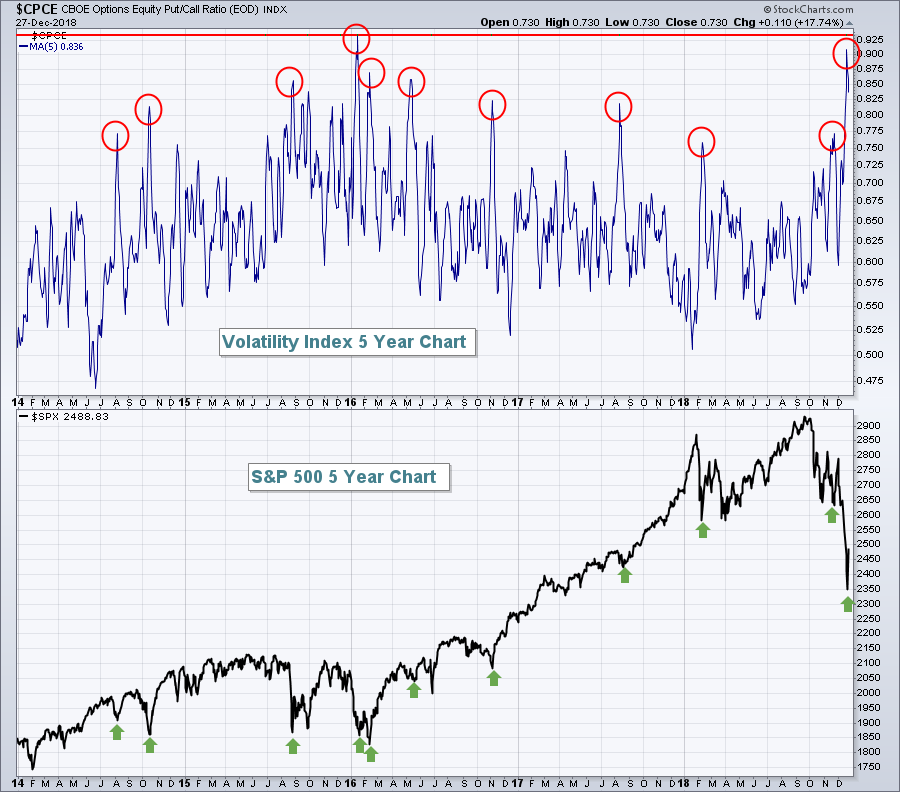

Honestly, I'm really not using technical levels of support and resistance to trade. We're in an extremely emotional market so I tend to watch the VIX and the equity only put call ratio ($CPCE) for sentiment clues as to future direction. In that light, take a look at the 5 day moving average of the CPCE this month and how it compared to recent highs:

Every significant spike in the CPCE has coincided with a fairly important S&P 500 price support level and bounce. It's simply the way the market works. When everyone turns bearish, the stock market bottoms. But this signal can be very, very short-term in nature, which is why we should be on high alert. CPCE readings will go higher if we are, in fact, in a bear market. In the 2007-2009 bear market, we saw readings that eclipsed the 1.00 level.

Every significant spike in the CPCE has coincided with a fairly important S&P 500 price support level and bounce. It's simply the way the market works. When everyone turns bearish, the stock market bottoms. But this signal can be very, very short-term in nature, which is why we should be on high alert. CPCE readings will go higher if we are, in fact, in a bear market. In the 2007-2009 bear market, we saw readings that eclipsed the 1.00 level.

Bottom line: Don't think for a minute that we can't go lower with so much bearish sentiment. However, these sentiment extremes do typically result in a short-term reversal and that's what we're in the midst of now. Enjoy it while it lasts.

Pre-Market Action

Despite the bounce in U.S. equities, the 10 year treasury yield ($TNX) actually closed at another low on Thursday, down more than 5 basis points to 2.74%. This suggests to me that the current bounce in stocks is a very temporary one. Money is not rotating from the bond market to support a more significant advance. Until that happens, treat the bigger picture downtrend in stocks with the utmost respect. The second half of November was a perfect example. The S&P 500 rose from 2640 to 2800 from the Friday after Thanksgiving to December 3rd, but the TNX showed much more trepidation, falling from 3.08% to 2.98% over the same period, establishing new 10 week lows.

Crude oil ($WTIC) is higher by 1.50% this morning to $45.28 per barrel, also remaining rather close to its recent lows - not a great signal for global economic conditions. Asia was mixed overnight, while we're seeing solid action in Europe.

Dow Jones futures are poised for a continuation of its recent rally, up 112 points with nearly two hours before the opening bell.

Current Outlook

I'd much prefer afternoon strength over morning strength. Many times in a downtrend, you'll see our major indices showing early strength only to crater later in the session. But once the tide turns and the short-term character of the market turns higher, afternoon strength tends to become the norm. That's what we've witnessed the past two trading sessions and it's much more bullish:

The dotted directional lines show the morning action, action you really shouldn't trust. The solid dotted lines show the afternoon action, which has been much more bullish the past two sessions. While certainly never any type of guarantee, the probability is that we'll see the short-term direction remain bullish so long as buyers line up in the afternoon and into the close.

The dotted directional lines show the morning action, action you really shouldn't trust. The solid dotted lines show the afternoon action, which has been much more bullish the past two sessions. While certainly never any type of guarantee, the probability is that we'll see the short-term direction remain bullish so long as buyers line up in the afternoon and into the close.

Sector/Industry Watch

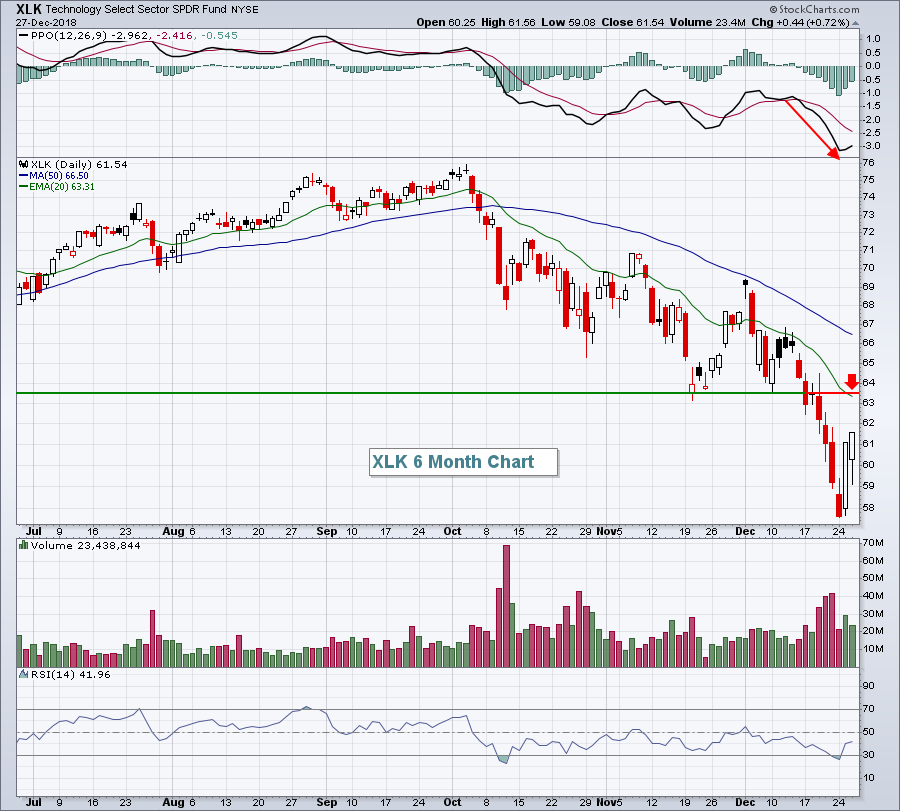

The technology ETF (XLK) is one that I always watch. When technology is downtrending, it's not normally a good thing for the overall stock market. Currently, we have a clear downtrend in play with a very weak PPO, one that favors the bears, and a bounce the past two days that's suggesting the XLK might have difficulty if it were to rise another 2-3%:

The price breakdown and the declining 20 day EMA both reside close to 63.50, or roughly 3% above the closing price on Thursday.

The price breakdown and the declining 20 day EMA both reside close to 63.50, or roughly 3% above the closing price on Thursday.

Historical Tendencies

Recently, American International Group (AIG, full line insurer) lost a third of its market cap over a 7 week period. If history is any guide, its struggles are likely to continue. Over the past two decades, AIG has averaged losing 4.6% and 4.3% during the months of January and February, respectively. A life insurer, Unum Group (UNM) has also struggled during the January-February timeframe with average monthly losses of 1.9% and 5.4%, respectively.

Key Earnings Reports

None

Key Economic Reports

December Chicago PMI to be released at 9:45am EST: 62.4 (estimate)

November pending home sales to be released at 10:00am EST: +1.5% (estimate)

Happy trading!

Tom