One look at the 10 year treasury yield's ($TNX) decline the past several months provides proof that the bond market isn't exactly agreeing with the Federal Reserve's stated position that they see economic improvement in the months ahead. The Fed announced on Wednesday that it sees another rate hike in 2017 and further hikes in 2018. That would suggest a strengthening economy. Yet a strengthening economy should trigger the selling of treasuries and higher treasury yields. But that has not been the case. Who's right, the Fed or the bond market?

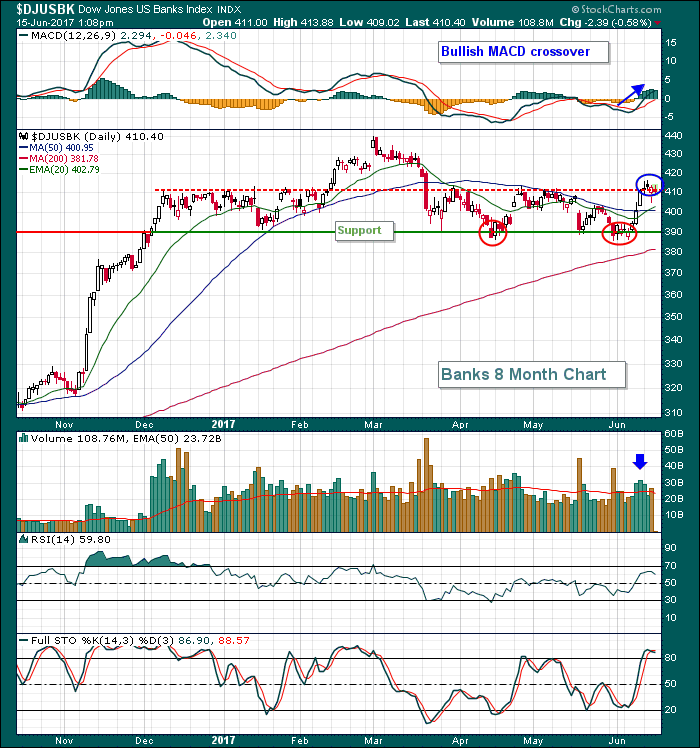

During all this "debate", the Dow Jones U.S. Bank Index ($DJUSBK) simply hasn't been able to make up its collective mind if rates are heading higher or lower. Normally, higher rates favor a strengthening banking group as net interest margins, the primary driver for banks, tend to expand in a rising interest rate environment. A declining interest rate environment has the opposite and negative effect on banks. The chart on the DJUSBK is very interesting as we have seen several false breakouts and breakdowns in recent months as traders cannot accurately predict which way treasury yields are heading. Here's the chart:

The two red circles show what appeared to be breakdowns beneath 390 price and neckline support, only to see the banks recover. The blue circle highlights the recent breakout above 410 shoulder resistance, only to see price action close on Wednesday back beneath that 410 level. What gives?

The two red circles show what appeared to be breakdowns beneath 390 price and neckline support, only to see the banks recover. The blue circle highlights the recent breakout above 410 shoulder resistance, only to see price action close on Wednesday back beneath that 410 level. What gives?

Well, I'm going to give the benefit of the doubt to the bulls here. Volume has been expanding and momentum is strengthening. But don't go blindly running into bank stocks. Watch the TNX. Banks need the tailwinds that higher treasury yields offer. So if the TNX turns back lower off the past couple sessions' uptrend, all bullish bets are off for the banks.

Happy trading!

Tom