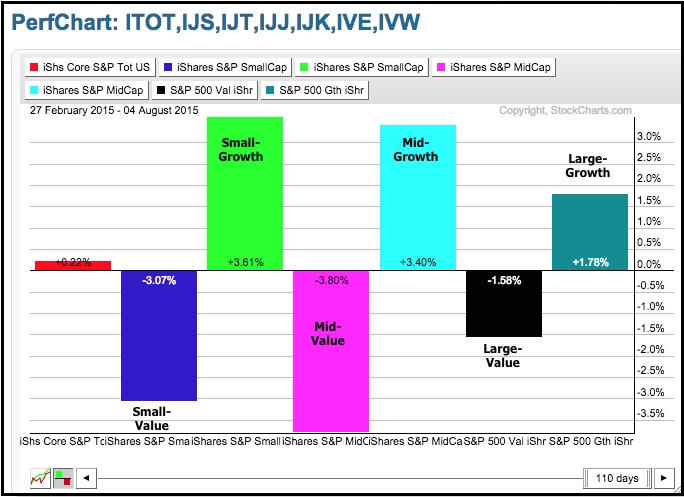

The S&P 1500 can be divided into the S&P 500, S&P MidCap 400 and the S&P SmallCap 600. These three ETFs can be further divided into their growth and value components to create six different index styles (small-growth, small-value, mid-growth, mid-value, large-growth, large-value). It is usually preferable to see growth leading value because the growth end of the market represents stocks with higher risk. Growth stocks typically have higher PE ratios, higher Betas and more volatility. The market favors risk over safety when growth is leading value and this is net positive for the stock market. The chart below shows three growth-value pairings and all three are in uptrends. The IJT:IJS ratio has been trending up since January and took off in early May as small-growth outperformed small-value. The IJK:IJJ ratio stalled out in April-May and then took off in mid June as mid-growth outperformed mid-value. The IVE:IVW ratio also took off in mid June as large-growth outperformed large-value. I will show a Perfchart and a sector break down after the jump.

The PerfChart below shows the performance for the three growth-value pairs since February 27th, which is when the trading range started for the S&P 500. These are clearly split with all three growth ETFs showing gains and all three value ETFs sporting losses. In an interesting twist, notice that large-value is down less than mid-value and small-value, and this shows relative strength. However, large-growth is up less than small-growth and mid-growth, and this shows relative weakness. Regardless, the market split is obvious.

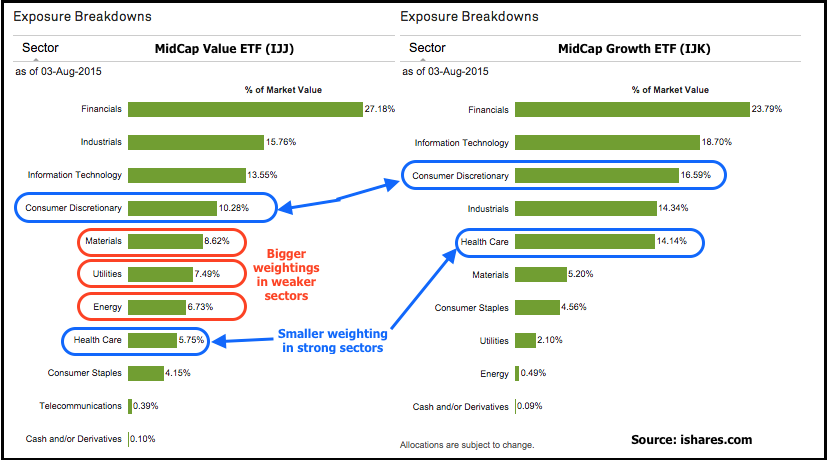

So why is growth outperforming value? The usual sector suspects are to blame (energy and materials). The image below shows the sector weightings for the S&P MidCap Value iShares (IJJ) and the S&P MidCap Growth iShares (IJK). It appears that the sector weightings are weighting on midcap value. Notice that the materials, utilities and energy sectors have much higher weightings in the midcap value ETF. These are three of four weakest sectors in the market (industrials is the fourth). In addition, the consumer discretionary and healthcare sectors have lower weightings. These are two of the three strongest sectors in the market (finance is the third).