The significant components of my Weight of the Evidence are Price Measures and Breadth Measures. All of my Price Measures use the Nasdaq Composite Index which I have written about many times. If using the same price, then the difference between most price indicators is to offer varying time periods; short, medium, and long. Breadth on the other hand, can offer many different indicators of trend. Price is just price; but breadth is advances, declines, advancing volume, declining volume, new highs, and new lows. Those are what I call internal market breadth. There are other breadth measures that are not internal, such as percent of stocks above a moving average, bullish percent (involves point and figure), and Participation measures. Sales Pitch to follow: I completely updated my “The Complete Guide to Market Breadth Indicators” a few years ago and ALL of those indicators are now part of StockCharts.com’s Symbol Catalog (they all begin with !BI). There is also a StockCharts.com ChartPack with all of them included and is automatically updated as the new data is available. End of Sales Pitch. Before we dive into the Weight of the Evidence indicators there are a couple of clean-up items I need to discuss.

The significant components of my Weight of the Evidence are Price Measures and Breadth Measures. All of my Price Measures use the Nasdaq Composite Index which I have written about many times. If using the same price, then the difference between most price indicators is to offer varying time periods; short, medium, and long. Breadth on the other hand, can offer many different indicators of trend. Price is just price; but breadth is advances, declines, advancing volume, declining volume, new highs, and new lows. Those are what I call internal market breadth. There are other breadth measures that are not internal, such as percent of stocks above a moving average, bullish percent (involves point and figure), and Participation measures. Sales Pitch to follow: I completely updated my “The Complete Guide to Market Breadth Indicators” a few years ago and ALL of those indicators are now part of StockCharts.com’s Symbol Catalog (they all begin with !BI). There is also a StockCharts.com ChartPack with all of them included and is automatically updated as the new data is available. End of Sales Pitch. Before we dive into the Weight of the Evidence indicators there are a couple of clean-up items I need to discuss.

Indicator Evaluation Periods

I have never just accepted an indicator’s value; I always had to prove it using my techniques. Sometimes, in the old days, that meant pouring over printed charts - slowly. Often taking days, if not weeks. Indicators need to be evaluated over cyclical bull and bear markets, secular markets, periods covering calendar-based times, randomly selected periods, and almost any other period selection process you want to try. I truly hate to even mention calendar-based but that is what Wall Street functions on, so why fight it. Remember, the goal is to find parameters (the variables in the indicator) that meet the needs of the model you are trying to create. An example of an indicator parameter is when you select 21 periods for a moving average. Twenty-one (21) is the parameter since you can select any amount you want. You want indicators whose statistics over various times provide the safety and return that you expect of them. Ideally, you want to test the indicators with a certain portion of your data, get the parameters that work well, and then check it on the remaining portion of your data. This is known as in sample and out of sample testing. If the indicator continues to perform on the previously unused data, then you probably have something of value.

Here is a partial list of indicator evaluation measures you should consider:

Winning Years

Trades per Year

Average Return per Trade

Total Return

Compounded Annual Return

Compounded Annual Return while Invested

Percentage of Time Invested

Largest Trade Loss

Maximum Drawdown

Ulcer Index or other Risk Measure

When we address Price-based indicators I will show you a table of those measures along with the data. Notice the item based upon "while invested." Modern finance and Wall Street have no idea what I'm talking about; they never consider cash or a cash equivalent as an asset class. I do.

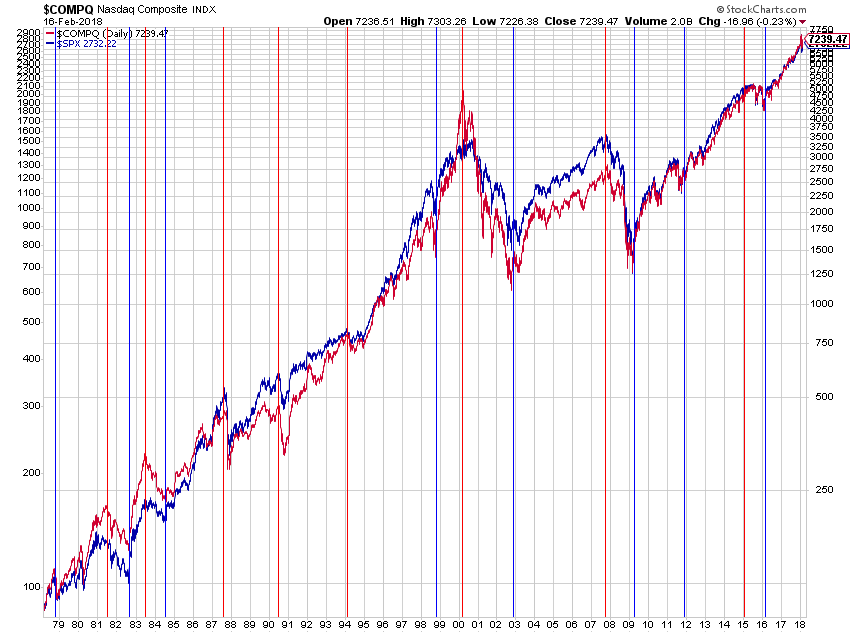

Chart A shows the Nasdaq Composite Average and the S&P 500 Index. The vertical lines are placed at each low and high that can be used to determine the evaluation periods. You must be careful with this and include the significant peaks and troughs when viewed over the long-term. In fact, using a weekly price chart is probably better for this than using a daily price chart. Additionally, plotting the data in semi-log format will let you see the peaks and troughs better.

Chart A

Chart A

A Warning about Optimization

When evaluating indicators to be considered for trend following, you cannot optimize over long-term periods and then just pick the best performing indicator. That is a guarantee of failure and probably quite soon. Optimization is a great process in which to discover areas to avoid, but a poor process to actually determine parameters. If you try to optimize then please read some good book on the downfalls of doing so. Optimization in the wrong hands is extremely dangerous. One area of value is to plot all of parameter’s performance and look for plateaus where the parameter performed steadily over a range of similar values. Picking a spike in the performance values is the worst thing you can do as the parameters surrounding the spike are probably closer to where you will see the actual results.

I have to say this again! Make perfectly certain you understand the downside of optimization. I see too many who get excited about optimized results and after trying it with real money find that the result does not give a clear indication of the path it took to get there. In fact, Perry Kaufman, created an indicator a few decades ago called Efficiency Ratio. I use it in my ETF Ranking and Selection process. It basically measures the straight-line distance between two time periods and compares it to the path the price (in my case, the ETF) takes. The shorter the path, the more efficient it is. Finally, the true benefit of correct optimization is getting you into the ball park for parameter sizing.

The next article in this series will be about price-based indicators.

Dance with the Trend,

Greg Morris