Market Recap for Tuesday, March 13, 2018

It appears to be a case of "too much of a good thing". Technology stocks (XLK, -1.15%) retreated off of a 60 minute negative divergence and that reverberated throughout most parts of the NASDAQ (-1.02%), which led our major indices lower on Tuesday. Internet stocks ($DJUSNS, -1.99%) were unable to keep up with software ($DJUSSW), semiconductors ($DJUSSC) and computer hardware ($DJUSCR) - all of which broke out to fresh new highs this week. The DJUSNS backed down just as it approached overhead price and gap resistance:

Price momentum is strengthening in the DJUSNS, but it'll need to clear 1765-1770 on a closing basis to confirm its next breakout. In the meantime, I'd look to the rising 20 day EMA as key short-term support on any further weakness.

Price momentum is strengthening in the DJUSNS, but it'll need to clear 1765-1770 on a closing basis to confirm its next breakout. In the meantime, I'd look to the rising 20 day EMA as key short-term support on any further weakness.

Technology, along with both the NASDAQ and Russell 2000, ran into problems early yesterday when their price highs were not met with accompanying PPO highs. This resulted in a negative divergence and could lead to additional near-term weakness or sideways consolidation to allow price to meet 50 hour SMA support. Here's what to watch for:

The pink arrows highlight potential PPO centerline and 50 hour SMA tests, which are typical destinations after negative divergences print. While the overall market is much healthier now than it's been at any point over the past several weeks, I wouldn't be surprised to see technology take a back seat to other areas of the market in the very near-term. A breakout above Tuesday's high would help to negate the scenario described above.

The pink arrows highlight potential PPO centerline and 50 hour SMA tests, which are typical destinations after negative divergences print. While the overall market is much healthier now than it's been at any point over the past several weeks, I wouldn't be surprised to see technology take a back seat to other areas of the market in the very near-term. A breakout above Tuesday's high would help to negate the scenario described above.

The February CPI report was released prior to the stock market opening on Tuesday and that report showed that inflation is not a problem at the consumer level. That helped to alleviate inflationary fears and was a catalyst for the early morning market strength. Keep in mind that the Friday jobs report showed that wage inflation was under control so the consumer price index (CPI) was icing on the cake for the bulls.

Pre-Market Action

The 10 year treasury yield ($TNX) is mostly flat and continues to consolidate in a 2.80%-2.95% range after a dovish February CPI report was released Tuesday morning. Meanwhile, most Asian markets were fractionally lower overnight. In Europe this morning, most indices are green and that strength seems to be carrying over into pre-market action here in the U.S. Dow Jones futures are higher by 85 points with an hour to go before today's opening bell.

Current Outlook

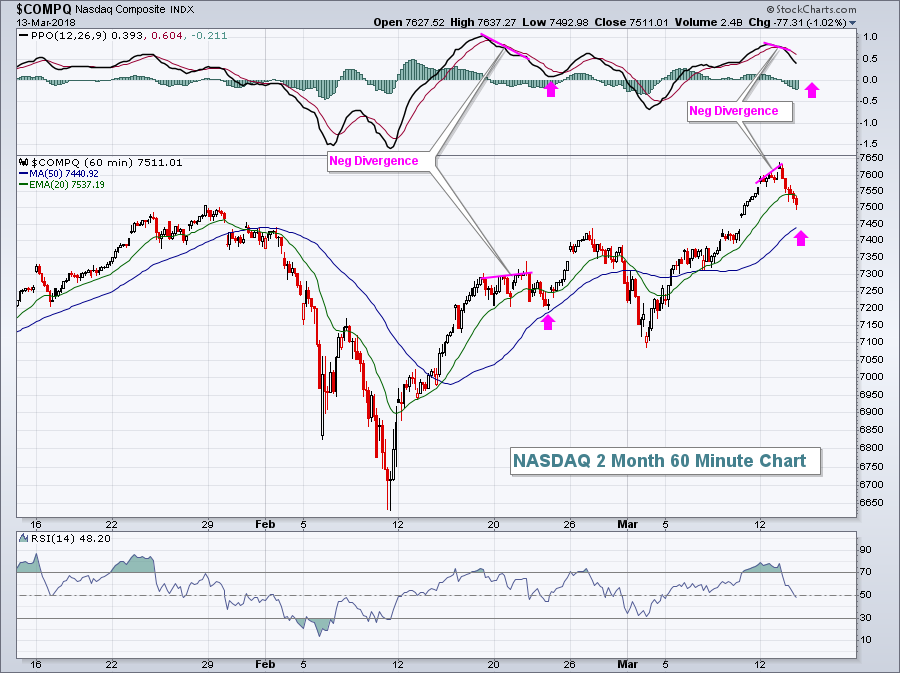

I mentioned the 60 minute divergence present on the XLK above in the Market Recap section. Well, there's one on the NASDAQ Composite as well and that could hinder progress in the near-term:

While this 60 minute negative divergence wouldn't have me running around screaming "Bear Market!", it does give me reason to pause and consider perhaps a bit of upcoming selling/consolidation. It's a definite risk, just as the negative divergence three weeks ago led to a bit of short-term weakness. After all, the NASDAQ just ran 550 points higher in the last 10 days. It's entitled to a pause.

While this 60 minute negative divergence wouldn't have me running around screaming "Bear Market!", it does give me reason to pause and consider perhaps a bit of upcoming selling/consolidation. It's a definite risk, just as the negative divergence three weeks ago led to a bit of short-term weakness. After all, the NASDAQ just ran 550 points higher in the last 10 days. It's entitled to a pause.

Sector/Industry Watch

Food retailers & wholesalers ($DJUSFD) are struggling to hang onto price and gap support as can be seen below:

The DJUSFD is an industry group within the consumer staples space (XLP) and helps to illustrate how badly this sector has underperformed throughout the market's recovery phase. Of course, underperformance in defensive areas is exactly what you want to see if you're bullish. But you also want to see wide participation so look for the DJUSFD to continue to hang onto its gap support zone from 347-357.

The DJUSFD is an industry group within the consumer staples space (XLP) and helps to illustrate how badly this sector has underperformed throughout the market's recovery phase. Of course, underperformance in defensive areas is exactly what you want to see if you're bullish. But you also want to see wide participation so look for the DJUSFD to continue to hang onto its gap support zone from 347-357.

Historical Tendencies

The NASDAQ has been hot, breaking out to fresh all-time highs in recent days. Let's look at the current month, April and May for seasonal expectations:

March: +9.36% (ranks 7th among all calendar months)

April: +17.39% (ranks 4th)

May: +10.88% (ranks 5th)

The above numbers reflect the NASDAQ's monthly gains (annualized) since 1971. While the next couple months aren't the best, they certainly aren't the worst either. Given current bullish technical conditions, I expect we'll see more highs on the NASDAQ over the next couple months prior to the seasonally difficult summer months.

Key Earnings Reports

None

Key Economic Reports

February PPI released at 8:30am EST: +0.2% (actual) vs. +0.2% (estimate)

February Core PPI released at 8:30am EST: +0.2% (actual) vs. +0.2% (estimate)

February retail sales released at 8:30am EST: -0.1% (actual) vs. +0.4% (estimate)

February retail sales less autos released at 8:30am EST: +0.2% (actual) vs. +0.4% (estimate)

January business inventories to be released at 10:00am EST: +0.5% (estimate)

Happy trading!

Tom