| THIS WEEK'S ARTICLES |

| John Murphy's Market Message |

| FOREIGN STOCKS ARE LEADING U.S. LOWER |

| by John Murphy |

FALLING FOREIGN CURRENCIES... Last week's message showed the U.S. Dollar Index rising to the highest level in twenty years. That's due largely to the fact that the Fed has been hiking rates faster and higher than most foreign bankers. What's good for the dollar, however, is bad for foreign currencies and stocks tied to them. Chart 1 shows the Euro and British Pound falling to the lowest level in two decades. Although not shown here, the Japanese yen has done the same which has forced its central bank to intervene to support the currency. Emerging market currencies are falling as well. Chart 2 shows the WisdomTree Emerging Currency Strategy Fund under heavy selling pressure.

FALLING CURRENCIES BOOST INFLATION... Last week's message also explained why falling foreign currencies create problems for central bankers. For one thing, falling foreign currencies can contribute to rising inflation in their economies. That forces foreign central bankers to raise rates not only to fight inflation, but to support their falling currencies as well. That can also have a negative effect on foreign stocks which are underperforming stocks in the U.S.

Chart 1 Chart 1

Chart 2 Chart 2

FOREIGN STOCKS UNDERPERFORM U.S... The weekly bars in Chart 3 show the MSCI EAFE iShares falling to the lowest level since 2020. The blue solid line is a ratio of the EAFE divided by the S&P 500 which is also falling. That relative strength ratio shows foreign developed markets falling faster than the U.S. Chart 4 shows the MSCI Emerging Markets iShares falling faster than U.S. stocks as well. That may carry bad news for U.S. stocks.

Chart 3 Chart 3

Chart 4 Chart 4

GLOBAL COMPARISON... The blue line in Chart 5 shows the MSCI World ex USA Index leading the S&P 500 lower. That index includes foreign developed and emerging markets. Their relative weakness in clearly weighing on the SPX. Global stocks are highly correlated which means that they usually trend in the same direction which right now is down. Falling foreign currencies are one of the reasons that foreign stocks are doing so poorly. Their poor relative performance is just another sign that global economies are in recession or heading into one. That's not good news for them or the U.S.

Chart 5 Chart 5

|

| READ ONLINE → |

|

|

|

| Art's Charts |

| Understanding Bear Markets and Setting Expectations |

| by Arthur Hill |

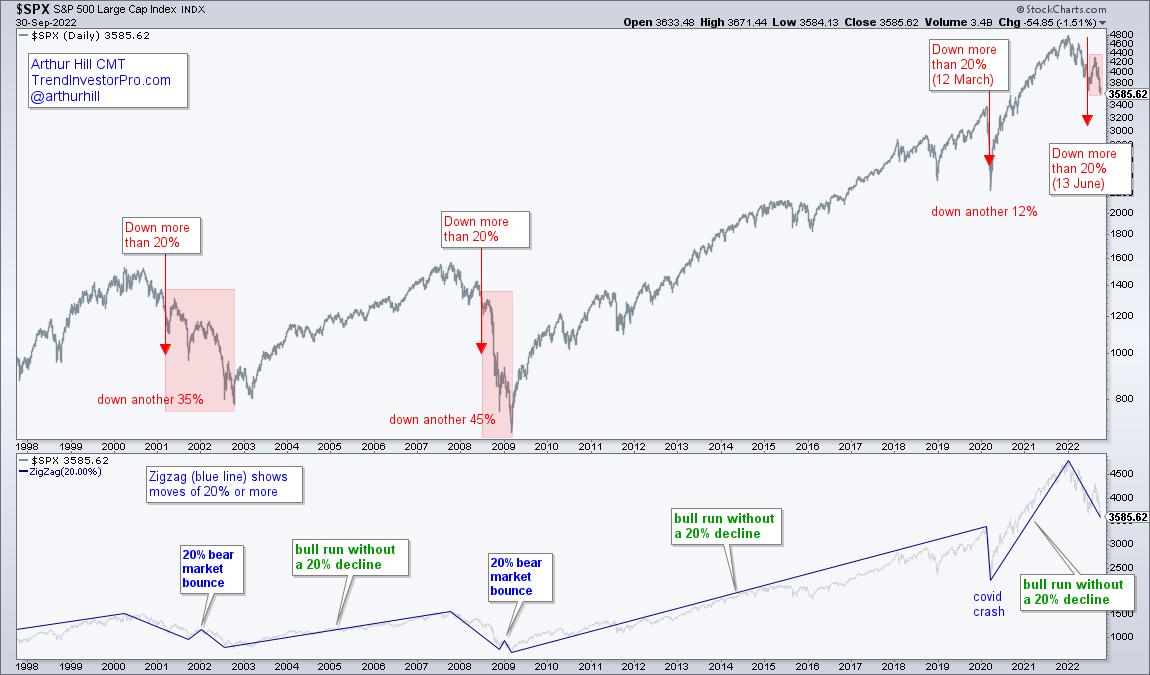

Technical analysts often scoff at the notion that a 20% decline marks a bear market. However, a look back shows that further losses are certainly possible after a 20% decline. Over the last 25 years, the last two bear markets started with declines in excess of 20% and the S&P 500 lost another 12% after the 20% decline in mid March 2020. The red arrow-lines on the chart below show when the S&P 500 declines more than 20% from a peak (daily closing prices). The red shading shows the subsequent declines. The S&P 500 fell another 35% after the initial 20% decline into early 2001 and fell another 45% after the initial 20% decline in 2008. The index fell another 12% after the initial 20% decline during the covid crash and then rebounded. Technical analysts often scoff at the notion that a 20% decline marks a bear market. However, a look back shows that further losses are certainly possible after a 20% decline. Over the last 25 years, the last two bear markets started with declines in excess of 20% and the S&P 500 lost another 12% after the 20% decline in mid March 2020. The red arrow-lines on the chart below show when the S&P 500 declines more than 20% from a peak (daily closing prices). The red shading shows the subsequent declines. The S&P 500 fell another 35% after the initial 20% decline into early 2001 and fell another 45% after the initial 20% decline in 2008. The index fell another 12% after the initial 20% decline during the covid crash and then rebounded.

The indicator window shows the Zigzag indicator (blue lines) with the S&P 500. This indicator shows swings that are greater than 20%. Note that there were no 20% declines during three bull runs (2002 to 2007, 2009 to 2020 and March 2020 to December 2021). The S&P 500 also went the entire 90s without a 20% decline.

The blue callouts highlight two bear market bounces of at least 20%. These two bounces occurred over a year after the S&P 500 peaked and the index moved to new lows after these bounces. We already witnessed a 17% bear market rally from mid June to mid August. Judging from the last two bear markets, we can expect another counter-trend bounce at some point, but this is unlikely to be the bounce that ends the bear market.

No two bear markets are exactly the same, but we can study the last two bear markets to better understand the dynamics and set expectations going forward. In particular, there are the three phases of a bear market according to Dow Theory. We have also yet to see a capitulation phase that sets up a monster advance that typically signals an end to the bear market. This week I dissected the two bear markets and applied the lessons learned to the current bear market. This detailed report and accompanying video are available to subscribers of TrendInvestorPro. Click here for immediate access.

---------------------------------------

|

| READ ONLINE → |

|

|

|

| The Canadian Technician |

| Staring at the Quarterly Charts |

| by Greg Schnell |

First off, the markets have been testing the June lows for 6 days. Does this eventually give way, or do we hold? There's no shortage of bad news out there; could this be the worst of the worst, and it gets marginally better from here?

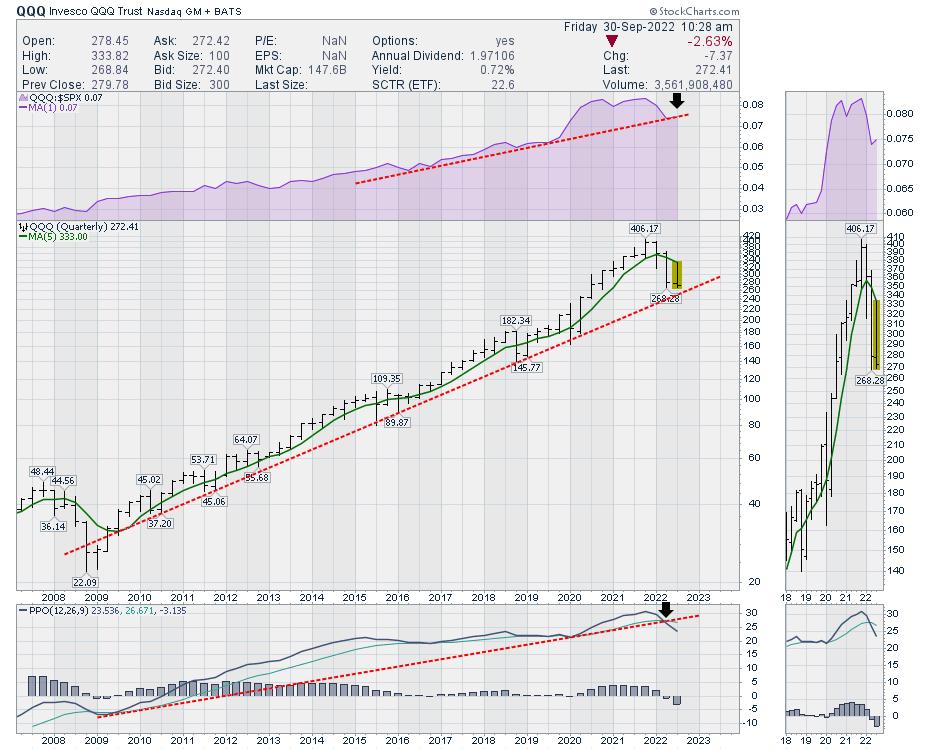

For the Nasdaq 100, ending the 3rd quarter on the bottom of the quarterly price bar sure doesn't look good. I notice the relative strength trend of the QQQ, compared to the $SPX in purple, is testing the trend line this quarter. We have not seen the Nasdaq 100 underperform the $SPX so significantly in the last 14 years. Look at the size of the drop over the last three quarters.

I have a 5-quarter moving average line in green that has rolled over for the first time since 2008. The PPO has broken the uptrend.

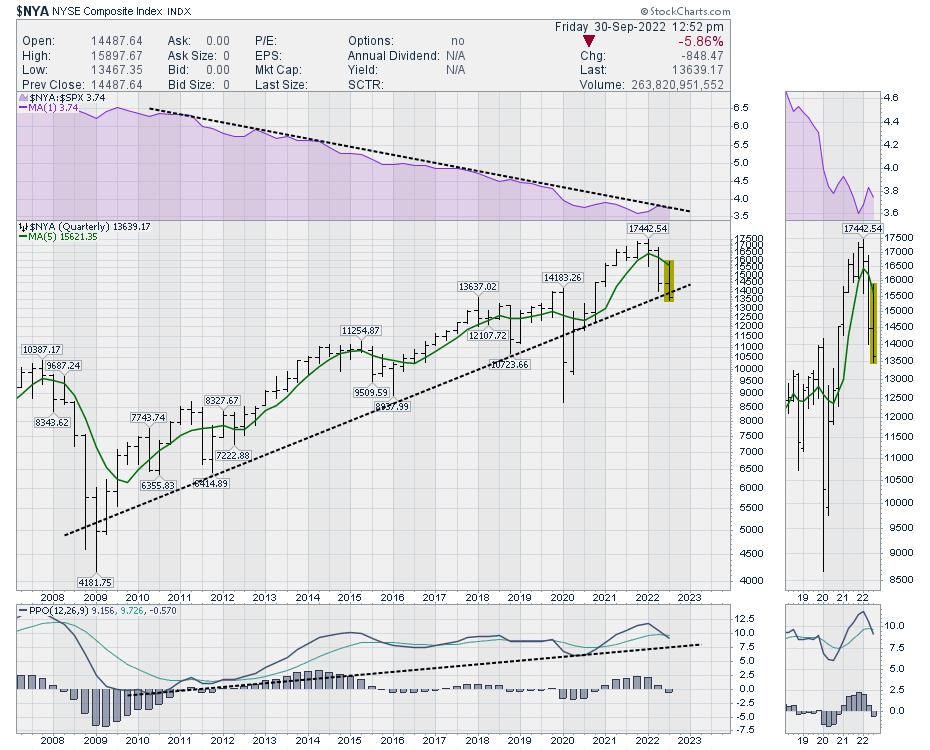

There is also the $NYA Composite, which covers the action for the entire NYSE market. The market composite typically underperforms the S&P 500, so that is not new, as shown in purple. However, this chart looks ready to close below the line. This line represents the economic uptrend we have been in since 2009.

Nine months ago, there was a huge amount of optimism as the indexes were in the top right corner. This video turned out to be very prescient. Did I get all the calls right? No, some charts changed direction. But we developed an expected plan from technicals and it played out.

FOr

Influential Events Of 2021

For fans of technical analysis, this will be a comforting video. For fans of fundamental analysis, this might work as an introduction to why technicals can help the investment focus.

Next week, we'll get the opportunity to see 17 technical analysts give us a view towards the fourth quarter at ChartCon 2022.

ChartCon 2022

In particular, I am going to be putting out some of my best charts on the outlook for the fourth quarter!

I hope you get some insights and ideas from the conference. There is something special when you get a strong overview of the markets after 11 months pointing lower from 17 analysts. These analysts are some of the best in the business! Technicians will be noticing the changes long before the fundamentals start to improve.

|

| READ ONLINE → |

|

|

|

|

|

| The Traders Journal |

| Five Decades Of Personal Stock Market Passages, Tools, Lessons And Stories: Part 3 |

| by Gatis Roze |

When I began investing full-time, my methodology's foundation was based on William O'Neil's CANSLIM® approach. It's a deeply researched and proven strategy. The AAII's own ongoing trading models validate that fact. When I began investing full-time, my methodology's foundation was based on William O'Neil's CANSLIM® approach. It's a deeply researched and proven strategy. The AAII's own ongoing trading models validate that fact.

For the next three decades, my efforts were focused on how best to incrementally increase the probabilities of success for each of O'Neil's attributes and to layer on my own enhancers. In reality, our book "Tensile Trading: The 10 Essential Stages of Stock Market Mastery" spotlights dozens and dozens of what I'll label "Probability Enhancers".

When you understand and embrace probabilities as an investor, you find that the emotional burden of losses and the exuberance of profits level out and become more manageable. Grasping probabilities facilitates you taking a present loss knowing that you are now one step closer to your next big win. As you read about my passages, tools and lessons, consider each in the context of offering you a "probability enhancer" which when diligently applied should outperform the market!

Passage 1: A Sell Discipline

It hasn't been a cake walk, but I've learned to tame my two wild horses — my own inner fear and greed. The first stage was to believe my charts. Embrace that what they were telling me was indeed the truth. The second stage was to convince my ego to partner with me.

Early on, precious time was lost in this little negotiation as I tried to convince my ego to accept the charts reality before being able to pull the sell trigger. After years of effort, I've achieved the discipline to convince my ego beforehand to recognize what "wrong" looks like within each chart in each position I take.

When the charts tell me to sell, I don't freeze or begin a new negotiation. I'll react appropriately based on my previous sell scenario. It's less stressful and I'm free to move onward — closer to my next winning trade. An investor's mental energy is the fuel you run on. Vacillation and failure to promptly sell a loser consumes precious fuel that could be used instead on trading your next winner.

In his book, Trading in the Zone, Mark Douglas describes the four types of investor fears.

- Losing money

- Missing an Opportunity

- Leaving Money on the Table

- Being wrong

It's essential that you address each one in detail in hand with your ego prior to entering a trade. Understand that this negotiation — this sell discipline — is meant to protect your profits and protect you from yourself. Without it, you are falling prey to the old cliche "shutting the barn door after the horse has bolted" — late to action and after the damage is done.

I have great respect for Jesse Livermore who I believe was a generational trader. His words remain with me. "My plan of trading was sound enough and won oftener thank it lost. If I had stuck to it, I'd have been right perhaps as often as 7 out of 10 times." Even Jesse Livermore had challenges doing what he knew he should do. My experience is that there are two types of losses. The first type of loss is simply a result of the laws of probability and is to be expected even when you follow your methodology.

The second type of loss requires much more introspection and brutal self-honesty. Losses that result from ignoring your trading plan or similar bad behavior is what needs to be focused upon and minimized. There is no place for denial in successful investing. Buying is easy. You always have lots of company. Just google stock market books. The overwhelming majority of these books are all about buying. Don't quote me on this, but intuitively the ratio of books on buying equities versus selling strategies is 1,000-to-1. It's always been the way.

This is precisely why in our book, Grayson and I devote an entire chapter to selling methodologies and the requisite mindset and routines to succeed. Remember — your goal is to stay in the game. If you protect yourself on the downside from all the inevitable mini-panics, the rallies will take care of you. This is not the forum to dig into that here in detailed fashion, but I would encourage you to check out this blog I wrote: "Selling Methodology: 1 + 1 = 3" (October 16, 2015).

Passage 2: Seize The Free 1%

This is more an awakening versus a passage. I realized that there is a good deal of low hanging fruit that investors can gather in the way of finding an extra 1% and retiring early. Do the math; that's all it takes. Investing is a game of inches. Yes, it takes only 1%, and if you start young, it's a slam dunk. Warren Buffett is always talking about the magic of compounding. It's absolutely true.

So where is the 1%? It's all around you hiding in plain sight — simply there for the taking if you focus on costs and fees. This awakening is more of a mindset, an attitude to persistently consider costs, expenses and fees as an investor. I'm living proof that if you embrace my two mantras, you should outperform the market. (a) Embrace all my probability enhancers when you trade equities. (b) Embrace the 1% mentality. Find free money by simply minimizing costs, expenses and fees.

Let me say again that by embracing these two mantras, you should outperform the market. It's mind-bending how higher fees and expenses create a slow burn of your assets over time. In addition, not acting defensively and thinking about tax minimization also vaporizes those same assets. Remain vigilant because the money management world is expert at enticing you to play the "shiny object game" which yields higher fees for them — lo & behold! It all comes out of your pocket.

Basic case in point: there are over two dozen ETFs that represent the S&P 500. The Vanguard ETF (VOO) has fees of 0.03% which is basically free. SPY— the SPDR S&P 500 is 0.095% which is three times higher. From there, other ETFs skyrocket to stupid expense levels and some investors buy them. It's sheer madness. It's the same S&P 500 Index! Look at the PerfChart of two S&P 500 index funds — SPY and RYSPX. They both hold EXACTLY the same equities. There's no "expert stock picking" involved here. Had you invested $100,000 in 2003 in SPY and your twin sibling invested the same in RYSPX, nineteen years later you'd have $426,000 while your twin would have only $249,000. The difference would be caused entirely by fees. I'd say your twin's investment in RYSPX is both sticky and stupid — but I digress!

About a decade ago in my class, I bought equal amounts of two identical gold ETFs. The only difference between them was that GLD (the more popular of the two with twice the assets) had 0.40% expenses. IAU is half the size and logically should have had higher expenses. But IAU came in with 0.25% expenses.

I recently sold both of these ETFs. The profit difference shocked me. I knew there would be one, I wasn't expecting the dollars involved. IAU made me far more money. Do your diligence. It's free money if you do — low hanging fruit which adds to your 1%. This blog is not the place for a granular description of all the low hanging fruit to save you 1% but I'll briefly list a few examples.

- Cash balances — pay attention! One click or phone call can move dollars from zero interest accounts to significant interest income accounts. Don't ignore this free money.

- I've already given you an ETF example. With every ETF, explore alternatives. Try ETF.com.

- Mutual funds — don't get me started! I'm not picking on American Funds, but they offer the exact same funds — in some instances under a dozen or more different ticker symbols. Why? To maximize front-end loads, 12b1 fees, redemption fees, expenses, etc. Beware of money managers that put you in the high fee funds (for their benefit) versus cheaper versions of the same fund.

- Advisor fees — 1% a year doesn't sound like much, but you'd be stunned what it costs you over 10 - 20 years. And remember, all fees are negotiable. So negotiate and renegotiate as your assets grow.

- Think defensively. Think tax minimization. There's a whole population of governmental professionals poised to think of new ways to get at your assets. A top tier estate planning attorney and accountant are a priority for all investors — not a luxury!

The bottom line: with minimal effort, you can make your money work better for you.

TOOL #1

An appropriate example of my "probability enhancer" approach is "Seasonality Charts." This tool highlights stocks, ETFs and mutual funds tendency to perform better in some months and worse in other months on a recurring basis. (Check out the ChartSchool articles on StockCharts.com.)

In your arsenal of Asset Allocation rebalancing tools, put the winds of probability at your back by selling positions into the strongest months of the year (using Seasonality) and accumulating positions during historically weak months. Overtime, selling into strength and buying on weakness delivers profits. In this previous Traders Journal blog, I identified six equities with historically strong performances in December. A month later in this Traders Journal blog, I recapped the actual performance. This basket of six equities with favorable seasonality bested the market by 150% in December.

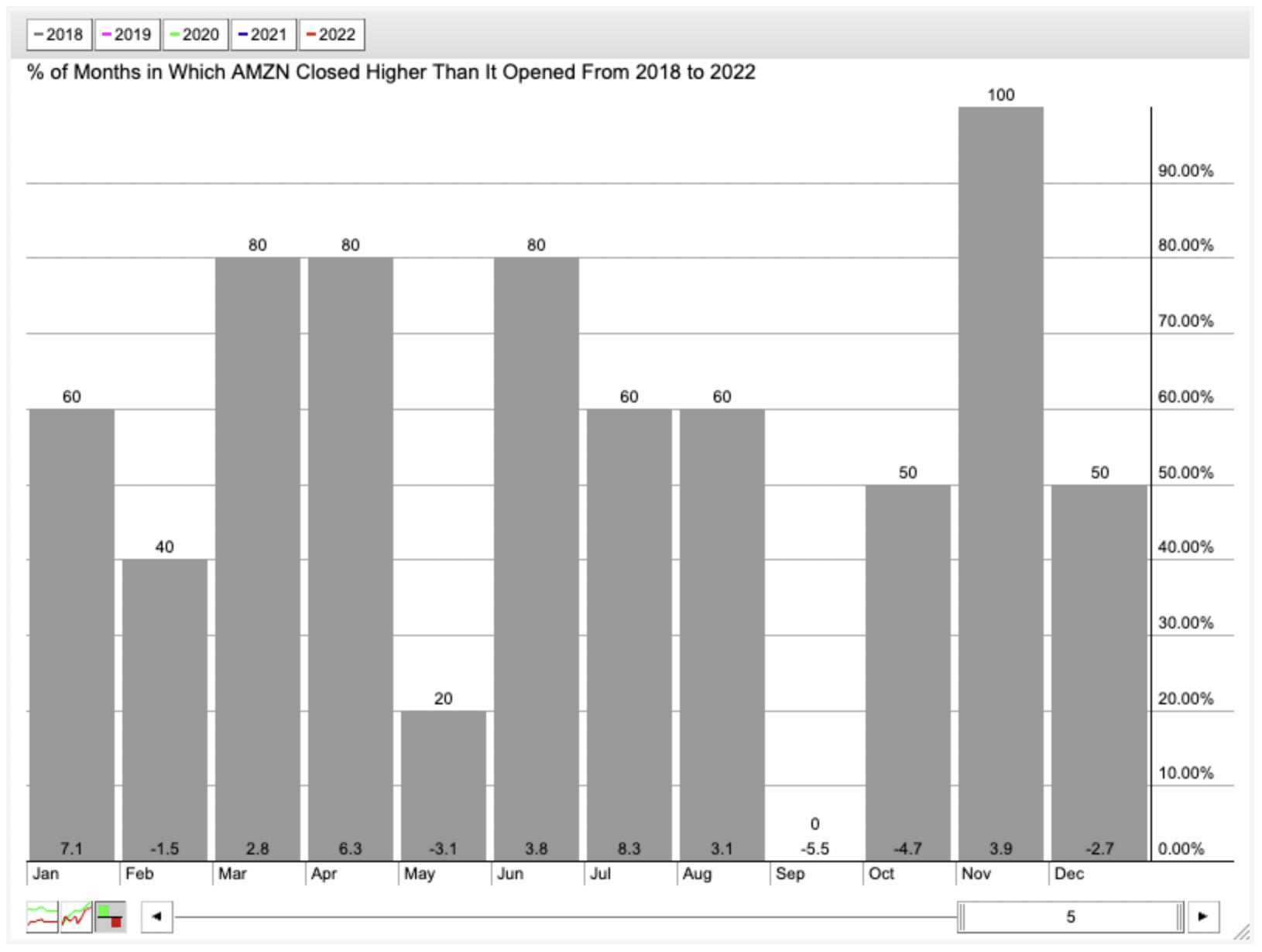

Seasonality works! A final example. I looked at four of the largest equities in the S&P 500 over the past 5 years: Apple, Amazon, Tesla and Google.

- All have one month where they had positive price appreciation 100% of the time. Never down in that month.

- All have one weak month or more where either they have never experienced any price appreciation or have only one year out of the past five that had positive price movement for that month. Make probabilities work on your behalf.

To some of you, this might not seem like a seismic investment recommendation. But many investors see that seasonality is indeed a probability enhancer and multiple enhancers cumulatively add up to an appreciable growth in your bottom line.

TOOL #2

There are great insights to be had when you focus on the power of varied time frames — analyzing the markets or an equity through a series of lenses, each one a tighter time frame than the previous. I call this methodology "telescope to microscope". Aligning the trends in various periods shifts the odds in your favor. A corollary methodology applies the same principle top down. To further empower your investing probabilities, you only buy in an up trending market. Then look for the strongest sector. Since sectors are a collection of industries, you search out the strongest industry in the uptrending sector. Finally, you gravitate to the best-of-breed stocks in the strongest industry.

I have a pre-formatted chart style to help you.

FIVE LESSONS

- Have a "sell strategy". If you don't, the market will assign you one and call it "KABLOOEY." It's both a cliche and a fact that "the first loss is the cheapest" and "mental stops don't work."

- Don't buy 100% of your position all at once. Stage your purchasers in tiers. My personal rule is never to buy a second position unless my first position is profitable. I've witnessed far too many investors who try to catch a falling knife. They buy an equity at $20. It falls to $15, and they buy more — all the way down to bankruptcy. Think logically. If you bought it at $20 and it's now $15, the market is telling that you were wrong. Stop being wrong! Don't do more wrong. Ralph Vince has written a number of books on the mathematics of money management and risk analysis which unequivocally prove that pyramiding both into and out of a position (albeit selling faster than buying) is the scientifically proven optimal strategy. Here's a link to a more detailed blog on the subject.

- Buy "Best of Breed". I like my cars to be fast, reliable and luxurious so my ownership experience is 5-star. I'm the same with stocks. I buy the best because I want my positions to offer a similar 5-star ownership experience. I just don't get it. Why would a pharmaceutical investor not buy Eli Lilly Co. (LLY) and buy Omeros (OMER) instead. I buy only "best of breed" equities because it's not worth buying second or third tier companies. Yes, the price-to-earnings ratio is higher, but so is my peace of mind.

- Know your own bandwidth! Before I attended Wall Street University (i.e. I started trading) and paid lots of tuition to learn how to invest with consistent profitability, my holdings were vast in number. Too vast. After years of judiciously reviewing my winners and losers, I discovered my positive performances were directly coupled to having fewer positions. I now have 10 stocks, 10 ETFs and 10 mutual funds. I never buy or acquire a new position without first removing another. Having said that, if you have Bill Gates' bandwidth, perhaps 20 is fine.

- Be Mr. / Mrs. Adjustable Elastic. The market is always right and the market is always changing. Yes, Mr. High IQ Big Shot — the markets demand compliance. I love to quote Charles Darwin. "It is not the strongest of the species that survives, not the most intelligent that survives. It is the one that is most adaptable to change." Buy and Monitor — not Buy and Hold — is my mantra.

Finally, a little story. I had a finance professor in Business School who was renowned on Wall Street for creating the Sharpe Ratio, CAPM — The Capital Asset Pricing Model (including Alpha and Beta) and other common tools. Understandably, he won a Nobel Prize for his work. The point being, he was brilliant, cerebral and frankly sometimes on a totally different tier. He came to class one afternoon and rhapsodically described in fine detail this new theory he had developed. After what seemed like eternity, one of my classmates who had been an investment banker said, "Professor Sharpe, this is interesting but how do we make money with it?" To which Professor Sharpe replied, "I don't know, but isn't it cool?!"

My point being that investing attracts many brainy folks who wander off intellectually into cerebral frontiers that are indeed interesting but won't help you become a better manager of your money. One prime arena I'll point to is the hundreds of technical indicators that have been created where frankly most should be siloed since they only contribute to more complexity instead of profits.

p.s. I'm really looking forward to exchanging ideas and thoughts with you October 7th and 8th at ChartCon 2022. I hope you join all of us at this very special event! CLICK HERE for more information and to register.

Trade well; trade with discipline!

Gatis Roze, MBA, CMT

StockMarketMastery.com

|

| READ ONLINE → |

|

|

|

| Martin Pring's Market Roundup |

| Inflation is All the Rage, but Many Market Signals are Pointing in a Different Direction |

| by Martin Pring |

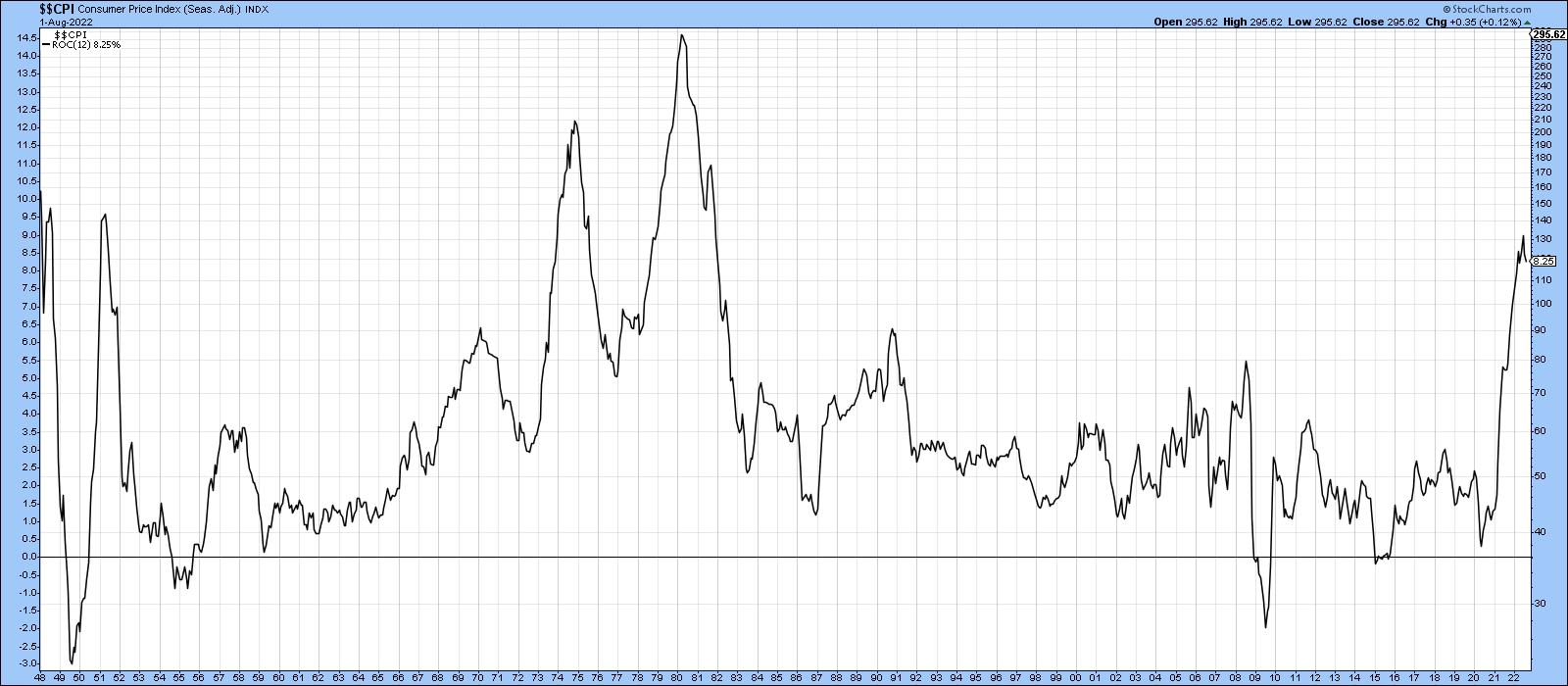

Polls show that the number one issue with voters is inflation, but some intermarket relationships are signaling otherwise. I am not saying that inflation is about to be wrestled to the ground, but it goes in waves, as you can see from Chart 1. Also, once prices go up, they rarely come down. There are only three instances of that happening since 1949, and each was short-lived. So, what I am saying is that it's very likely, based on market signals, that the 2020-202? wave is probably in the process of cresting.

Chart 1 Chart 1

Here is my reasoning.

Let's start with gold, which has traditionally been regarded as an inflation hedge. In reality, though, like everything else, it depends where you buy it. Chart 2 shows that January 1980, for instance, would not have been a good time acquire the yellow metal, because it is still below that level today. Compare that to the the turn of the century, when gold was being offered at bargain basement prices.

Chart 2 also features the quarterly Coppock Curve. The green shading indicates when this oscillator has been above its 8-quarter MA. The unshaded areas therefore tell us when this technique is in a negative mode. Since it has just dropped below its moving average, inflation-adjusted gold is now officially in a bear market. Further evidence of a bear trend comes from the price, which has just violated its secular up trendline.

Chart 2 Chart 2

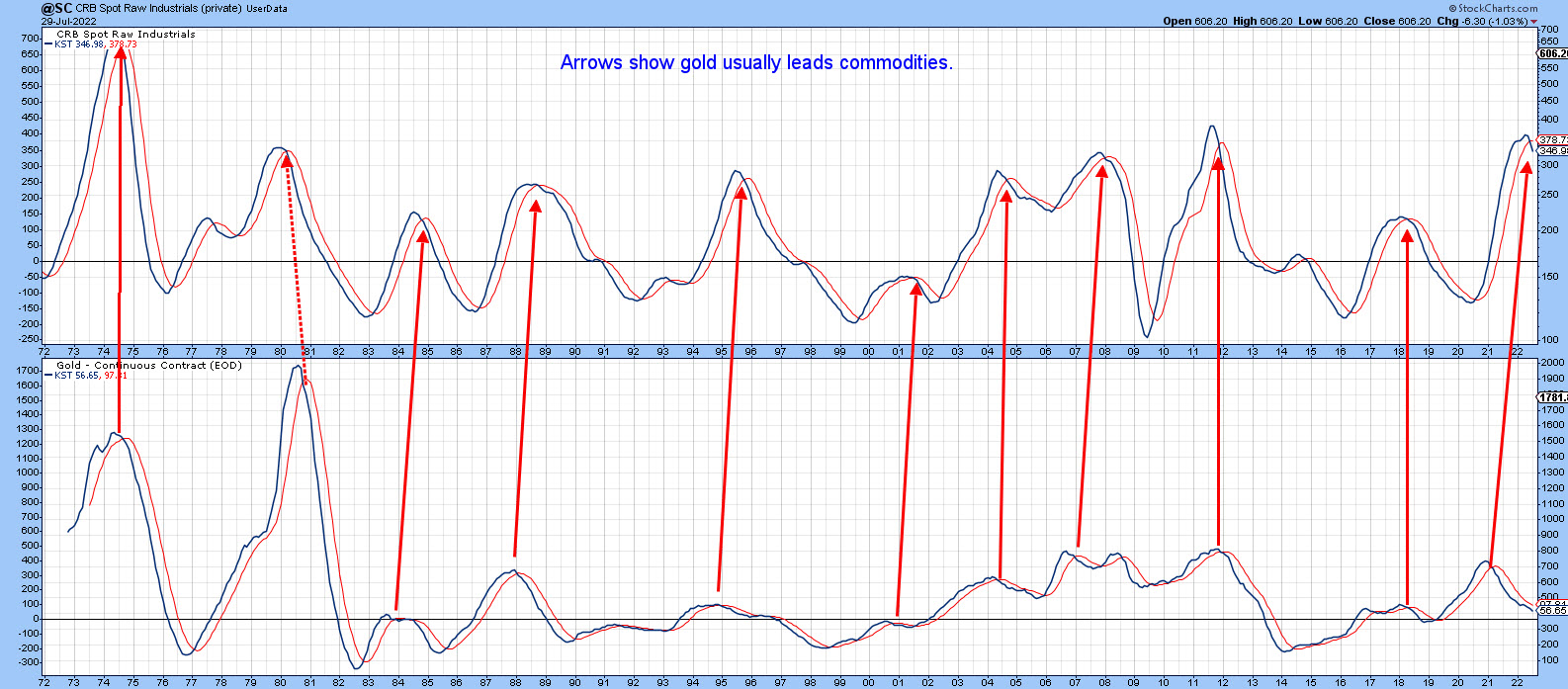

This breakdown is important because gold weakness is usually followed by industrial commodity prices, a leading indicator of consumer price inflation. In that respect, Chart 3 shows that the KST for the gold price has a consistent habit of leading commodity momentum. It's not a perfect relationship, because the leads differ from cycle to cycle. There is even one example (1980) when gold lagged. The gold KST peaked at the beginning of 2021, well ahead of the CRB Industrials, which has only recently reversed to the downside. Based on previous action, lower commodity prices appear likely.

Chart 3 Chart 3

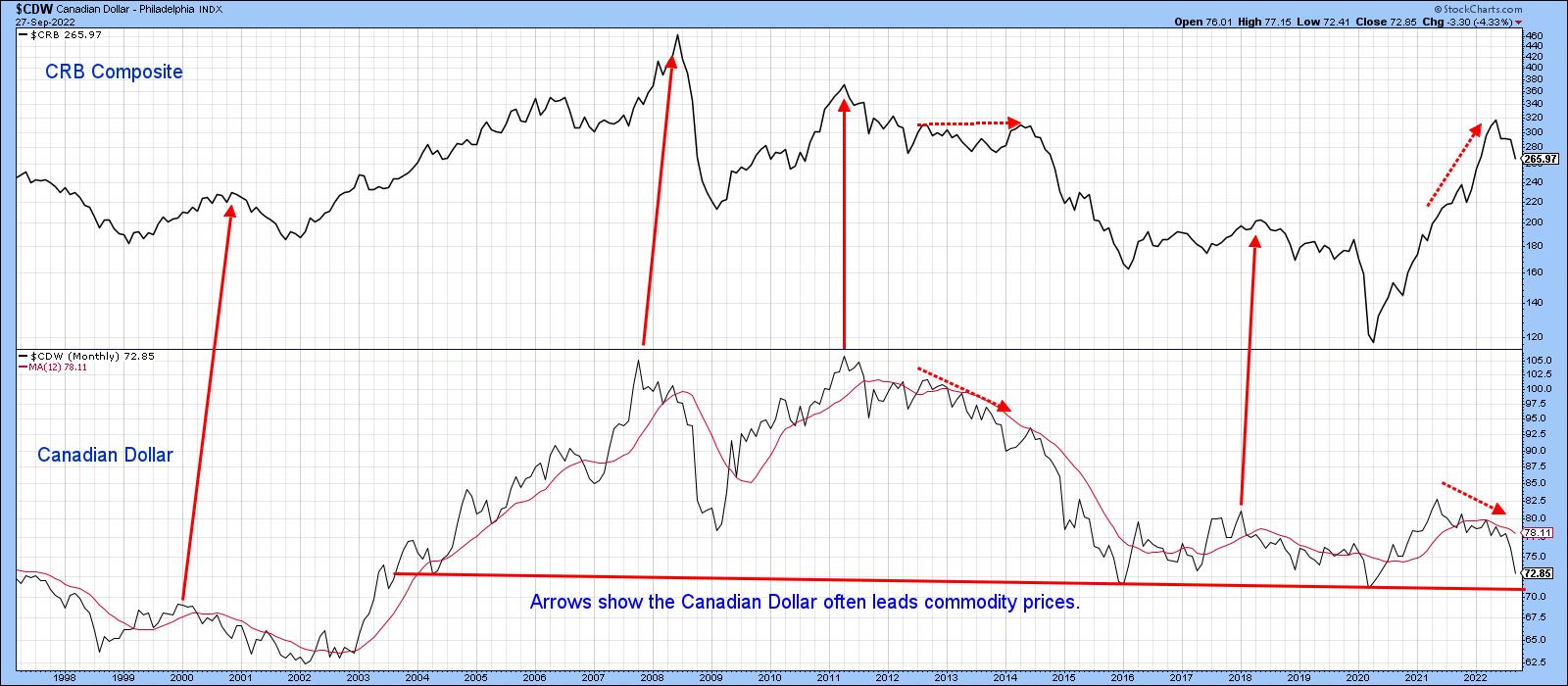

Another useful intermarket relationship comes from that that between commodity-sensitive currencies and commodities themselves. Chart 4, for instance tells us that the Canadian Dollar fluctuates in tandem with the CRB Composite -- not tick for tick, of course, but certainly in a broad sense. The solid arrows point up the fact that the currency usually plays a leading role. The two sets of dashed arrows indicate important divergences, when the dollar fails to confirm a new high in the commodity index. The latest divergence, which began in 2021, is particularly egregious. Finally, it is worth noting that the currency is approaching an 18-year support trendline at just over 70c. Needless to say, a breach would likely be followed by significantly lower currency and commodity prices.

Chart 4 Chart 4

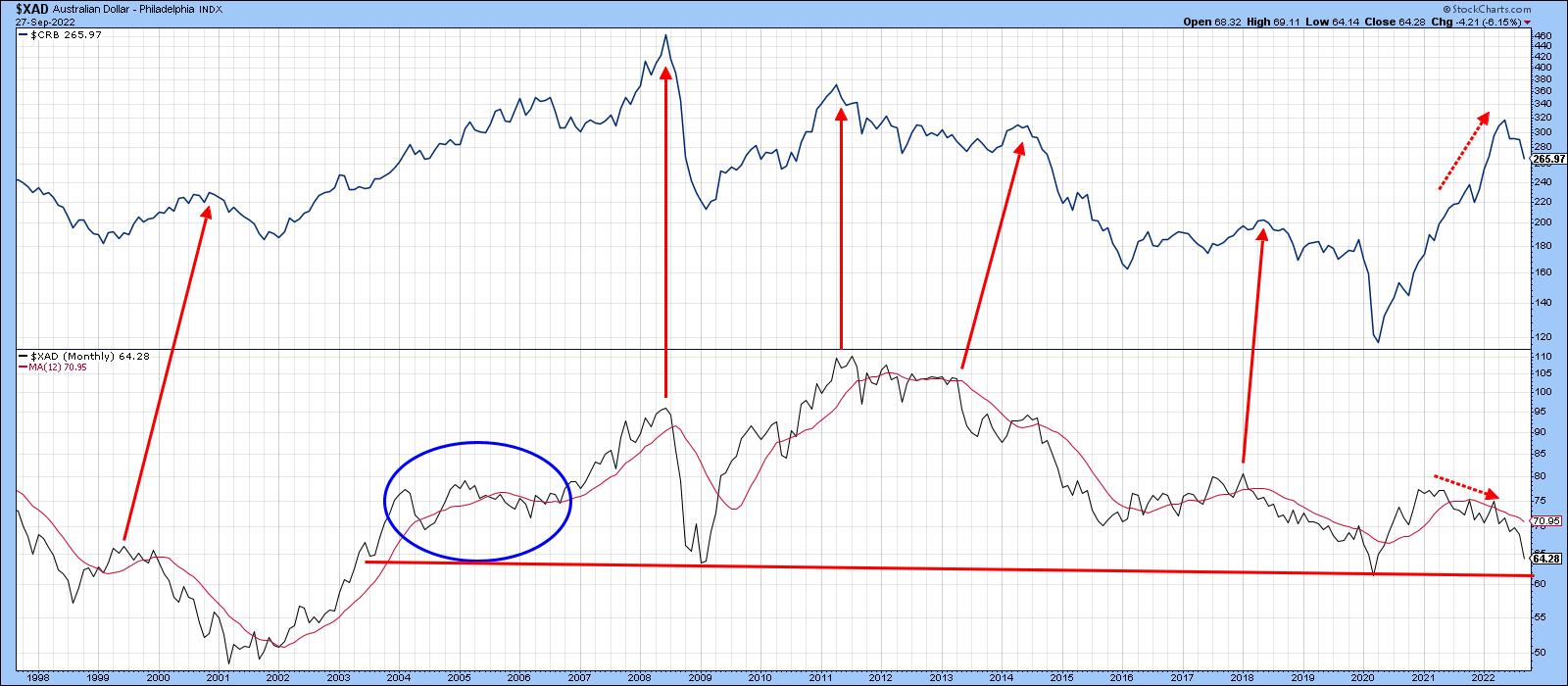

Chart 5 repeats the same exercise, but this time with the Australian currency. Once again, the two have been diverging in a negative fashion for commodities since 2021. This action continues to support the view, that commodities are headed lower on a primary trend basis. The Aussie dollar is also resting above a multi-year support trendline.

Chart 5 Chart 5

None of these relationships guarantee that the rate of inflation will moderate, but they do reveal that early bird inflationary signals are offering some hope at the end of the tunnel.

Time to for us Floridians to prepare for Ian!

Good luck and good charting,

Martin J. Pring

The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group of Walnut Creek or its affiliates.

|

| READ ONLINE → |

|

|

|

|

|

| Mish's Market Minute |

| Anticipating More Inflation |

| by Mish Schneider |

The PCE Price Index Excluding Food and Energy, also known as the Core PCE Price Index, makes it easier to see the underlying inflation trend by excluding two categories – food and energy – where prices tend to swing up and down more dramatically. The Core PCE Price Index is closely watched by the Federal Reserve as it conducts monetary policy. The PCE Price Index Excluding Food and Energy, also known as the Core PCE Price Index, makes it easier to see the underlying inflation trend by excluding two categories – food and energy – where prices tend to swing up and down more dramatically. The Core PCE Price Index is closely watched by the Federal Reserve as it conducts monetary policy.

It is crucial to prepare for adjustments in Fed policy and the credit markets, and adjust your trading accordingly, given the persistence of high inflation.

As seen above, The Fed-preferred inflation gauge (core PCE) remained elevated at 4.9% in August, as data released Friday remains far above the Fed's goal of 2%. It is worthwhile to think about how unique the selloff has been, why some anticipated it, and how might all of us trade better in the future.

I have one specific vehicle that I glance at daily, which tells me a lot about risk appetite and future equity returns. Anyone can look at this vehicle and quickly see where the market is headed.

In response to high inflation, central banks have aggressively raised rates quickly. The speed of these hikes will influence our economy, and the current stock market carnage is a side effect.

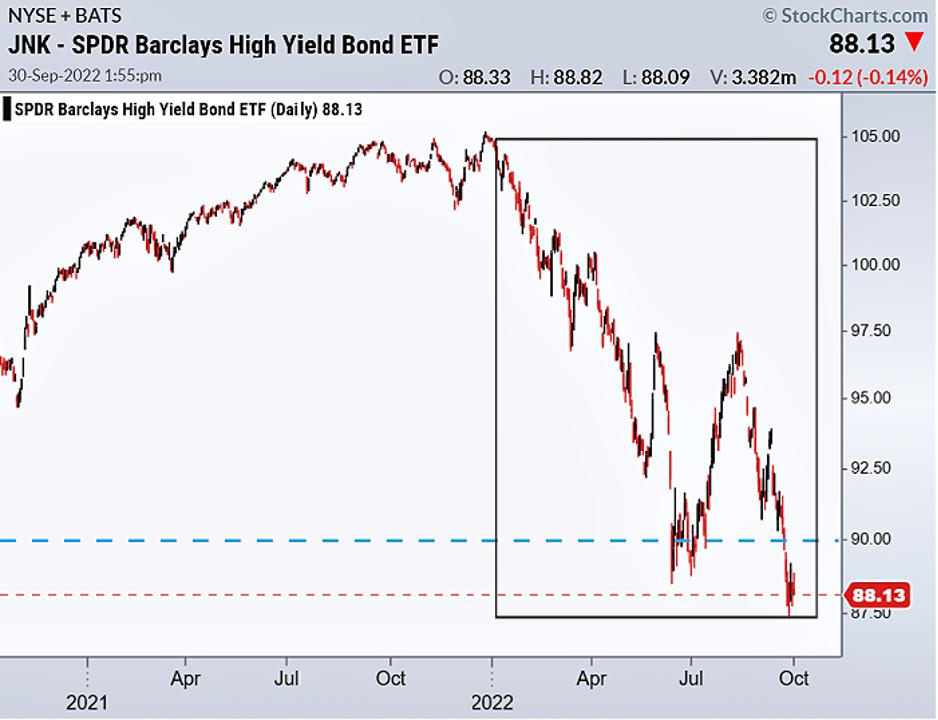

One of the many areas we watch are various credit markets and spreads. I follow the junk bond market. It usually leads the stock market, since the credit market is cyclical and tends to be inter-correlated with the economy. Please notice the Bloomberg High Yield Bond ETF (JNK) high yield corporate bond fund has taken out its previous low in the summer. The price tells us something important about the stock market's direction.

On new yearly lows, unless we see that reverse, take it as a harbinger that the selling in the whole market is not over.

Please take a moment to watch Mish's latest media clips where she outlines the macro down to the micro. We also invite you to become a MarketGauge subscriber for more regular analysis. You can sign up for a free consultation with Rob Quinn, our Chief Strategy Consultant, by clicking here. He'll help you learn more about my top-rated risk management trading service.

Mish's Upcoming Seminars

ChartCon 2022: October 7-8th, Seattle (FULLY VIRTUAL EVENT). Join me and 16 other elite market experts for live trading rooms, fireside chats, and panel discussions. Learn more here.

The Money Show: Join me and many wonderful speakers at the Money Show in Orlando, beginning October 30th running thru November 1st; spend Halloween with us!

Get your copy of Plant Your Money Tree: A Guide to Growing Your Wealth and a special bonus here. Get your copy of Plant Your Money Tree: A Guide to Growing Your Wealth and a special bonus here.

Follow Mish on Twitter @marketminute for stock picks and more. Follow Mish on Instagram (mishschneider) for daily morning videos. To see updated media clips, click here.

Mish in the Media

Mish talks hedges and stock picks under the current environment in this appearance on BNN Bloomberg.

Mish says yes to Palantir, no to Bed, Bath and Beyond in this appearance on CNBC Asia.

Mish talks about a few of her picks, going short and why metals are in focus in this appearance on TD Ameritrade.

Mish talks putting your cash to work in this appearance on Business First AM.

Mish and Neil Cavuto discuss Central Bank credibility, US policy and more inflation to come on Fox Business's Coast to Coast. Unless this is a spectacular bottom, preserving cash is smart.

Read Mish's latest article for CMC Markets, titled "When to Put Cash Back to Work".

Mish talks about key averages, yields and commodities on this appearance on Bloomberg TV.

ETF Summary

- S&P 500 (SPY): 353 support, 358 resistance.

- Russell 2000 (IWM): 162 support now, 168 resistance.

- Dow (DIA): 285 support, 289 resistance.

- Nasdaq (QQQ): 262 support, 268 resistance.

- KRE (Regional Banks): 57 support, 60 resistance.

- SMH (Semiconductors): 182 support, 188 resistance.

- IYT (Transportation): 194 support, 198 resistance.

- IBB (Biotechnology): 114 support, 119 resistance.

- XRT (Retail): 55.55 support, 58.56 resistance.

Mish Schneider

MarketGauge.com

Director of Trading Research and Education

Wade Dawson

MarketGauge.com

Portfolio Manager

|

| READ ONLINE → |

|

|

|

| Dancing with the Trend |

| Risk is More than a Four Letter Word |

| by Greg Morris |

Dictionary.com says: The exposure to the chance of injury or loss; a hazard or dangerous chance. American Heritage Dictionary says: The possibility of suffering harm or loss; danger. These are just two of the many entries and these were just for the noun. Risk in the world of investments and finance is more succinct. Risk is the uncertainty of outcome, however risk can be quantified whereas uncertainty cannot. Many use risk as a quantitative measure and uncertainty for measuring the non-quantitative type. This article will attempt to give an overview of risk, keeping to generalities, and identifying a few of the problems associated with trying to measure it. Moreover, without any equations. Dictionary.com says: The exposure to the chance of injury or loss; a hazard or dangerous chance. American Heritage Dictionary says: The possibility of suffering harm or loss; danger. These are just two of the many entries and these were just for the noun. Risk in the world of investments and finance is more succinct. Risk is the uncertainty of outcome, however risk can be quantified whereas uncertainty cannot. Many use risk as a quantitative measure and uncertainty for measuring the non-quantitative type. This article will attempt to give an overview of risk, keeping to generalities, and identifying a few of the problems associated with trying to measure it. Moreover, without any equations.

I frequently hear from investors who are concerned about performance. They want to know the performance over the last month, the last quarter, the last year, the last 5 years, etc. Rarely can I remember when one of them also asked about the risk associated with a money management style. Knowledge of performance without understanding the risk required to get that performance is worthless in most investment scenarios. Investors are generally aware of market risk, the risk you incur with exposure to securities whose prices move based upon movement of the forces of the overall market. Unfortunately, these investors were educated in a system that was essentially void of lessons on our credit or capital markets. They have been led to believe that market risk is just a "fact of life" when it comes to investing. I strongly believe differently. Performance without assessing the associated risk is not performance at all, but hope. Hope has its place in life, but not in investing.

Risk is measured in many different ways. You can open any mutual fund prospectus and read page after page of required documentation on numerous types of risk, such as: Interest Rate risk, Credit/Default risk, Call risk, Management risk, Liquidity risk, Sovereign risk, just to mention a few. Grab a prospectus sometime, you will be surprised! Awareness of these individual concerns is not nearly as important as the knowledge and understanding of accepting (requiring) performance on a risk-adjusted basis. These types of risk measures are attempts to quantify risk in such a way as to also know the bounds or extremes one may encounter. In a nutshell, risk measures are attempting to quantifying uncertainty.

Investments that carry more risk usually (but not always) offer higher returns, or I should say expected returns. That makes sense doesn't it? If you take more risk, you expect to be compensated for it. Therefore, the assessment of risk is an important element of successful investing. Risk measures are based on historical performance and from this we make our best estimates to what the risk will be in the future. It is the best measure of future risk and needs to be updated frequently knowing full well that the future is not predictable.

Peter Bernstein, author of "Capital Ideas" and many other good books on finance was asked, "What are investors' most common mistakes?" His answer was simple and straightforward: "Extrapolation. Leaving fund managers in a down year to go with whoever's hot." He went on to offer another tidbit of sound advice when asked how an investor could reduce risk, "The riskiest moment is when you are right. That's when you are in the most trouble, because you tend to overstay the good decisions." My short list of great books includes two by Peter Bernstein, "Against the Gods" and "Capital Ideas." Both are excellent reads and strongly recommended.

The world of finance is fraught with theories on how to control risk in one's portfolio. These theories, such as Capital Asset Pricing Model, Efficient Market Hypothesis, Random Walk, Options Pricing Model, etc., are a sound basis for all financial analysis. Personally, I think they are a little heavy in their assumptions and have stated such in previous articles, but one thing I really find at fault is their almost total belief that market risk can only be dealt with by diversification. Again, I do not believe this is the best way to handle market risk. I believe that when market risk reaches certain levels, one should take defensive action to prevent loss.

And finally, remember that the "world of modern finance" is entrenched in the belief that risk is measured by the variation of returns about their mean; or standard deviation. This is total nonsense because in order to use standard deviation you have completely accepted the belief that prices are random and normally distributed. They are not! That is unless you work in the confines of the sterile laboratory of modern finance, their ivory tower so to speak. And I will close with something I keep saying over and over; the beauty of the technical approach to investing is that you are dealing with systematic risk. That is the risk of bear markets and drawdown. Those "other" folks only deal with non-systematic risk or as it is also known - diversifiable risk. Think about it, how often do you read wire house (large brokerage firms) publications that constantly talk about diversification and rebalancing? And since I mentioned wire houses, keep in mind most if not all of their publications are for marketing purposes. It is hard to see that because they write so convincingly and what appears to be so logical; yet it is just there to make you feel they have your best interests at heart. If those "other" investors would ever wake up, they will sleep better.

Trade by knowing the risk,

Greg Morris

|

| READ ONLINE → |

|

|

|

| MORE ARTICLES → |

|