One of the most widely marketed recommendations for individual investors is the ‘Bucket Portfolio,’ developed by Morningstar Inc. This strategy generally underperforms the market — but if you make one simple change, as I reveal in this column, the annualized return jumps by more than 3½ percentage points. That’s huge! It would DOUBLE the gain in your portfolio within a few years: a great benefit for a working career or a comfortable retirement.

As I’ve written elsewhere, more than 100 million households in English-speaking countries alone — the US, UK, Canada, etc. — have money in 401(k), IRA, and other tax-deferred investment accounts. Unfortunately, the vast majority of 401(k) account owners have no way to buy stocks. These people are forced to be long-term traders. Most account holders are limited to the mutual funds offered by their 401(k) plan provider. Also, they are permitted to change their positions no more than once or twice a month. For details, see my Muscular Portfolios summary.

As I’ve written elsewhere, more than 100 million households in English-speaking countries alone — the US, UK, Canada, etc. — have money in 401(k), IRA, and other tax-deferred investment accounts. Unfortunately, the vast majority of 401(k) account owners have no way to buy stocks. These people are forced to be long-term traders. Most account holders are limited to the mutual funds offered by their 401(k) plan provider. Also, they are permitted to change their positions no more than once or twice a month. For details, see my Muscular Portfolios summary.

My columns are dedicated to these 100 million households. The good news is that there are easy ways to enjoy handsome, market-beating returns by trading only once a month, even when your selection of investment choices is limited.

Financial strategies like the Bucket Portfolio are designed to appeal to people who have no trading experience. Fortunately, a simple tweak — an example of long-term trading — makes a gigantic difference in the return of the Bucket Portfolio and other “Lazy Portfolios” like it.

We’ll use the Bucket Portfolio to illustrate profitable long-term trading methods in this four-part column:

- How Lazy Portfolios like Morningstar’s are constructed.

- What one simple step does to improve the Bucket Portfolio by 3.7 percentage points a year.

- How the change not only doubles the portfolio’s 28-year gain but also lowers its losses.

- Better strategies than the Bucket Portfolio, which is not ideally suited for maximum gains.

The Bucket Portfolio is a distinctive feature of Morningstar

The huge investment advisory firm has more than 5,000 employees and operates offices in 27 countries. The “Aggressive Retirement Bucket Portfolio” leads Morningstar’s model portfolios page. It’s presented to consumer gatherings several times a year by the firm’s director of personal finance, Christine Benz. The company’s strategy that I describe here is based on Morningstar’s aggressive retirement portfolio page as well as interviews I conducted with Benz in person and by phone (more on that in a later part of this column).

Like every Lazy Portfolio — a passive investment strategy, some examples of which have been tracked for more than 15 years on MarketWatch’s Lazy Portfolios page — the Bucket Portfolio contains a range of “asset classes,” including both US and non-US securities. Morningstar’s variation of a Lazy Portfolio holds nine asset classes in specific percentages. A long-term trader might execute this strategy using mutual funds or ETFs, which are listed on Morningstar’s portfolio pages. (The list of ETFs is behind a paywall. However, many libraries have a Morningstar subscription that allow you to access the page for free on a laptop. The example shown below uses mutual funds as investment vehicles.)

Unfortunately, the Bucket Portfolio, like other passive strategies, never changes the percentages allocated to its nine different securities. This static restriction prevents the portfolio from tilting toward assets that are in uptrends. Even worse, the portfolio heads straight into severe crashes whenever the world’s equity markets are collapsing.

The anatomy of a static asset allocation portfolio

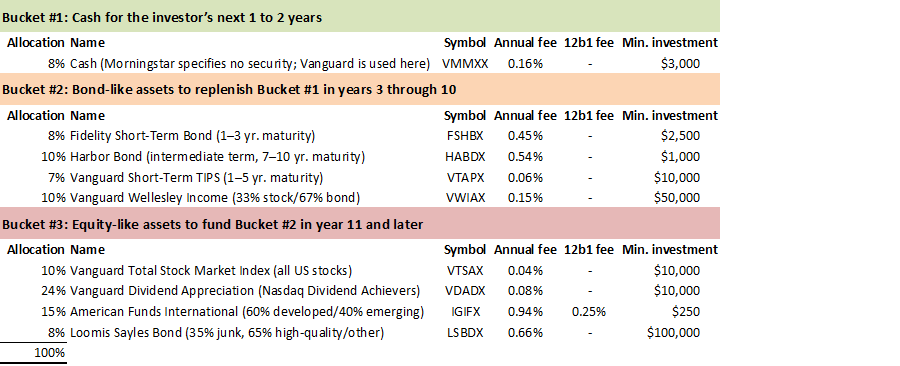

The following table shows the nine asset classes in the Bucket Portfolio, along with some of the mutual funds Morningstar recommends. Caution: The firm periodically changes the specified funds and even the asset classes themselves. For example, a commodities fund (GCC) was formerly allocated 5% of the portfolio, but was eliminated two years ago. The table below reflects Morningstar’s recommended funds as of Nov. 5, 2018:

Account owners are advised by Morningstar to hold three different categories of securities — cash, bond-like assets, and equity-like assets — in three mental “buckets.” Most importantly, investors are told Bucket #1 should contain approximately 8% of their total wealth in cash. (This could be a money-market fund, such as Vanguard’s VMMXX.)

Account owners are advised by Morningstar to hold three different categories of securities — cash, bond-like assets, and equity-like assets — in three mental “buckets.” Most importantly, investors are told Bucket #1 should contain approximately 8% of their total wealth in cash. (This could be a money-market fund, such as Vanguard’s VMMXX.)

Why 8%? Benz herself acknowledges that a cash allocation this large is a drag on the portfolio’s performance. However, it’s there to reassure skittish investors, especially those already in retirement and making withdrawals to live on. They would see that they have enough cash for two years’ worth of living expenses — 8% or some other percentage, depending on their situation — whenever the equity market is down or crashing. This cash cushion supposedly prevents the account owner from “throwing in the towel” and liquidating the stock portion of the portfolio at a loss. We’ll examine whether or not this actually works, later in this analysis.

Parts 2, 3, and 4 of this column appear on Nov. 8, 13, and 15, 2018.

With great knowledge comes great responsibility.

—Brian Livingston

Send story ideas to MaxGaines “at” BrianLivingston.com