Literally hundreds of millions of dollars are spent each year on the analysis of individual securities by Wall Street brokerage firms and independent firms (Zacks, Hoovers, Value Line, etc). Most brokerage firms have a large staff of analysts, which make huge salaries, and are widely summoned to television shows each day for their opinions based upon their research. Most will focus on a single industry so that their expertise will not be diluted; they are specialized, they are considered experts. In fact, most of what makes up daytime financial television are the interviews of these analysts, and of course, the never-biased (TIC) CEOs of the companies.

Literally hundreds of millions of dollars are spent each year on the analysis of individual securities by Wall Street brokerage firms and independent firms (Zacks, Hoovers, Value Line, etc). Most brokerage firms have a large staff of analysts, which make huge salaries, and are widely summoned to television shows each day for their opinions based upon their research. Most will focus on a single industry so that their expertise will not be diluted; they are specialized, they are considered experts. In fact, most of what makes up daytime financial television are the interviews of these analysts, and of course, the never-biased (TIC) CEOs of the companies.

One of the major components of their analysis resides with what we know as “multiples.” “Multiples” refers to the fundamental ratios that govern how a company is doing financially. There are many of these ratios, such as: Price to Earnings, Price to Book, Price to Dividend, Cash to Price Percentage, Working Capital to Price, Earnings to Book, Net Assets to Price, Price to Sales, on and on. The purpose of using multiples is so one can compare one company against others using a common measuring stick. This is the heart and soul of what is known as fundamental analysis. Fundamental analysis is big stuff; go to any brokerage website, type in a stock symbol, and you will be inundated with beautiful color multi-page reports discussing the potential of the stock and the analysts’ current rating. The first hint of a real problem is that they all use different terminology to describe their ratings, such as: overweight, equal weight, neutral, underweight, etc. They don’t give you the more desirable buy, sell, or hold anymore. This new terminology gives them the ability to mask what they mean behind various types of valuation methods.

So what’s the problem? Most fundamental ratios (multiples) use price or a derivative of price in their calculation. Because of this, as the price of a stock changes constantly, and the financial reporting is usually only quarterly, these ratios can be better or worse just based upon the movement of the stock’s price. So why not just analyze price? Bingo! And that is what technical analysis is primarily all about.

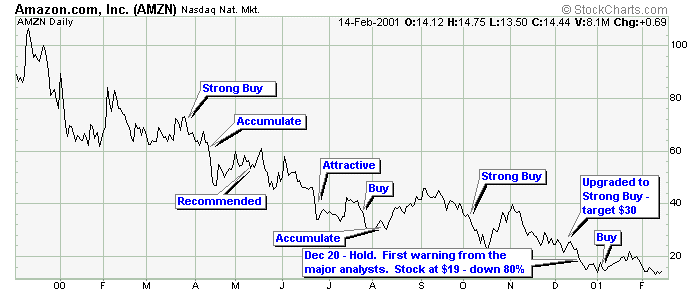

Do you remember Enron and its downfall in 2001? If you followed the Wall Street analysts you would have never realized there was a problem – all the way down until the stock became worthless, the majority of the analysts described what a great opportunity it was to buy the stock. The following chart shows the price of Amazon’s stock and the analysts’ calls. Not overly impressive is it? Notice how the fundamentally impaired continually recommended it – all the way down?

Chart A

Chart A

For the past few weeks, the market has seen a significant decline. I swear, if I hear another expert on television say this is a buying opportunity or hold the course because the market goes up in the long run, I think I’ll... The ever bullish Wall Street only wants you to sell when they have something else for you to buy (or sell to you). The large wire houses produce truckloads of fundamental research for their clients – trust me, it is just marketing and of no value. Marketing disguised as research is sinful. Stick to technical analysis, the analysis of price, which an instantaneous view of supply and demand. Remember earnings are reported quarterly and prices can plummet daily. Wow, that sounded almost like a rant!

Finally, is there anything good about fundamental analysis? Sure, if it makes you feel better to buy stocks that have good multiples, do so, but use technical analysis to determine when to buy and sell them based upon risk and reward. Another way is to use fundamentals to narrow the field of issues you wish to analyze technically. Let the market tell you what is going on and act accordingly.

Trade technically,

Greg Morris