In yet another fairly eventful week, the Indian equity markets continued to digest the general elections fully, ending with a violent reaction to the portfolio allocation of the new set of cabinet ministers. After witnessing a 420-point trading range while marking incremental highs on a closing basis, the headline index NIFTY ended with net gains of 78.70 points (+0.66%) on the weekly note.

The markets also ended the month while reacting to every possible event. The difference between the high and the low in the month of May was 932.85 points, which speaks of the amount of volatility the NIFTY saw in May. Despite such a broad trading range, the NIFTY ended May with net gains of just 174.65 points (+1.49%) on a monthly note.

As we approach the next trading week, it's essential to note that we have reached a point where the markets have finished reacting to the election and are done digesting all the events. We have arrived at a point where the markets are now set to react to the broader technical setup and macroeconomic environment along with other global factors.

A tepid start to the week is likely, as the levels of 12040 are set to act as a stiff resistance point for NIFTY. Beyond this, the NIFTY will enter uncharted territory and may find resistance at 12200. On the lower side, supports come in at 11800 and 11610.

The weekly RSI stands at 64.4315 and continues to show bearish divergence against the price. The weekly MACD remains bullish while trading above its signal line; however, it can be seen flattening its trajectory.

While the pattern analysis shows that the NIFTY halted its up move following a half-hearted attempt to break out at a double top resistance point, it also shows the index meeting resistance at the lower trend line of the upward channel that it breached earlier in October 2018.

The Bollinger bands show that the upsides, if any, may have limited potential. The recent price action around the bands, compared to the movement of the Relative Strength Index (RSI), suggests that a possible (short-)selling opportunity may exist. Prices have recently peaked above the upper band. This action was followed by a selloff, then by another peak inside the bands. The RSI has diverged from this price action with successive lower peaks, suggesting weakness ahead.

We also expect some volatility to resurface during the coming week. The markets face technical headwinds at higher levels. We strongly recommend not using dips blindly to make aggressive purchases. A greatly selective and stock-specific approach is advised for the coming week.

Sector Analysis for the Coming Week

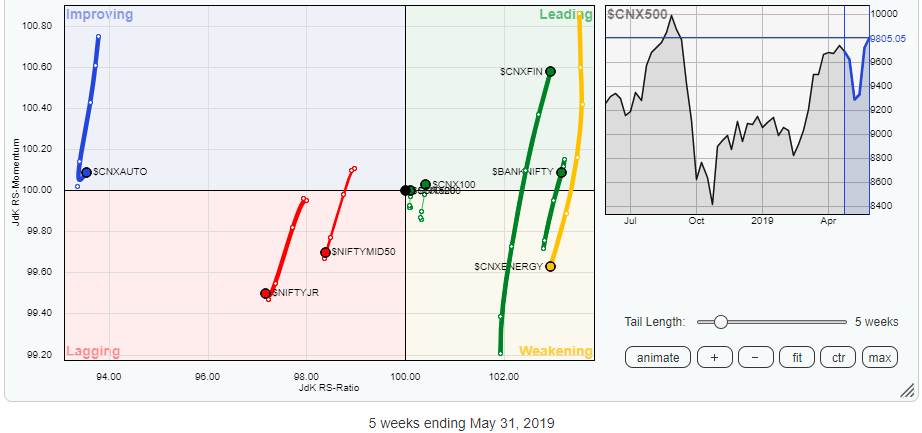

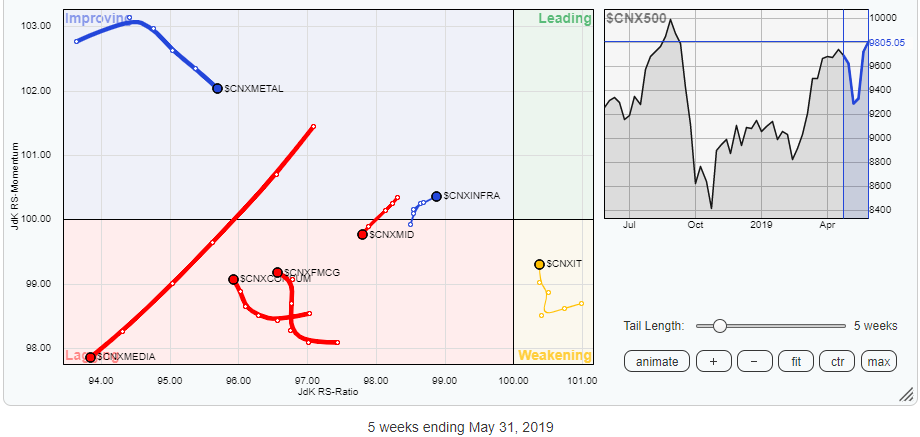

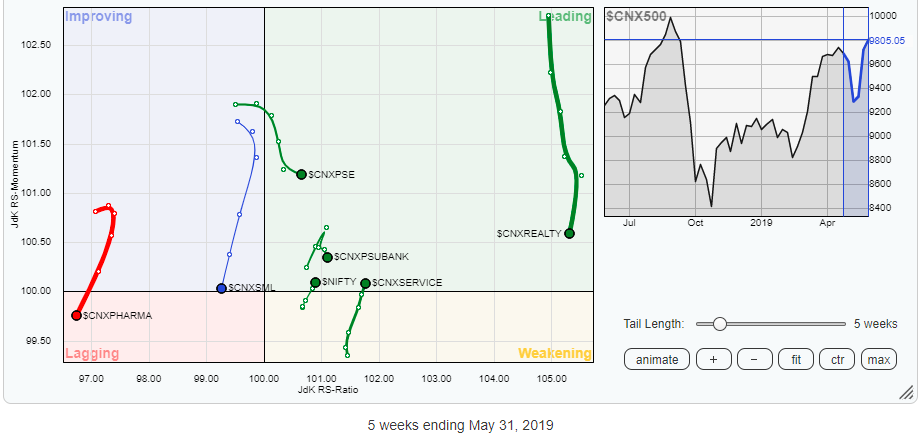

In our look at Relative Rotation Graphs, we compared various sectors against CNX500, which represents over 95% of the free float market cap of all the stocks listed.

Our review of Relative Rotation Graphs (RRG) shows the outperformance against the broader markets is likely to remain limited to specific sectors only. The Financial Services and Service Sector index are expected to relatively out-perform. The Infra pack is also expected to put up a resilient performance.

Our review of Relative Rotation Graphs (RRG) shows the outperformance against the broader markets is likely to remain limited to specific sectors only. The Financial Services and Service Sector index are expected to relatively out-perform. The Infra pack is also expected to put up a resilient performance.

The Bank NIFTY, Realty, PSU Banks, Energy, Pharma and Auto indexes are steadily losing momentum against the broader CNX500 index. Some stock-specific performance from the IT pack can be expected.

Along with the Financial pack, the CNXPSE index is likely to put up a resilient show as well, as it remains placed in the leading quadrant while consolidating its position.

Important Note: RRG™ charts show you the relative strength and momentum for a group of stocks. In the above chart, they show relative performance as against the NIFTY500 Index (Broader Markets) and should not be used directly as buy or sell signals.

Milan Vaishnav, CMT, MSTA

Consulting Technical Analyst

www.EquityResearch.asia