A complete set of ETFs covering all major world markets has been available to US investors for years. But what if your money isn’t in US dollars? • In the country where you now live — or one you may move to when you retire — your savings may be denominated in Canadian dollars, UK pounds, or some other currency. You can still tailor a menu of global ETFs to meet your needs.

Figure 1. Investors who live in Canada, for example, may prefer to have their portfolio gains denominated in Canadian dollars to avoid the risk that the US dollar will move against them and cut into their returns. The same concern affects investors who hold other currencies. Photo illustration by Cherezoff/Shutterstock.

• Part 2 of a series. Part 1 appeared on July 23, 2019. •

• NOTICE: This column will begin a temporary hiatus in August 2019. To continue receiving my articles, subscribe now to the free Muscular Portfolios Newsletter.

We saw in Part 1 of this series that investors who hold currencies other than US dollars (USD) like to own securities that are denominated in their own money. This helps to minimize currency risk: the chance that the other currency will move against you, eating up your gains.

Even relatively stable currencies like USD and the Canadian dollar (CAD) expose investors to risk. Just in recent years, US-priced securities gave Canadian holders a haircut of about 35% in 2007–2016, solely from the foreign-exchange fluctuation. On the other side of the coin, Canadians gained an extra 74% if they held USD investments in 2002–2007.

It’s hard to predict currency swings, as I’ve previously reported. A good plan for investors who use currencies other than US dollars, therefore, is to buy securities denominated in their local currency that “offer to hedge” most currency risk away. This means, for example, that a Canadian’s investment in an index of US large-cap stocks would have approximately the same percentage gain as Americans themselves received, no matter how the USD-CAD exchange rate shifted.

One of the model strategies in my book Muscular Portfolios involves nine low-cost exchange-traded funds (ETFs). Nine is what I consider the minimum number of asset classes to let individual investors take advantage of diversification and relative strength. The nine-asset strategy was developed by Steve LeCompte, CEO of the CXO Advisory Group. He calls the formula SACEMS. In keeping with my book’s theme of Goldilocks Investing — not too risky, not too tame, just great gains — the strategy is also called the Mama Bear Portfolio.

The Mama Bear employs ETFs that are priced in US dollars. To help me determine which ETFs should be used as substitutes by investors who use other currencies, I spoke with Scott Clayton, a senior analyst for the TSI Network (The Successful Investor Network), based in Toronto, Ontario.

“iShares ETFs trade on the Toronto Stock Exchange,” Clayton notes. “XUS is the iShares Core S&P 500 Index ETF. XSP is the same thing, but is actually hedged.” The currency hedging prevents swings in the USD-CAD exchange rate from affecting the returns of Canadian investors. In Canada, Clayton continues, “Vanguard has VFV for the S&P 500, and VSP for the S&P 500 hedged.”

ETFs that protect against currency nightmares may legitimately have annual fees that are a small fraction of a percentage point higher than their USD equivalents due to the insurance cost, Clayton says. For example, take VOO, Vanguard’s US-based index fund that tracks the S&P 500. “VOO charges 0.03%. VFV and VSP charge 0.08%.” I believe small differences such as this are worth it for the peace of mind.

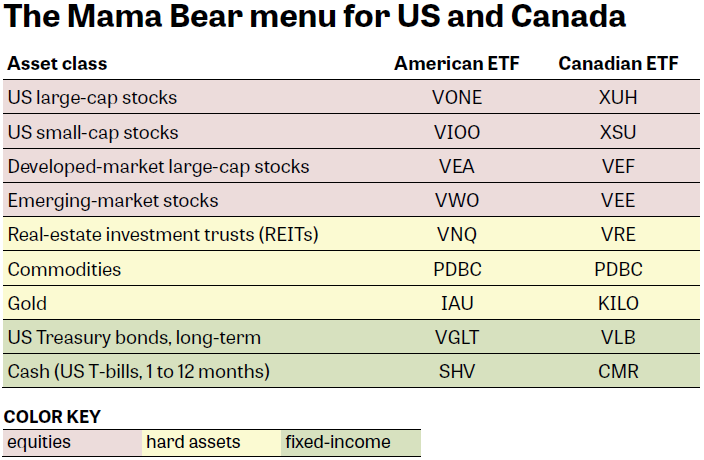

Using index ETFs offered by Vanguard Canada, BlackRock Canada (the parent of iShares), and Purpose Investments, I put together the table in Figure 2. It shows the CAD-denominated ETFs that should come the closest to matching the USD-priced ones in the Mama Bear “investing universe” (menu).

It’s impossible for me to specify the index funds that investors in every country of the world should use. In today’s column, I name funds that are priced in CAD as examples. But you can repeat the process for any country or currency and get similar results — although, if you use different ETFs, you can’t expect the returns to be identical.

Figure 2. Investors who use currencies other than the US dollar can usually find index funds for sale in their countries that will approximate the USD performance without taking on the currency risk. Source: MuscularPortfolios.com.

If you simply held in your portfolio an equal weight of the nine ETFs, you’d have what’s known as a Lazy Portfolio. However, as we’ve seen in my previous column, every Lazy Portfolio performs much better in the long term if you add a single Momentum Rule. With this single tweak, you’re also subjected to smaller losses during bear markets. The strategy rules for the Mama Bear Portfolio are as follows:

- Select a specific day each month to tune up your portfolio. LeCompte produced a study showing that the best days to make course corrections were the first two trading days of the month and the last seven trading days, although the difference might not be significant.

- On your chosen day, rank the nine ETFs by their gain, including dividends, over the past 105 trading days (about five calendar months).

- Sell any ETF that is not in the top three, and purchase any ETFs you don’t already own that are in the top three.

- Rebalance only if any ETF is more than 20% off its ideal dollar weight in the portfolio. Exact percentages are not important.

The five-month gains of the nine US-dollar ETFs are available free of charge on the Mama Bear page of Muscular Portfolios website. The page’s numbers are recalculated every 10 minutes while the New York markets are open. The gains of the Canadian-dollar ETFs should be very similar to those of the equivalent USD index funds.

What the non-US index ETFs actually index

The following is a short explanation of the CAD-denominated symbols in Figure 2. The annual fee for each ETF — which in Canada is called the “management expense ratio” or MER — is shown in parentheses. All ETFs in the list below that hold non-Canadian assets are CAD-hedged, except where noted.

EQUITIES

- XUH — The iShares S&P US Total Market Index ETF holds all US stocks, delivering mostly the gains of American large-caps. The Total Market Index has better historical performance than the S&P 500. (MER: 0.07%.)

- XSU — The iShares US Small-Cap Index ETF tracks the Russell 2000 index of smaller American stocks. (0.36%.)

- VEF — The Vanguard Developed All-Cap ex-US Index ETF tracks stocks in all developed countries except the US, thereby including all Canadian stocks. (0.22%.)

- VEE — The Vanguard Emerging Markets All-Cap Index ETF tracks stocks in developing countries. (0.24%.) This fund is not CAD-hedged. At this writing, there don’t appear to be any hedged emerging-market ETFs. Hopefully, Vanguard, iShares, or another provider will develop one.

What if you want to hold more Canadian equities than the percentage in VEF? Make three changes:

- Add Vanguard’s VCE for exposure to Canadian large-cap stocks. (0.06%.)

- Add iShares’ XCS for Canadian small-caps. (0.55%.)

- Replace VEF with Vanguard’s VI. (0.23%.) This ETF tracks all developed-country stocks except those in the US and Canada. Holding VI instead of VEF avoids duplicating the American and Canadian equities that are indexed in XUH, XSU, VCE, and XCS.

HARD ASSETS

- VRE — The Vanguard Canadian Capped REIT Index ETF includes real-estate investment trusts and other publicly traded real-estate securities in Canada. (0.39%.)

- PDBC — The PowerShares Deutsche Bank Commodity Index ETF tracks a basket of commodities, which are mostly energy and agricultural products. (0.59%.) This is a US-based ETF and is not CAD-hedged.

- KILO — The Purpose Gold Bullion Fund mirrors the spot price of physical gold. (0.20%.)

Like the situation with emerging-market stocks, there may not be at this writing a commodities ETF that’s hedged for other currencies. Most commodities are priced in US dollars in world markets, so investors who use other currencies do take on some foreign exchange risk.

KILO is a relatively new gold-bullion ETF that launched in October 2018. According to a review in Wealth Professional Canada, KILO’s 0.20% annual fee is one-half to one-third as much as other physical-gold ETFs that are priced in Canadian dollars. The sponsor of KILO allows withdrawals in units of one kilogram (2.2 pounds). The reviewer says this is only “a tenth the redemption requirements seen at other [Canadian] physical gold bullion funds.”

Withdrawing one kilo of gold at a time would cost approximately 50,000 USD at today’s spot price. Canadians who don’t want to tie up that much capital in gold could always buy IAU, a US-dollar-denominated ETF. That physical-gold fund currently costs only about 13.70 USD per share. You’d simply accept the currency risk.

FIXED-INCOME

- VLB — The Vanguard Canadian Long-Term Bond Index yields whatever a basket of Canadian government and corporate bonds with maturities of 10+ years may be paying. (0.19%.)

- CMR — The iShares Premium Money Market ETF plays the role of “cash” in the portfolio, like T-bills. But CMR holds CAD debt obligations from Canadian governments and corporations with a very short — and ultrasafe — weighted maturity of about 36 days. (0.28%.)

Unfortunately, I can’t estimate the returns that the above CAD-denominated ETFs would have generated over the past four or five decades, as I can for Muscular Portfolios that use USD index funds. The historical data that’s available for the asset classes in US dollars might not match the same assets that were priced in other currencies.

The best we can do is look at the track record for the Mama Bear and other portfolios in my column of July 16, 2019. You can decide for yourself whether the substantial boost in returns — and the sizeable reduction in losses — is worth the 15 minutes it takes to tune up such a portfolio each month.

I think it’s worth it, no matter what currency you may use — if you hedge your risk.

With great knowledge comes great responsibility.

—Brian Livingston

Send story ideas to MaxGaines “at” BrianLivingston.com