Webster defines Odds and Ends as different kinds of things that are usually small and unimportant. I would prefer to define them as sort of important. I’ll use this format for issues that I cannot justify an entire article on. So expect Odds and Ends II at some point.

Webster defines Odds and Ends as different kinds of things that are usually small and unimportant. I would prefer to define them as sort of important. I’ll use this format for issues that I cannot justify an entire article on. So expect Odds and Ends II at some point.

Mutual Funds

If you buy a mutual fund you are not buying a money manager, you are buying an objective manager. Let me explain. Many, if not most will choose a mutual fund based upon its performance over a period of time or the victim of exceptional marketing. Too often I think the period of performance is void of bear markets such as the last 7 years. This does not give a valid representation of the fund’s performance over the long run. The fund rating companies show 3-year, 5-year, 10-year, and since inception or at least close to those. Many funds have only been in existence much less than the 10-year time period. Okay, I drifted off subject.

Let’s say you have been told that aggressive growth is where to put your money. You do a due diligence search for the best aggressive growth mutual fund and find one that does really well and has been in existence for 6 years. As long as the market is rising and aggressive growth stocks are rising with it, you believe you are a master fund picker. Then a bear market begins. Your fund NAV (Net Asset Value) drops and drops and after a year or so you are down 45%. You get angry and call the fund manager all sorts of names. In fact, you should look in the mirror and direct your anger at the reflection. It was YOU who picked an aggressive growth mutual fund. The fund manager is required by law to maintain the objective. In fact, he/she is required to keep 80% of the fund’s assets in aggressive growth stocks. I can assure you he/she was only doing what you expected them to do – be in aggressive growth stocks – period.

I would suggest finding mutual funds that are actively managed and in particular those who treat cash as an asset class.

Sometimes It Just Depends on When you were Born

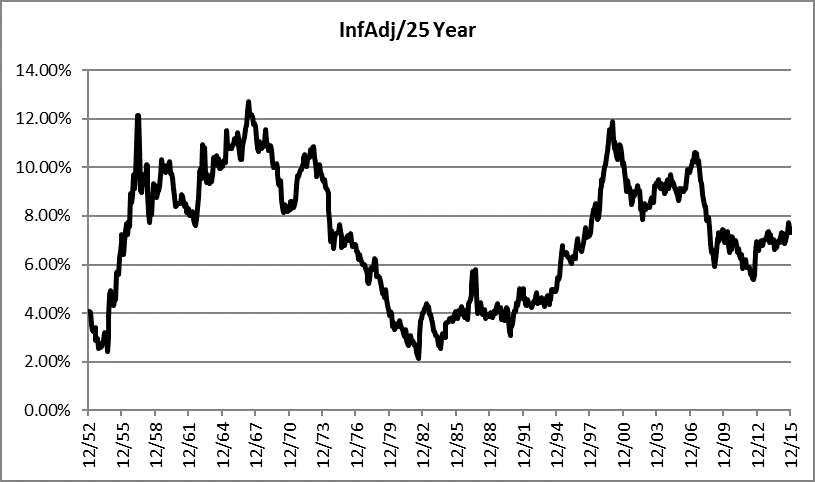

I have been on record for years stating that most investors do not really get serious about socking money away for retirement until they are in their forties. I know this is a generalized statement and I have no data to support it, but if you think about it, it probably makes sense. In your twenties and thirties, with a new house, kids, educations, and the materialistic expensive car, it is fairly hard to put much away. Once you settle down, better job, empty nest, then it becomes easier. Modern finance, the marketing department for Wall Street likes to show you a 125-year chart of the market returns and tell you it averages 8% a year. I say, there are many 20-25 year periods where the average returns were considerably less.

Chart A shows a 25-year rolling return of the S&P 500 Total Return adjusted for inflation since 1928. Let me explain rolling returns, in this case annualized. Take the peak point at approximately 12/00 which is in the year 2000. The value is at 12%, which means the previous 25 years have returned 12% annualized. Nice! Now look at the low point at about 12/82, which is at 2%. Holy Cow! Big difference! The poor guy who turned 65 in 1982 and was minimally capitalized for retirement, expecting the promised 8% a year is now a Walmart greeter. The last data point is the end of 2015 at 7.72%. So, if you have the misfortune of being born such that at age 65 you are at the beginning of a poor quarter century of performance, just blame your parents. That was purely tongue in cheek – you are to blame if you are a buy and hold investor or index investor.

Chart A

Chart A

Dance with the Trend,

Greg Morris