Bogle’s new book, Stay the Course, reveals one little thing individual investors do that costs them one-third of their return — but is easily prevented. • A difference between the trading of investors in traditional index mutual funds and that of investors in the flashier index exchange-traded funds (ETFs) explains a lot about the varying amounts both groups end up putting in their pockets.

• Part 1 of this column appeared on Jan. 15, 2019. •

John Clifton Bogle passed away on Jan. 16, 2019, four months shy of his 90th birthday. My hope is that, by understanding his last book and the travails he faced and overcame in his life, we will honor his memory. R.I.P., Jack. —BL

Despite being denied access to some of Vanguard’s historical documents, as Bogle says in Stay the Course, the famed founder of index funds was able to draw upon his vast first-hand knowledge to reveal some shocking facts about the investing business. These lessons can improve the returns of every investor.

One huge variation in trading profits relates to the difference in turnover by investors in index mutual funds and index ETFs. Using industry data, Bogle shows the following annual turnover rates:

18% — Vanguard mutual funds (he estimates an almost 6-year holding period)

135% — Vanguard ETFs (a 9-month holding period)

579% — Other ETFs (a 2-month holding period)

Bogle, of course, attributes the lower turnover in Vanguard’s own mutual funds and ETFs to the company’s emphasis on long-term investing rather than rapid trading. But he takes his analysis quite a bit farther than this.

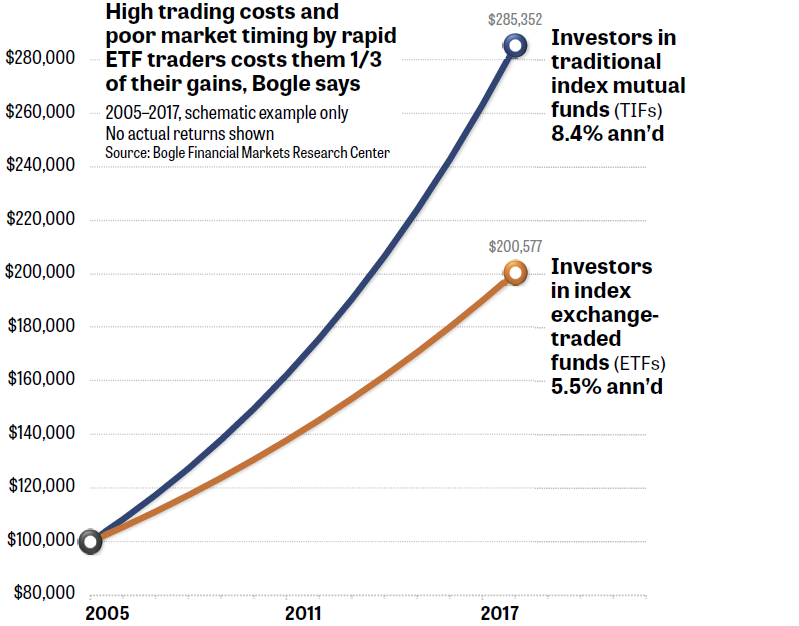

Figure 1, shown below, reflects Bogle’s calculation of the actual return to investors in similar equity vehicles that he calls “traditional index mutual funds (TIFs)” and index exchange-traded funds (ETFs). These are not the returns of the funds themselves. They are returns of the individual account holders, as Bogle calculates them from the money-flow data of Strategic Insight Simfund.

Figure 1. Holders of index ETFs trade them much more frequently than holders of similar index mutual funds. This costs the rapid traders about one-third of their possible gains, Bogle says.

Figure 1 shows the 13-year period from Jan. 1, 2005, through Dec. 31, 2017. (Vanguard, which pioneered index mutual funds, didn’t open its first ETF until 2001, as we shall see.)

The graph does not show historical returns from any actual funds or individual investors. Instead, I merely plotted two purely theoretical accounts that started with $100,000. I then compounded the mutual fund holders’ accounts using the rates of return that Bogle calculated from money-flow data. Actual historical returns, of course, would be characterized by jagged ups and downs.

In these 13 years, investors in equity index mutual funds compounded their money at an annualized rate of return of 8.4%. Investors in index ETFs compounded at 5.5% — only about two-thirds the rate. The mutual-fund owners turned $100,000 into $285,352. The ETF traders — so quick on the draw — ended up with only $200,577. Again, that’s about one-third less gain, although the difference would become greater as the years grow longer.

Despite how central these numbers are to Bogle’s message, I’ve never seen the difference in returns explained this clearly in any reviews of the book.

Does this mean individual investors should always buy mutual funds and never buy ETFs? Of course not!

Figure 1 simply points out — as Bogle puts it in Stay the Course — the “high trading costs, bad bets, and poor market timing” that afflict rapid traders. Limiting your trading in ETFs to no more often than once a month — less often, if possible — should eliminate these trading frictions and behavioral errors. (See my Muscular Portfolios summary for details.)

A loner in the very company he founded

Bogle’s dislike for the sheer idea of exchange-traded funds goes way, way back. Long before he saw the massive turnover that ETFs experience, he hated the rapid trading they allowed.

As we all know now, Vanguard invented the index mutual fund with Bogle’s launch of the First Index Investment Trust in December 1977. The fund tracked the S&P 500, a strange goal at the time and one that was derided by industry experts as “Bogle’s Folly.” It’s now called the Vanguard 500 Index Fund (symbol VFINX, which closed to new investors in November 2018, and VFIAX thereafter). The 500 Index Fund and the Total Stock Market Index Fund — the largest mutual fund in the world — together hold 30% of the assets Vanguard now manages.

Mutual funds, of course, can be bought or sold only once a day: at the 4 p.m. market close. ETFs were a completely different matter for Bogle.

He reveals in Stay the Course that he was the first person approached in early 1992 by Nathan Most, then a vice president of the American Stock Exchange (now NYSE American). “Most was clearly a missionary for his concept,” Bogle writes. The proposal was for Vanguard to copy its 500 Index Fund with an ETF version — the very first ETF. It would trade freely during market hours, provide its holders with tax advantages, allow lower costs than mutual funds, and enable buying on margin and selling short — just like a stock.

“I wasn’t interested,” Bogle told Most. “I feared that adding all that liquidity would attract largely short-horizon speculators whose trading would ill serve the interests of the fund’s long-term investors.”

Bogle didn’t mean liquidity — an ETF’s liquidity is based on the volume of its underlying assets, not the ETF’s own volume — he didn’t like the tradability of the new-fangled investment vehicle.

Well, other people liked exactly that trait of ETFs. Nathan Most went straight to Vanguard’s competition: State Stree Global Advisers. That company, now a giant financial firm, launched Standard & Poor’s Depository Receipts (SPDR or “Spider”) in January 1993. It’s now better known under the symbol SPY. It’s the world’s largest ETF — holding more than $300 billion — and represents more daily dollar volume than any other security on any of the world’s stock exchanges.

With the success of SPY, pressure mounted on Vanguard to offer its own low-cost ETFs. But Bogle firmly resisted. Bogle had stepped down as Vanguard CEO in January 1996. He was pressured off the board in 1999 by, among others, John Brennan, his own hand-picked new CEO, according to CNNMoney. But Bogle remained on the Vanguard campus and was active in the firm’s management. Burton Malkiel, who served on the Vanguard board for 28 years, later told the Philadelphia Inquirer:

“I would have been in favor of doing it earlier than we did. It was Vanguard’s management (not the board) that were reluctant. ... Jack Bogle in particular was very negative about the product [ETFs].”

Overcoming Bogle’s opposition, Vanguard launched its Total Stock Market ETF (VTI), covering literally thousands of US stocks, in 2001 — more than eight years after the introduction of SPY. It wasn’t until as recently as 2010 that Vanguard introduced an ETF that tracked the S&P 500, using the symbol VOO. (V is the Roman numeral for 5, and “oh oh” looks like zero zero, get it?) The delay to 2010 was due in part to Bogle’s resistance, and in part to Vanguard losing a court case against Standard & Poor’s. S&P sought two licensing fees: one for its name being used on Vanguard’s mutual fund and another one for its ETF.

The battles took their toll. The Boston Globe reported in 2003 that Bogle and Brennan were no longer on speaking terms. “They don’t talk to me,” Bogle was quoted as saying. “There is no communications. It is fine with me.”

The Philadelphia Business Journal, in a 2014 interview, came right out and asked Bogle what he thought about Brennan asking him in 1999 to step down from the Vanguard board. “I regret the fact that it remains difficult for me and the higher ups here,” Bogle replied. “They seem to be unconcerned about all of the good things I do. The books. The speeches. The public relations. But I do them anyway.”

ETFs remain one of the best inventions of the 20th century

Exchange-traded funds are now widely accepted and aren’t going away. This is because of their great advantages over mutual funds:

- Lower taxation. Mutual funds are required to report “phantom gains” (distributions) near the end of each year. No money is actually distributed but — in a taxable account — you must pay tax on the declared amounts, even if you never sold a single share. ETFs almost never report these illusory gains.

- No marketing fees. Some mutual funds charge front-end loads, redemption fees, or 12b-1 marketing fees, all of which can finance commissions for brokers. For example, one Vanguard mutual fund, the Long-Term Corporate Bond Index Fund (VLTCX), charges a 1% “purchase fee.” ETFs never charge any of these fees.

- No minimums. To cover their expenses, many mutual funds have a minimum buy-in dollar amount. Some Vanguard mutual funds, for instance, require at least $3,000 from individual investors. By contrast, novices with only enough dough to buy a single share of an ETF can get started in investing.

- Buy and sell whenever the market is open. You never know the price you paid for a mutual fund until hours after the market’s 4 p.m. close. Because ETFs trade during the day like stocks, you can check an ETF’s price at 3 p.m., make a buy or sell decision, and get your order filled before 4 p.m.

That last trait — easy tradability — is essential for gradual asset-rotation systems such as the ones in Muscular Portfolios, which require that you check your holdings once a month. (The asset-rotation portfolios in the book make a position change, on average, in only 9 out of 12 months a year.)

Rapid trading can seriously hurt your performance. But the ability to periodically upgrade your holdings away from ETFs that are lagging and into ETFs that are rising improves your long-term performance a great deal.

In the next part of this column, we’ll see even more secrets Bogle reveals in his last book ever.

• Parts 3 and 4 appear on Jan. 22 and 24, 2019.

With great knowledge comes great responsibility.

—Brian Livingston

Send story ideas to MaxGaines “at” BrianLivingston.com